Global Market Analysis

General Thoughts: Our meetings at CERA differ from last year, as our discussions are now less about concepts and more about project return challenges –

General Thoughts: Our meetings at CERA differ from last year, as our discussions are now less about concepts and more about project return challenges –

Since mid-year, the acetyl chain has experienced substantial volatility, with low-cost producers benefiting upstream and downstream benefits mixed contingent on pricing power and demand.

We reiterate our constructive view of fertilizer and agricultural chemical markets, as we view this market as better poised to improve in late 2023 and

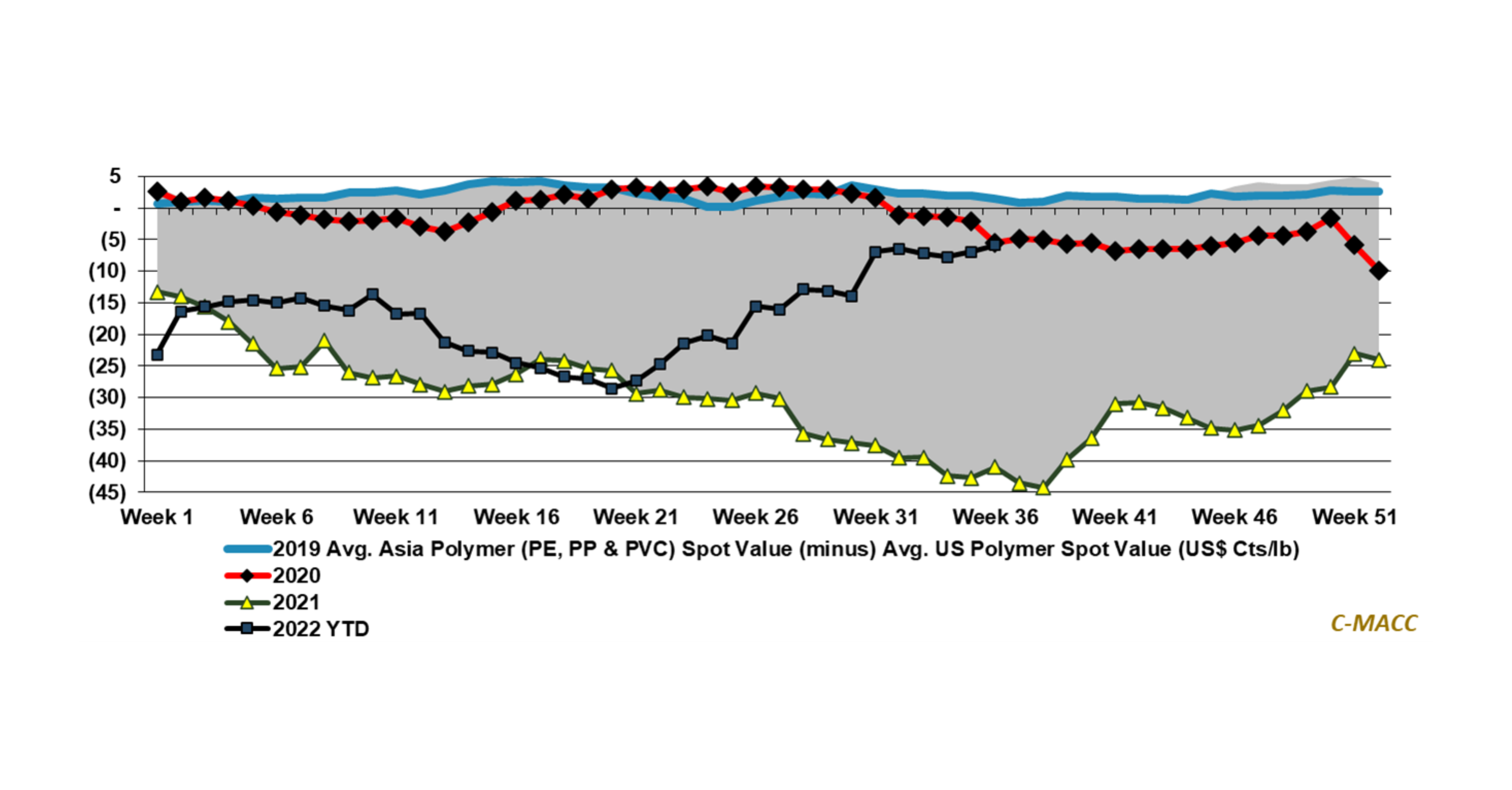

Global freight rates reflect downward pressure in 1H23, supporting the case for supply chain improvements and suggesting reduced commodity price differentials between regions in 2023.

