Global Market Analysis

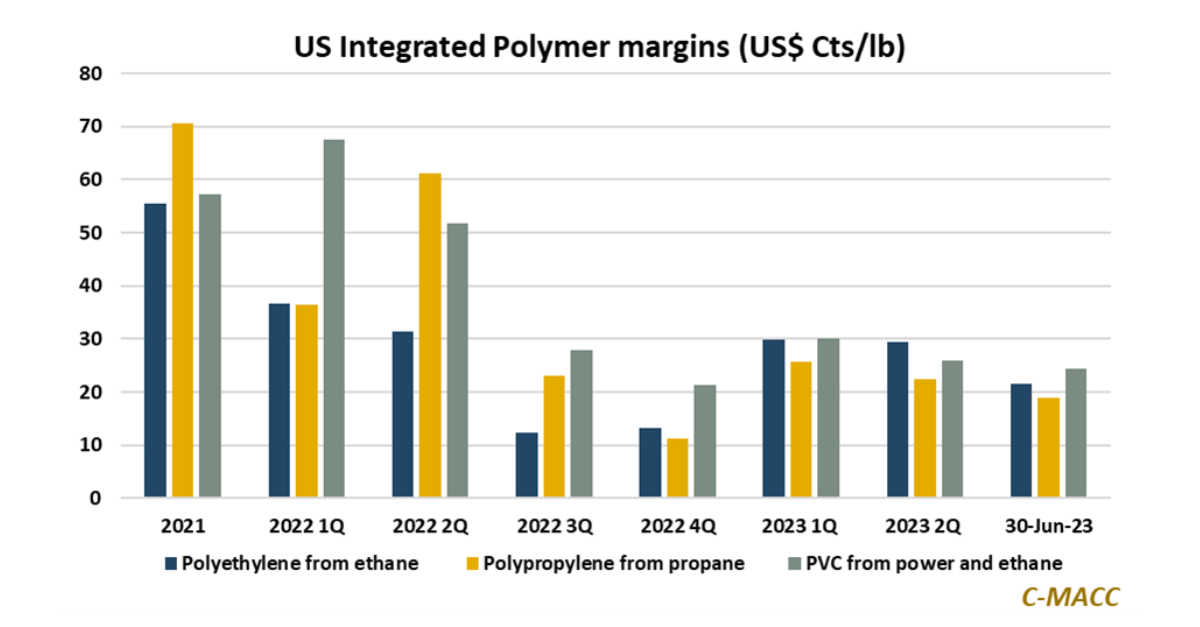

Global commodity chemical production margins ended the June quarter lower than the 2Q23 and 1Q23 averages, setting the stage for a lower 3Q23 (and 2H23)

Global commodity chemical production margins ended the June quarter lower than the 2Q23 and 1Q23 averages, setting the stage for a lower 3Q23 (and 2H23)

