Base Chemical Global Analysis

General Thoughts: Downward price pressure across global chemical markets will likely persist through 4Q25 unless production curtailments intensify, with recent outperformers facing greater downside risk

General Thoughts: Downward price pressure across global chemical markets will likely persist through 4Q25 unless production curtailments intensify, with recent outperformers facing greater downside risk

General Thoughts: Shifting energy costs, tighter margins, and policy uncertainty redraw the global chemicals map, favoring integrated, flexible producers but pressuring most in a demand-

General Thoughts: Into 4Q25 and 2026, compressed spreads, uneven demand, and policy recalibrations converge, rewarding nimble low-cost producers while penalizing rigid models tied to fragile

Structure, not scale, determines valuation, capital access, and resilience as oversupply, policy volatility, and higher rates punish complexity yet reward clarity, focus, optionality, disciplined execution,

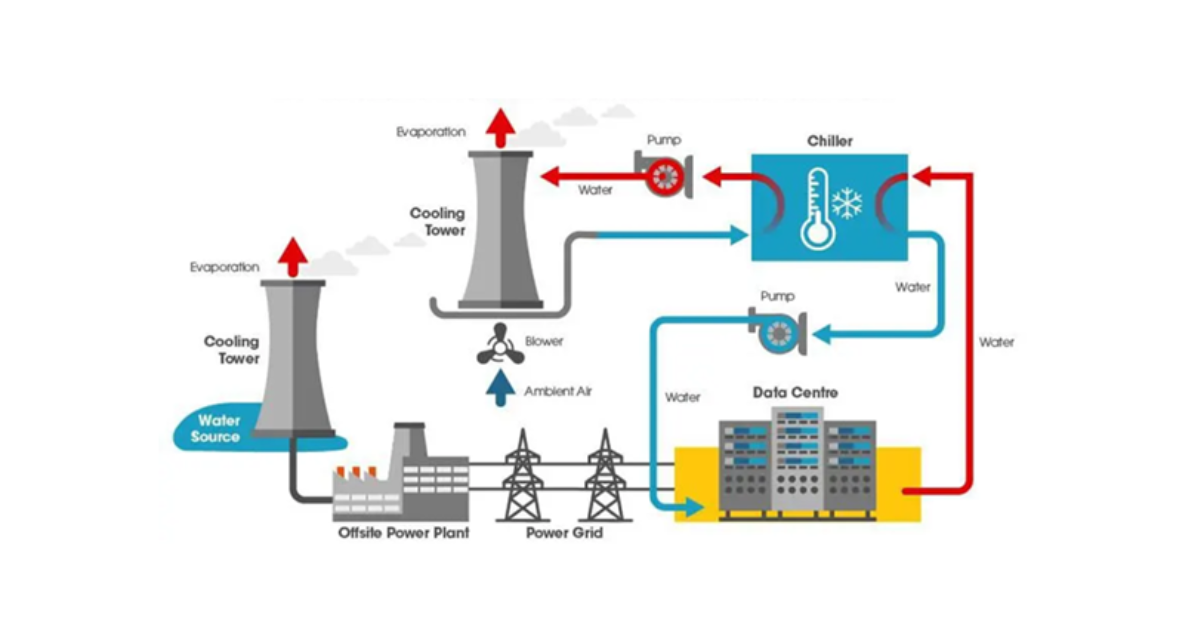

1st Topic of the Week: Water scarcity is AI’s hidden bottleneck, transforming data centers into hydrology-dependent assets. Will industry leaders secure resilient water strategies or

