Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

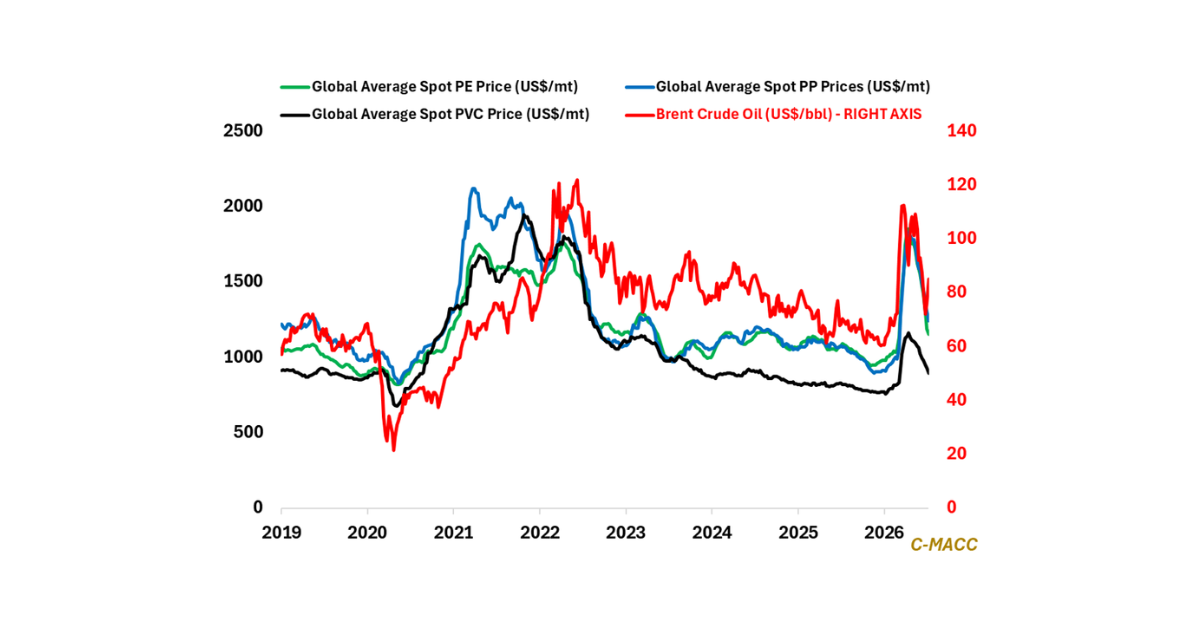

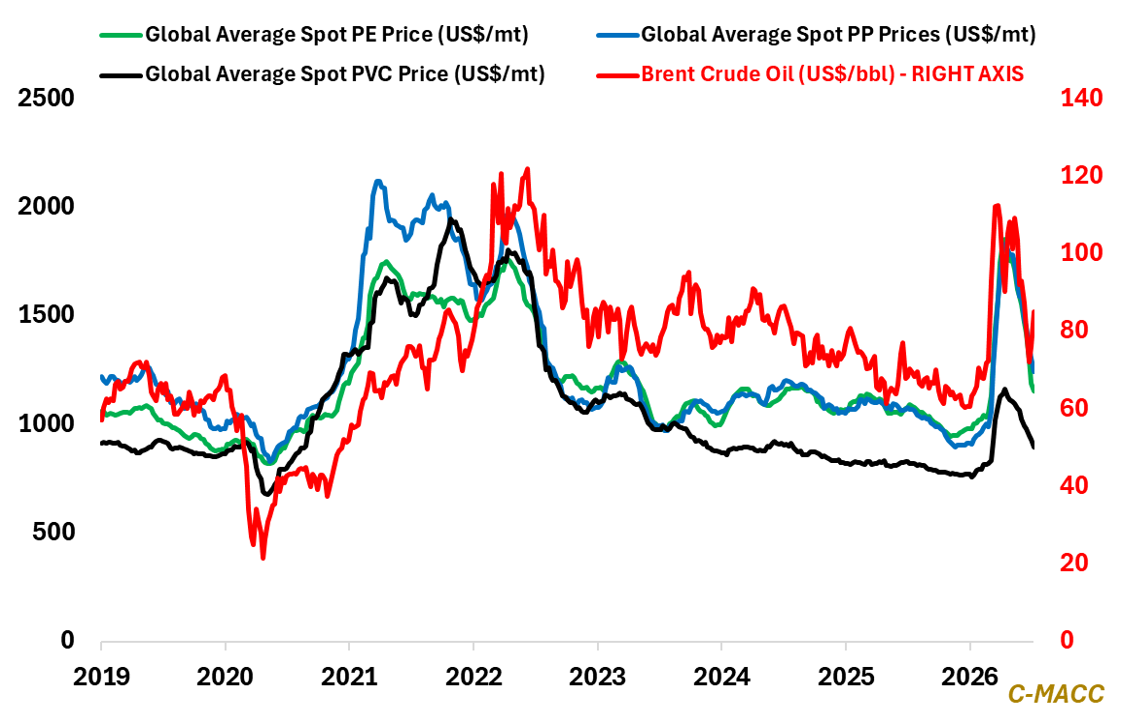

- General Thoughts: During 2Q26 earnings calls, polymer producers will address July prices below June-quarter averages, but higher costs and supply risks challenge forecasts for sustained 2H26 weakness or a return to 2H25 levels.

- Polyethylene (PE): Rising European and Asian PE production costs are shortening buyers’ purchasing windows, supporting 3Q26 spot prices and strengthening low-cost US capacity as uncertainty persists through year-end.

- Polypropylene (PP): Europe’s PP balance approaches an inflection as higher feedstock costs challenge buyer control, Asian cargo economics weaken, and regional dislocations support firmer global negotiations through 2H26.