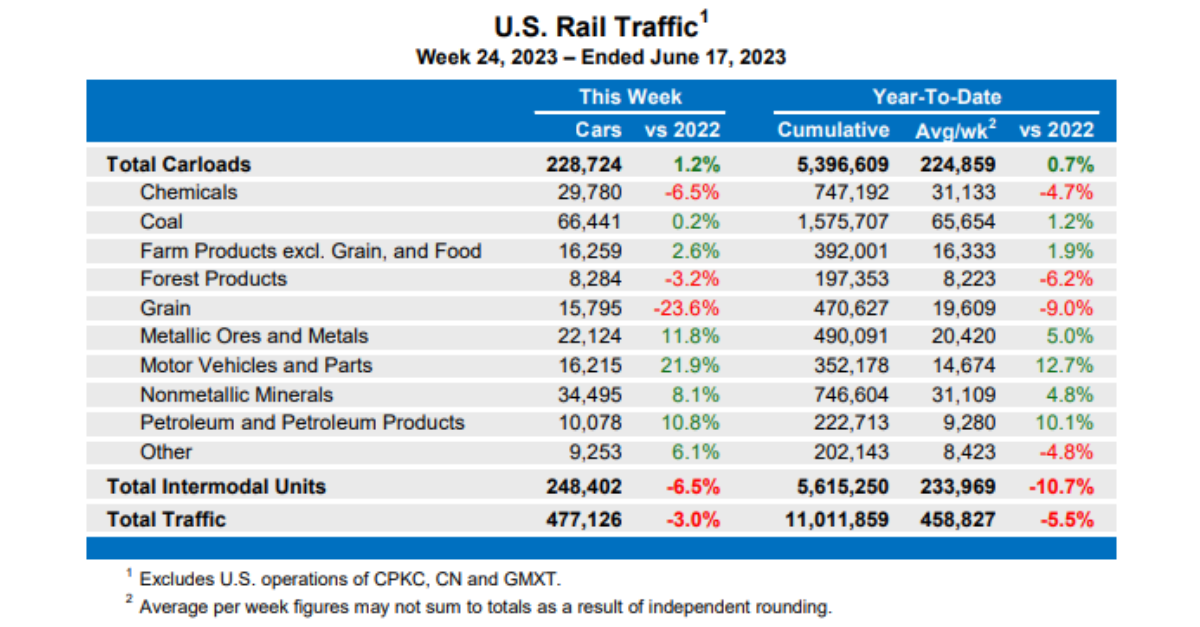

Drought conditions and a heat wave hit most of the US in June, putting its crop production at risk and lifting electricity demand. The June

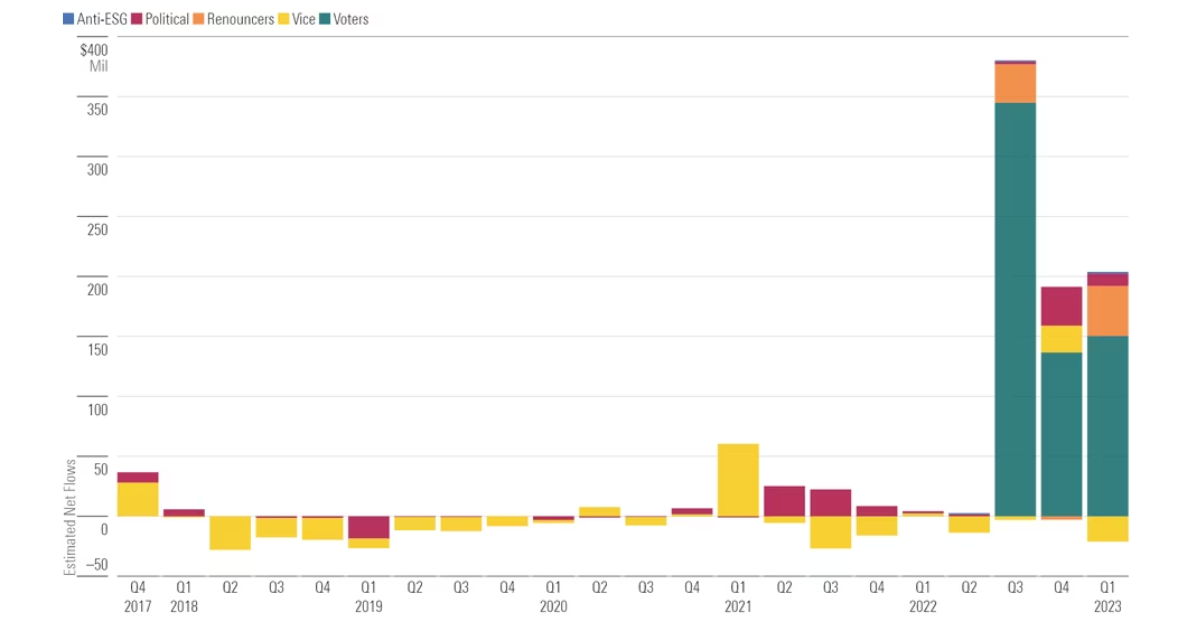

As Larry Fink removes the acronym ESG from his vocabulary, it is reasonable to ask how something that is intuitively right is now buried in