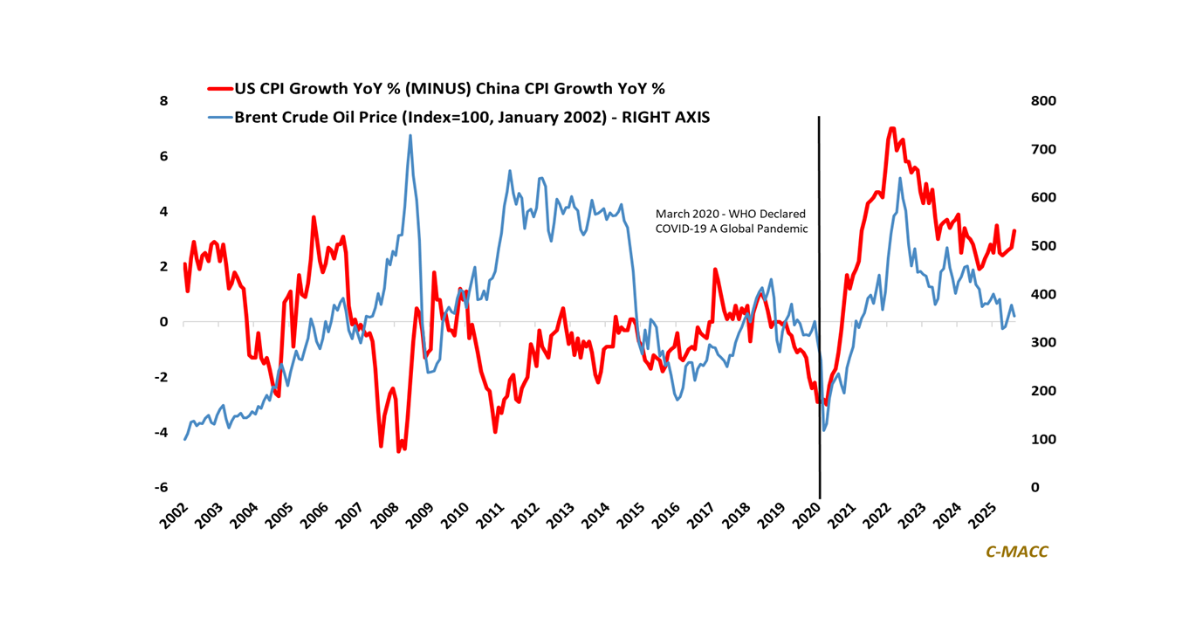

General Thoughts: Inflation divergence, steady USD/CNY, cheaper crude, and falling freight rates amplify China’s pricing power, compressing Western margins as outperformers prioritize corridor hedging, agility,

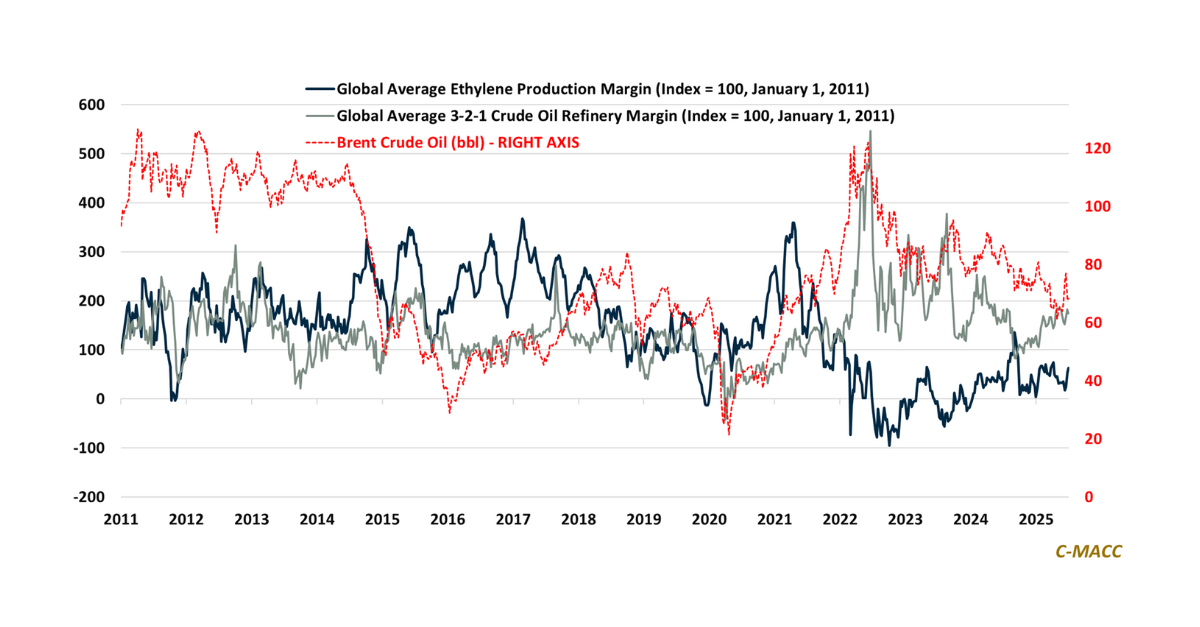

General Thoughts: Global refining margins have risen YTD on tight product balances, but chemical producers face persistent margin compression as oversupply, weak demand, and policy-driven