- Polyvinyl Chloride (PVC): July’s Asian spot PVC price rebound points to better US export optionality, which could absorb June’s inventory build, tighten domestic balances, and improve producer leverage without requiring a demand recovery.

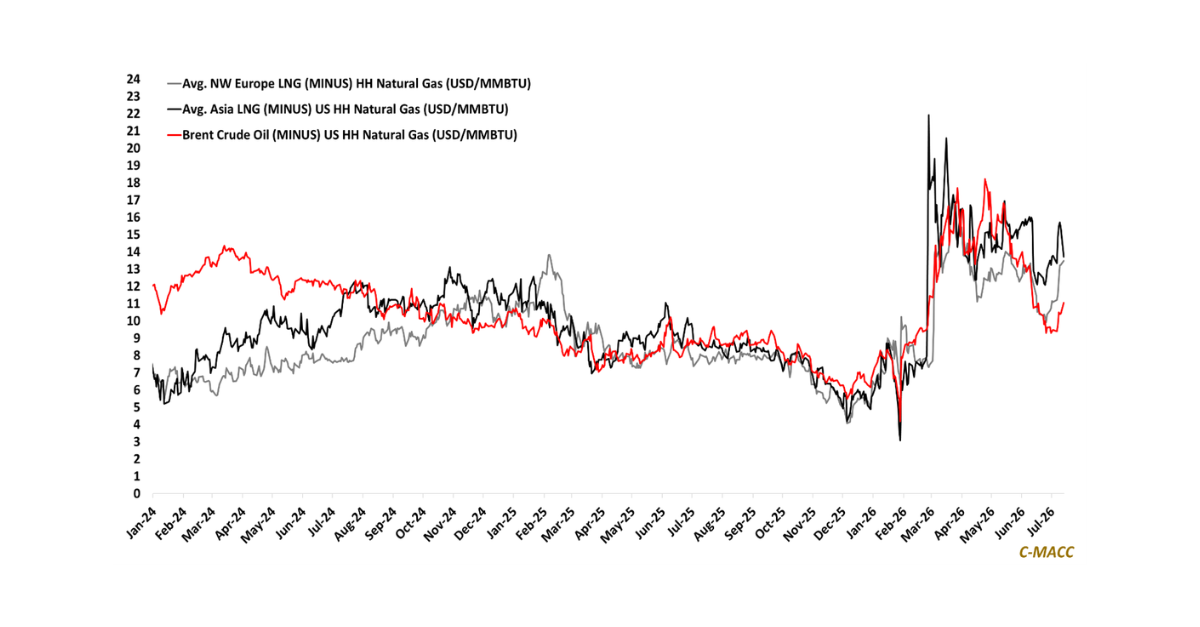

- Other Sector Developments: North American gas and NGL advantages deepen as higher oil and overseas gas costs widen production gaps, pressure foreign operating rates, and leave merchant olefin buyers less protected.

Exhibit 1 – Chart of the Day: Higher Crude and Trade Uncertainty Challenge Bearish 2H26 Polymer Forecasts.

Source: Bloomberg, C-MACC Analysis, July 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!