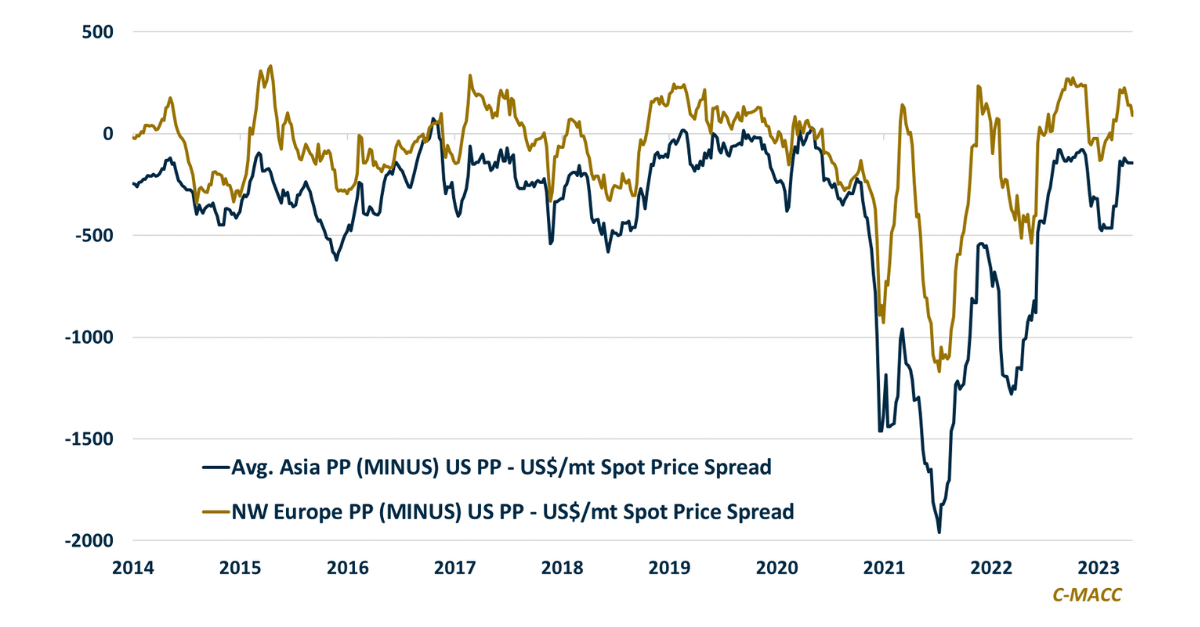

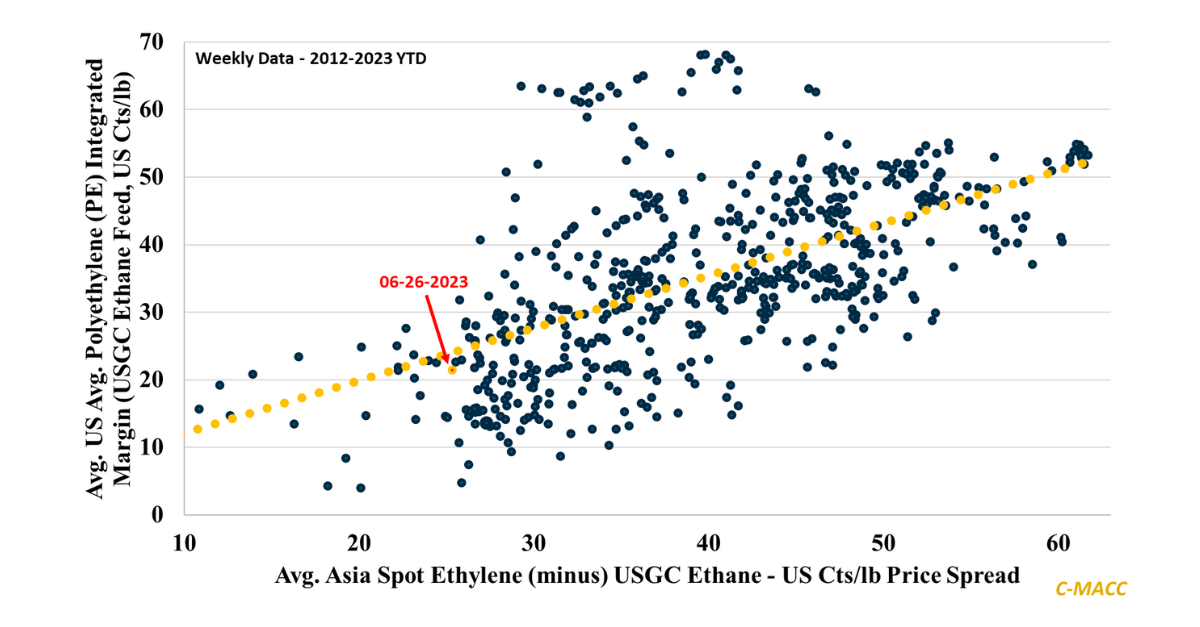

Spot polypropylene price spreads between major global regions have returned to pre-COVID levels, but prices (and profits) are lower, putting most 2023 outlooks set with