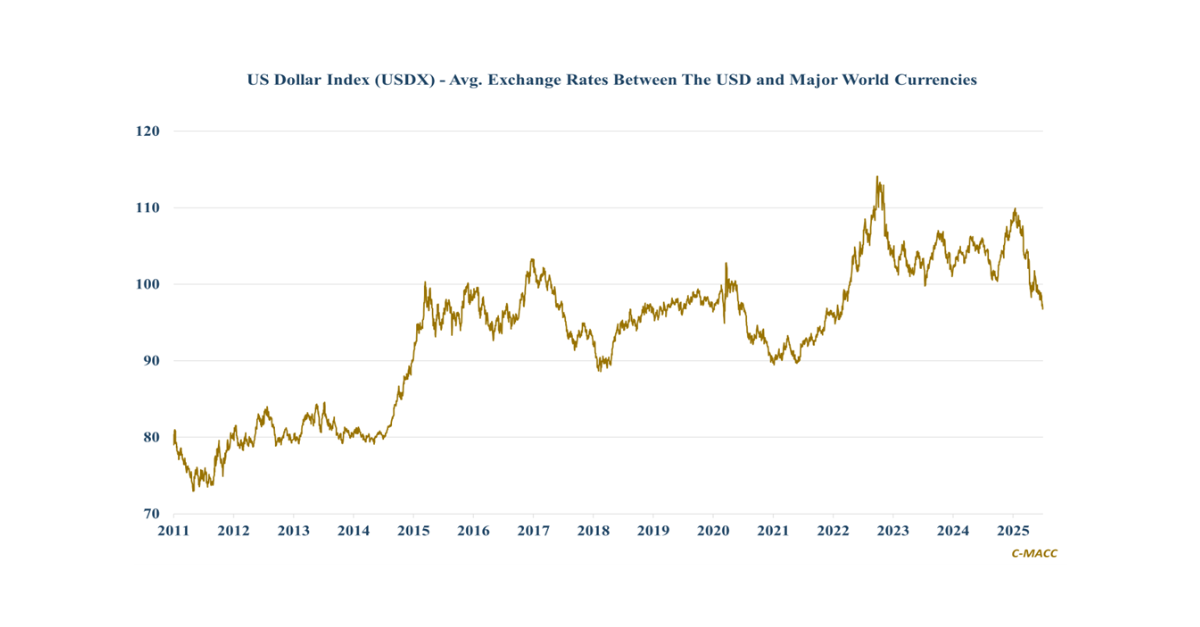

General Thoughts: The US dollar posted its worst first-half performance since 1973 in 1H25, and this decline lacks proper attention, as it increasingly favors US

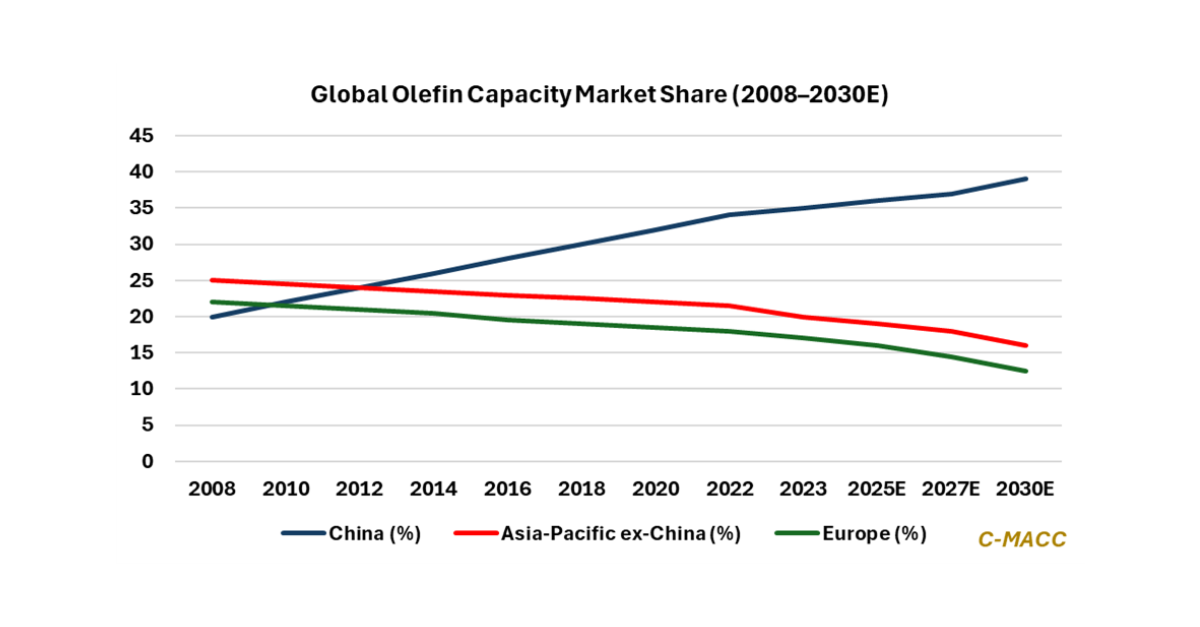

China is executing a long-cycle, state-aligned petrochemical strategy built on flexible feedstocks, converting refining into chemical scale and pricing advantage, while others contract under short-term

