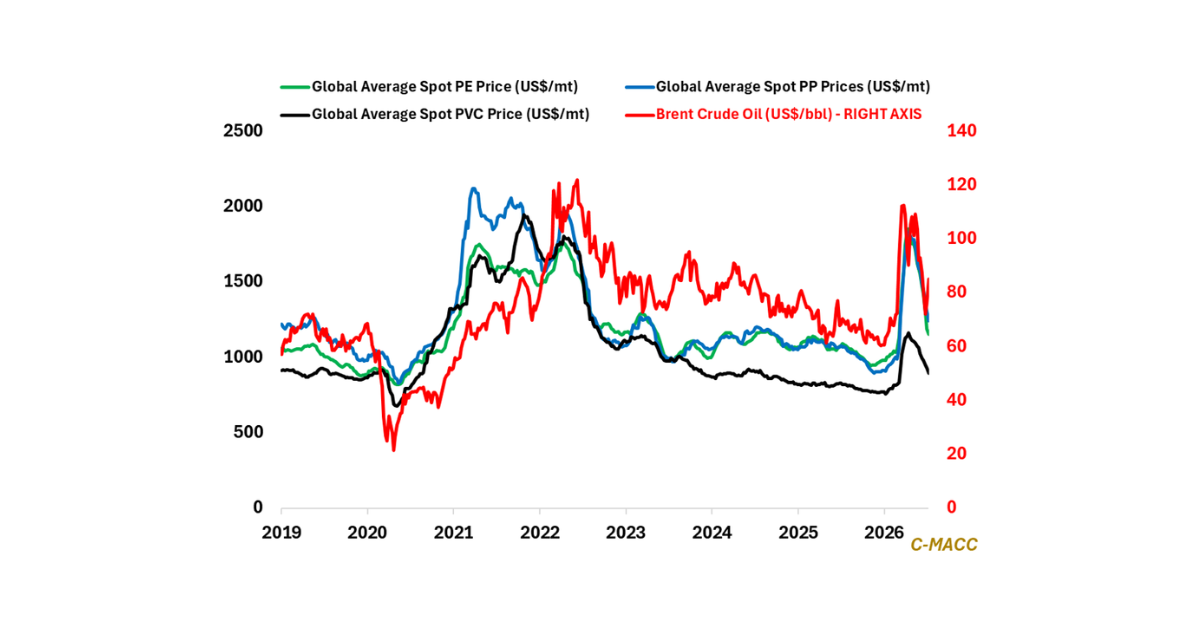

Polymer Global Analysis

General Thoughts: North American producers are gaining an edge as overseas margins weaken, with dependable integrated plants best placed to convert lower feedstock costs into

General Thoughts: North American producers are gaining an edge as overseas margins weaken, with dependable integrated plants best placed to convert lower feedstock costs into

