Base Chemical Global Analysis

Global Weekly Catalyst No. 302

- General Thoughts: Downward price pressure across global chemical markets will likely persist through 4Q25 unless production curtailments intensify, with recent outperformers facing greater downside risk than most.

- Feedstocks & Energy: With global crude oil prices trending lower, the recent widening spread between natural gas markets abroad and US prices will likely face downward pressure, setting the stage for lower chemical prices.

- Olefins: Global olefin margins remain under downward pressure as oil- and gas-linked feedstock values decline in a weak demand setting that reflects derivative oversupply, despite a few recent regional inventory cutbacks.

- Other Base Chemicals: Across aromatics, price erosion accelerates as crude-linked inputs soften; feedstock-driven pricing power will unlikely yield significant price improvement in 4Q25 unless met with production cuts.

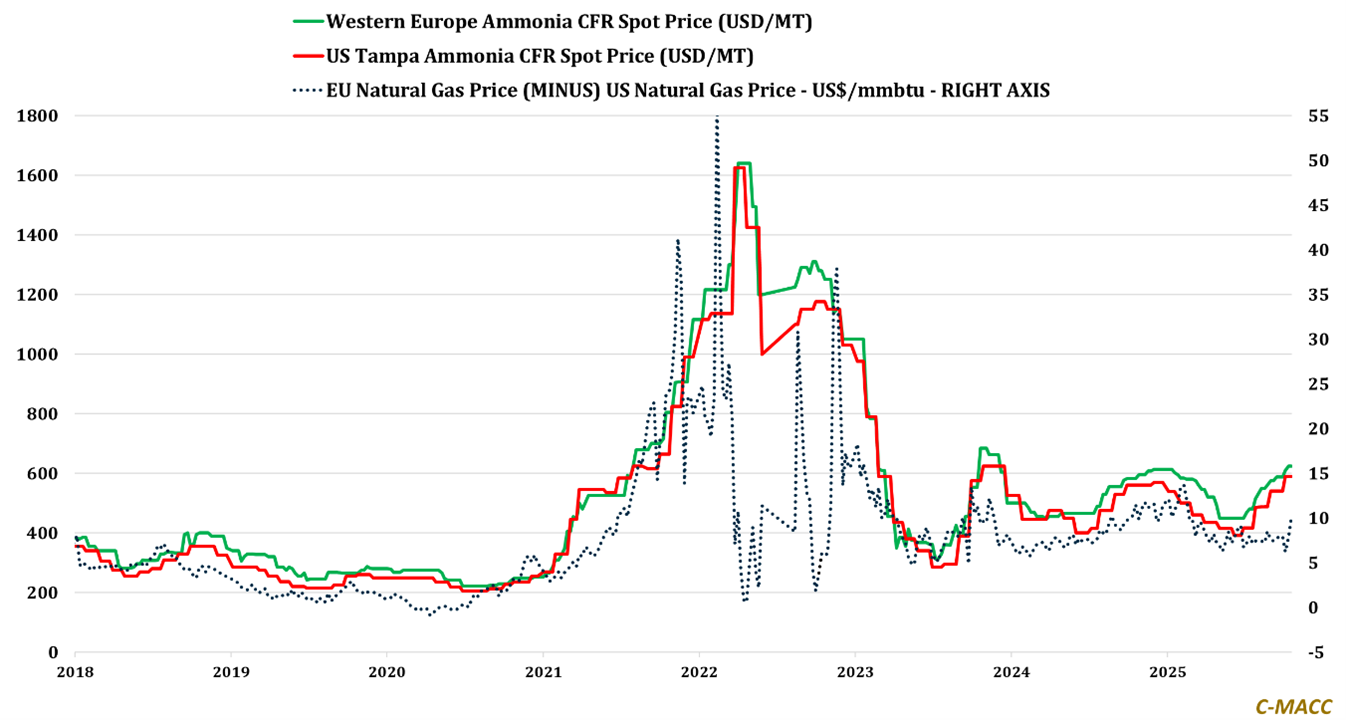

- Agriculture: Even as Western ammonia markets held their 2025 highs last week, recent feedstock spread improvement does not support it with tightness mostly resulting from production issues and corn enthusiasm.

- Refining & Biofuels: Ethanol and refined fuels are entering a policy-supported but margin-thin phase where declining input costs fail to offset decelerating seasonal consumption and volatile carbon compliance economics.

Exhibit 1 – Chart of the Day: Western ammonia spot prices hold 2025 highs; regional natural gas spreads tighter YTD.

Source: Bloomberg, C-MACC Estimates, October 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!