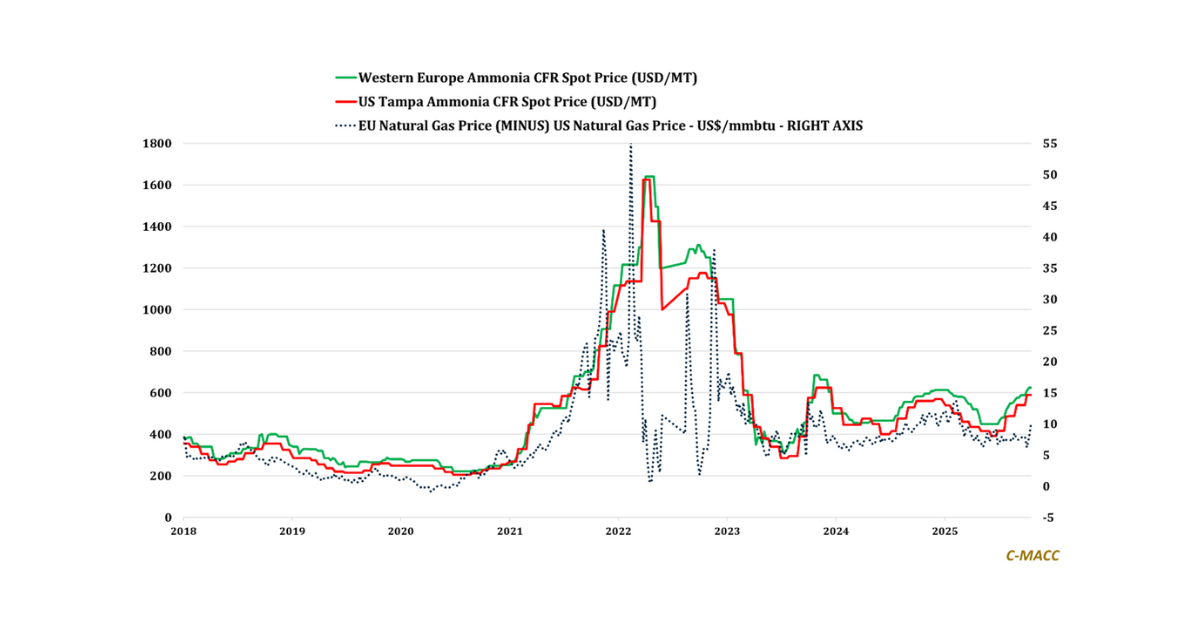

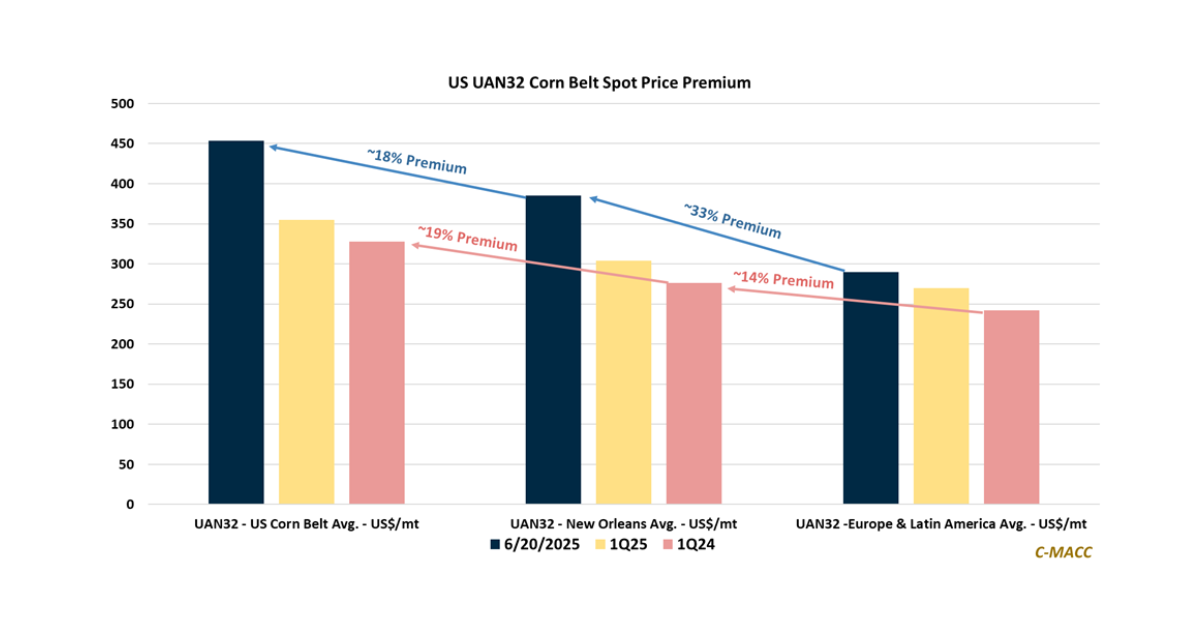

General Thoughts: Volatility demands agility in agri-energy markets, amid policy shifts and crop price fluctuations, which create headwinds likely to hurt ammonia market sentiment, despite