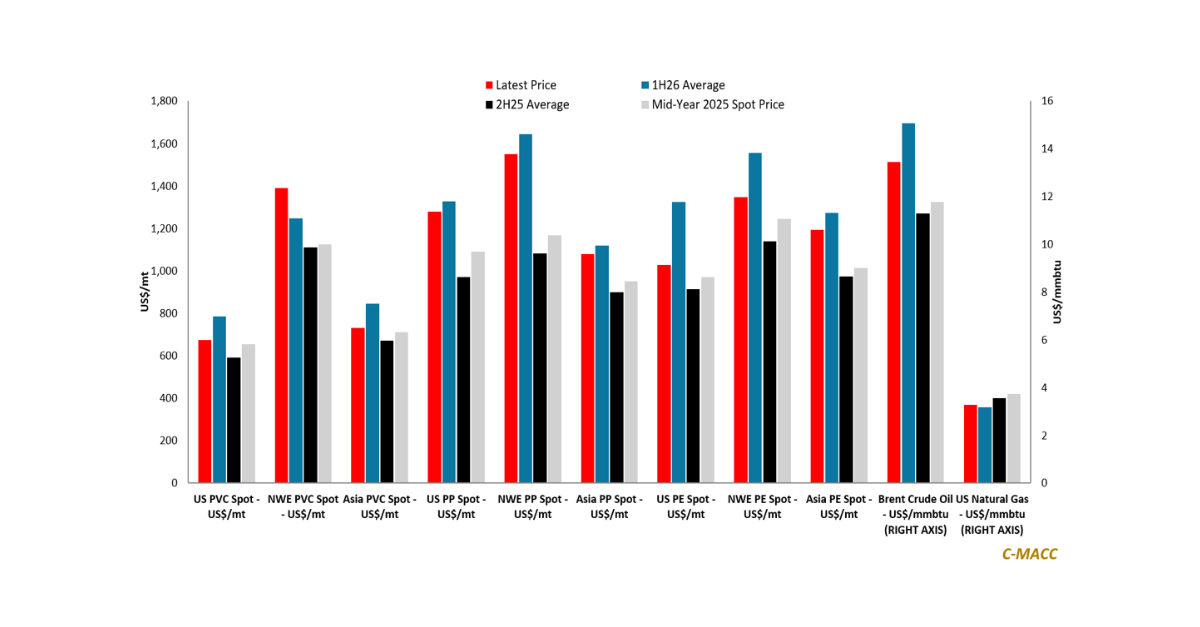

General Thoughts: During 2Q26 earnings calls, polymer producers will address July prices below June-quarter averages, but higher costs and supply risks challenge forecasts for sustained

General Thoughts: Global polymers are shifting from broad price erosion to contested floors as firmer crude and China spot support challenge consensus, while new capacity

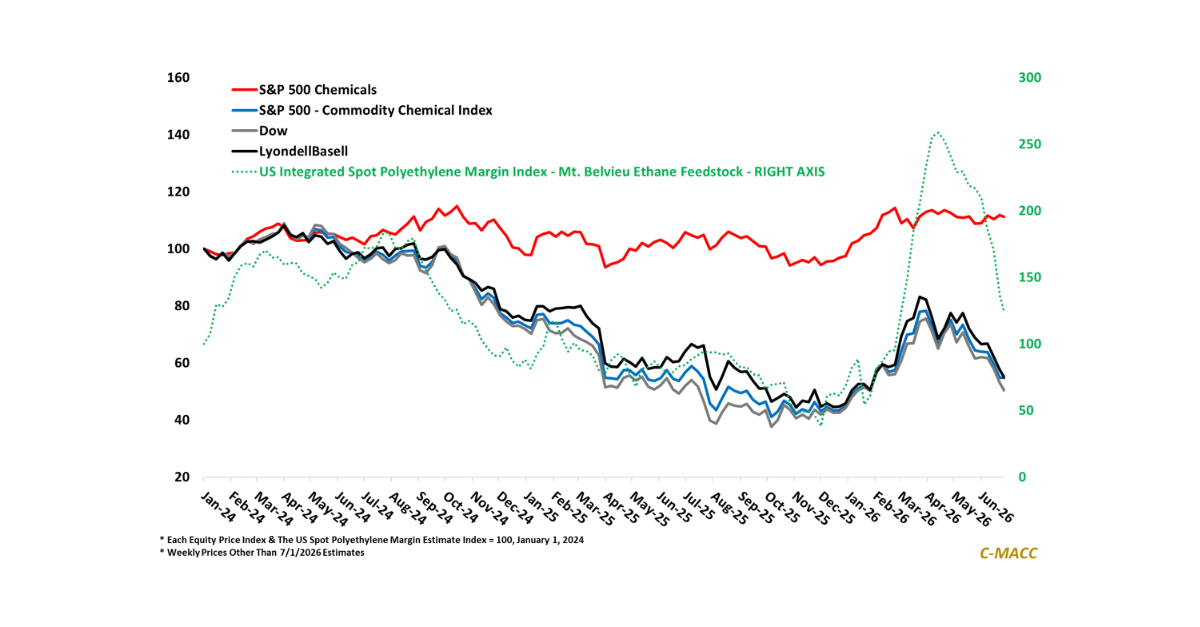

General Thoughts: US commodity chemical stocks track fading margins, but slower contract adjustments, buyer deferral, 2H26 disruption risk, and Asia ex-China and European restructuring challenge

General Thoughts: Global polymer buyers are waiting for crude and feedstock floors to form, as China exports and falling monomer prices shift price control toward

General Thoughts: Falling global polymer prices test which producers can defend returns, as excess supply, PE grade splits, PP route differences, PVC policy friction, and

General Thoughts: Plastic alternatives give brands more packaging choices, pushing polymer producers toward direct collaboration with brands or leaving converters with greater control over future