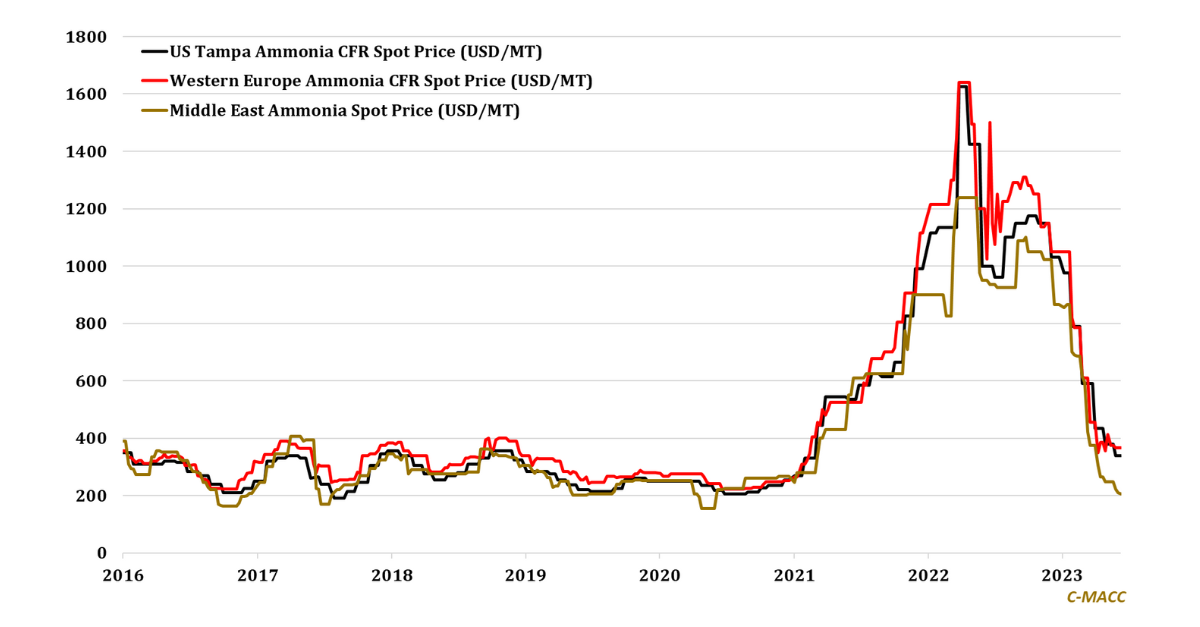

Global ammonia markets remain weak, but better times are on the horizon, as supply appears unlikely to keep pace with broadening existing and new demand

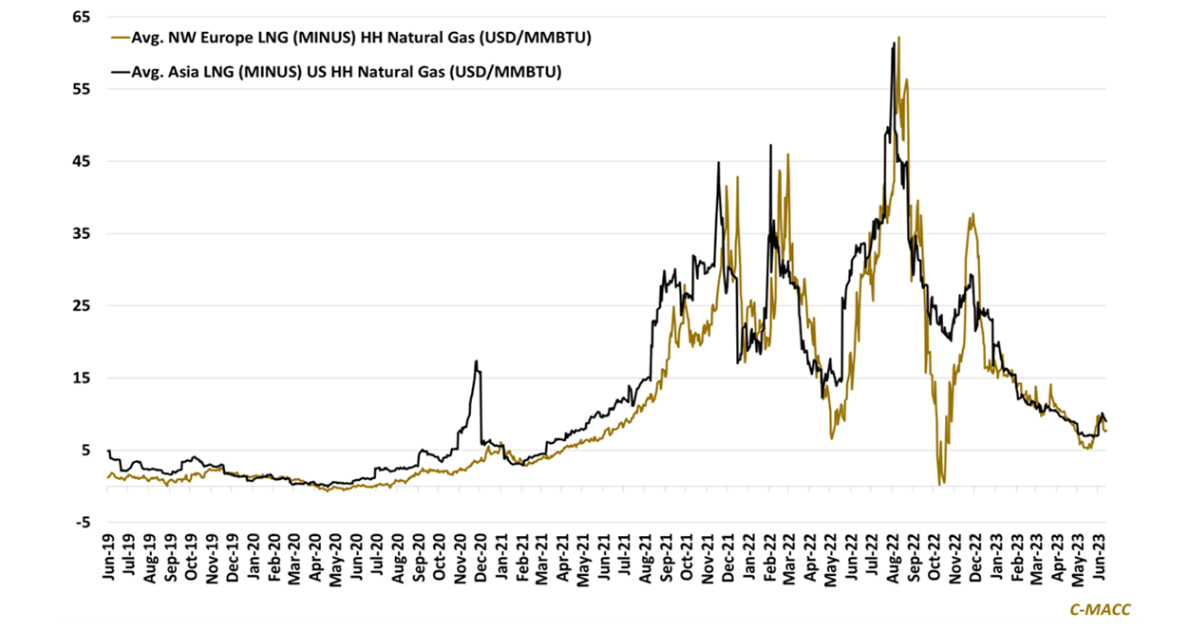

Global commodity chemical market indicators show growing oversupply, with sizable outages likely needed to enable price hikes for most polymers in 3Q23. 2Q23 shows lower