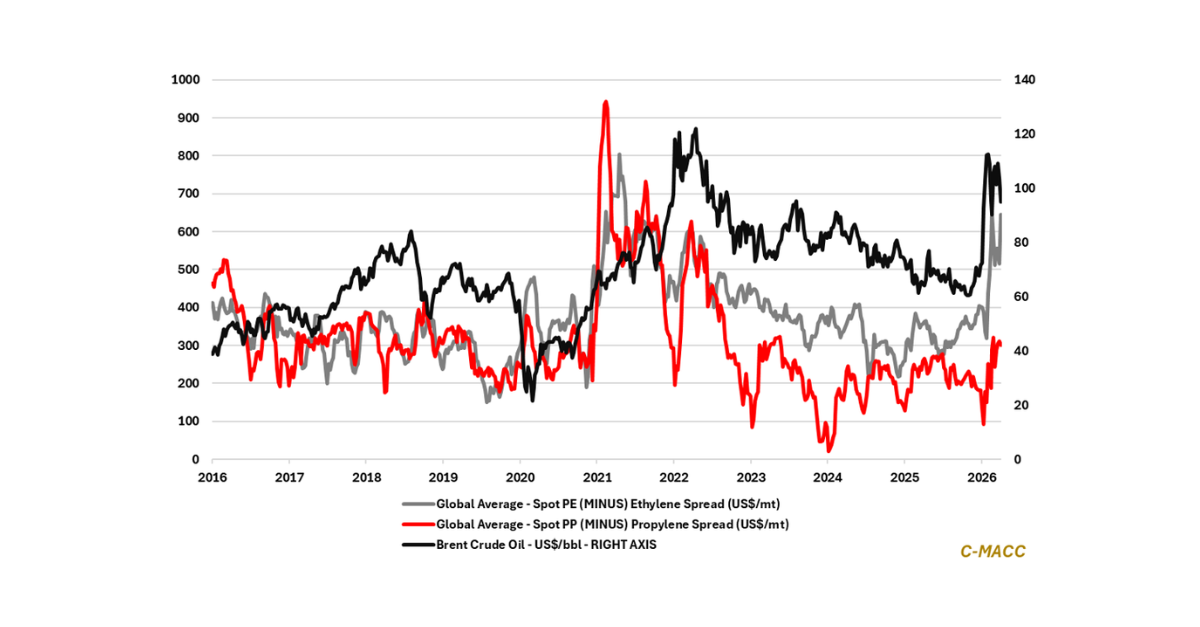

General Thoughts: Global polymer-to-monomer spreads remain above levels supported by feedstock costs and trade flows, leaving prices exposed as freight stabilizes, buyers preserve cash, and

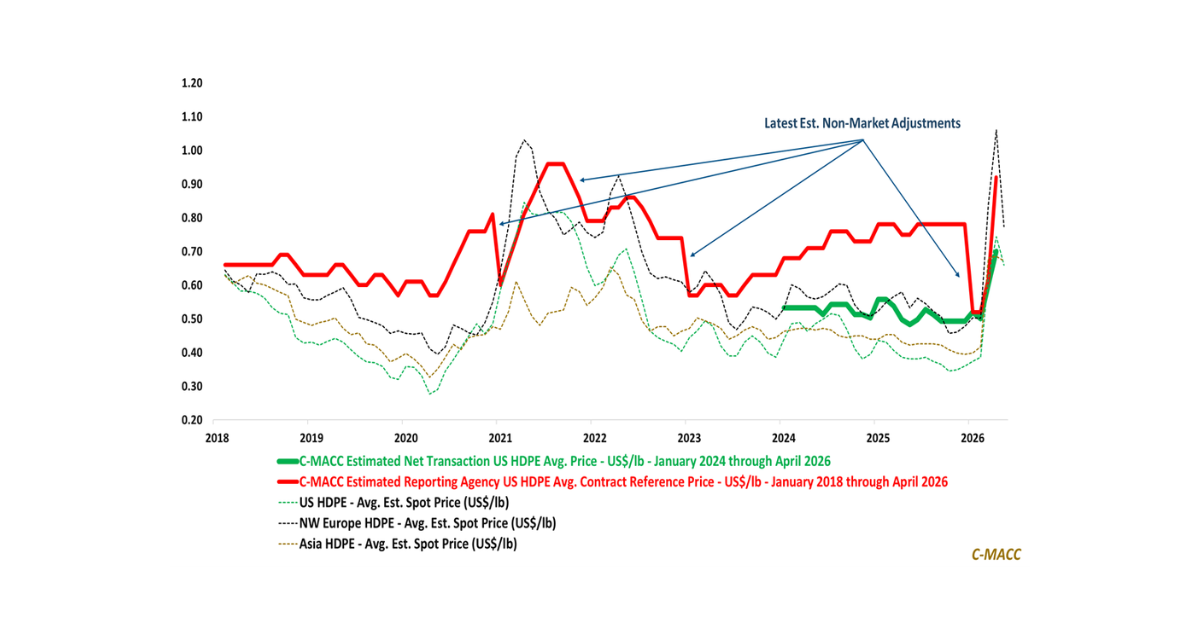

General Thoughts: Another US PE non-market adjustment may become more likely by year-end if spot weakness challenges contract benchmarks, reinforcing C-MACC’s value in pricing, procurement,

General Thoughts: Global polymer markets are exposing how buyer caution and inventory risk can weaken realizable pricing, amid uncertain demand and despite supply disruptions supporting