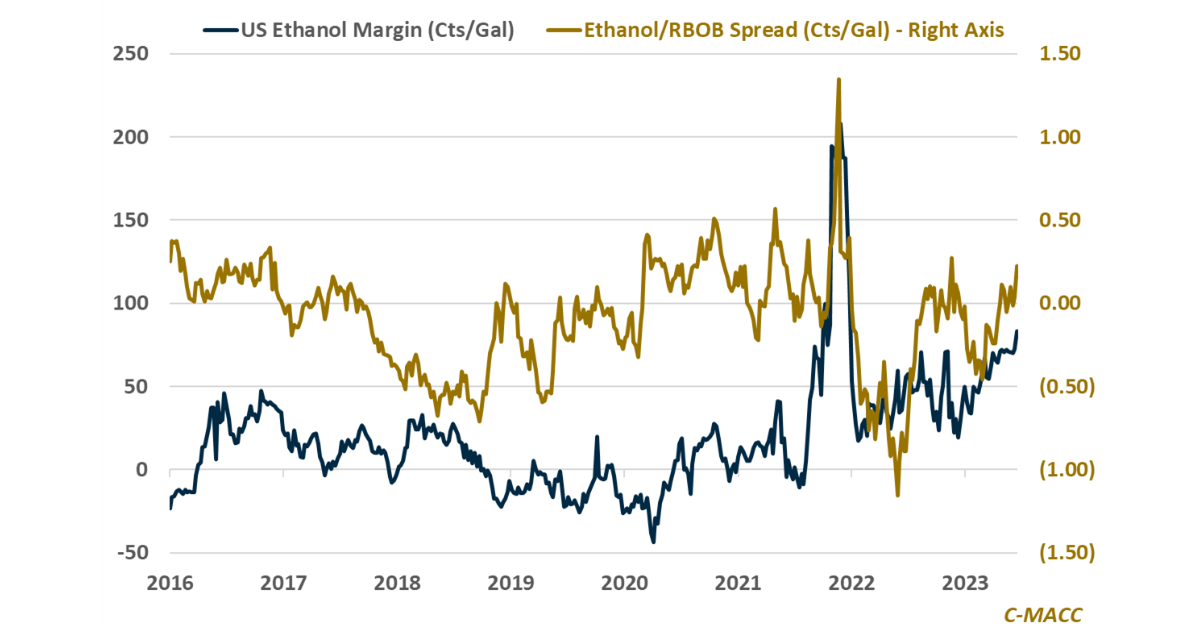

US crop indicators point to higher prices and farmer incomes, while US commodity chemical indicators illustrate an oversupplied setting and rising margin pressure despite cost

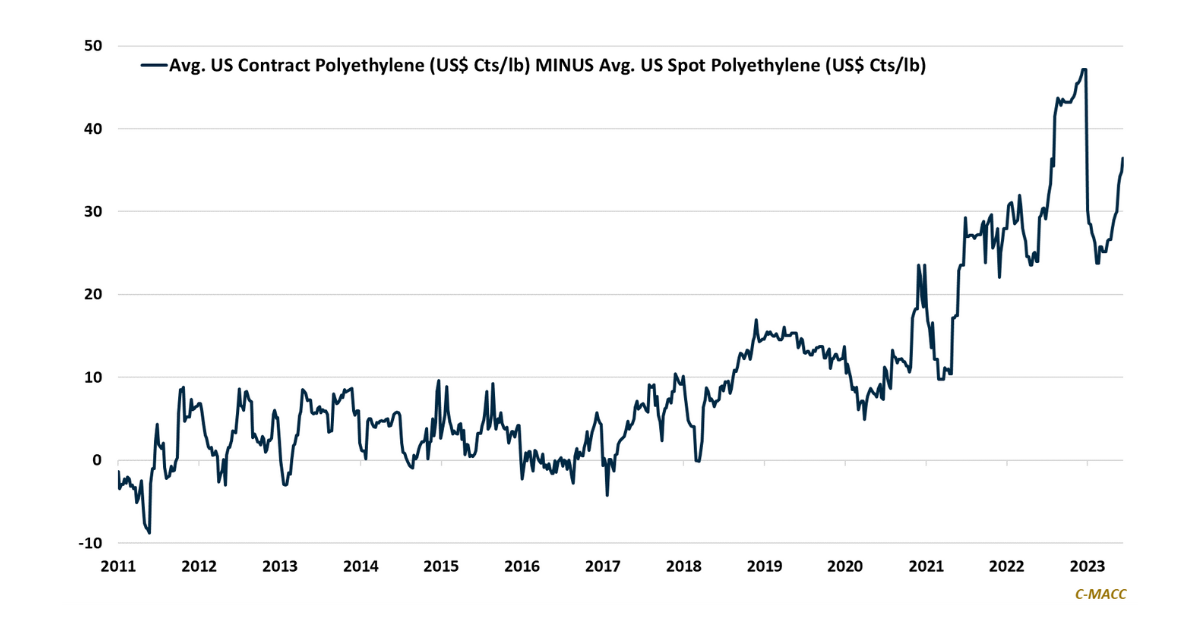

US polyethylene contract prices show an upward trend relative to spot values as exports have risen compared to domestic demand, becoming less linked to the

Blue hydrogen (and ammonia) reflect different challenges relative to green, as one requires cheap natural gas and a place to store/consume carbon, and the other

As we watch the “anti-woke” lobby in the US cause investors to step back from the responsibility they should never have wanted in the first