2023 is off to a bad start with low margins (but maybe not low enough) and global operating rates reflecting significant oversupply, which could worsen.

European chemical producer cutbacks will unlikely offset oversupplied Asian markets to support prices into 2023, limiting US cost benefits and forcing a battle from within.

We are critical of the Bloomberg “no chemical investment” initiative as, unusually for Bloomberg, it shirks environmental responsibility in our view.

The US can

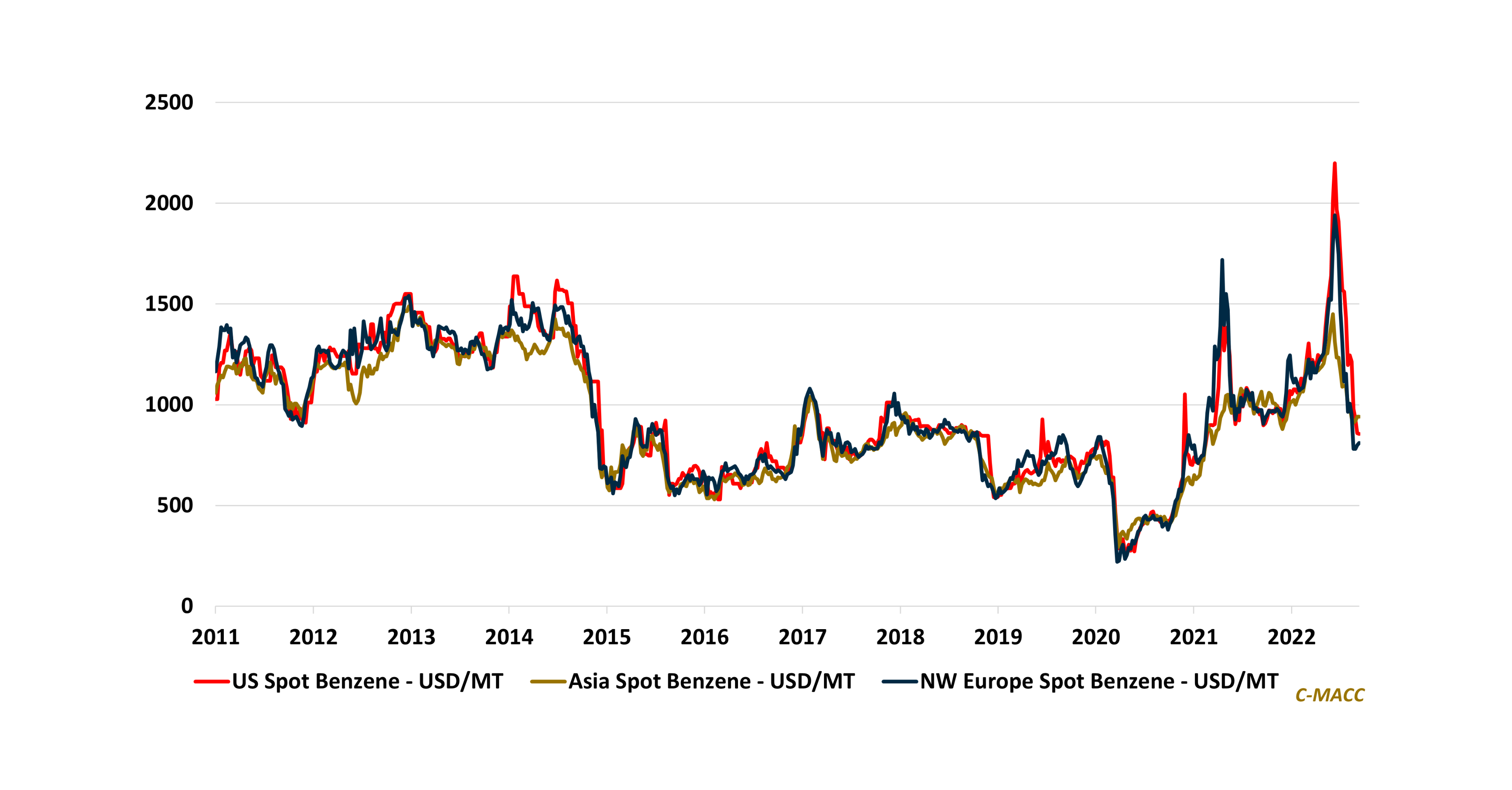

Global commodity chemical prices have declined during the past three months, but demand concerns outweigh the benefits of cost relief for most derivative producers.

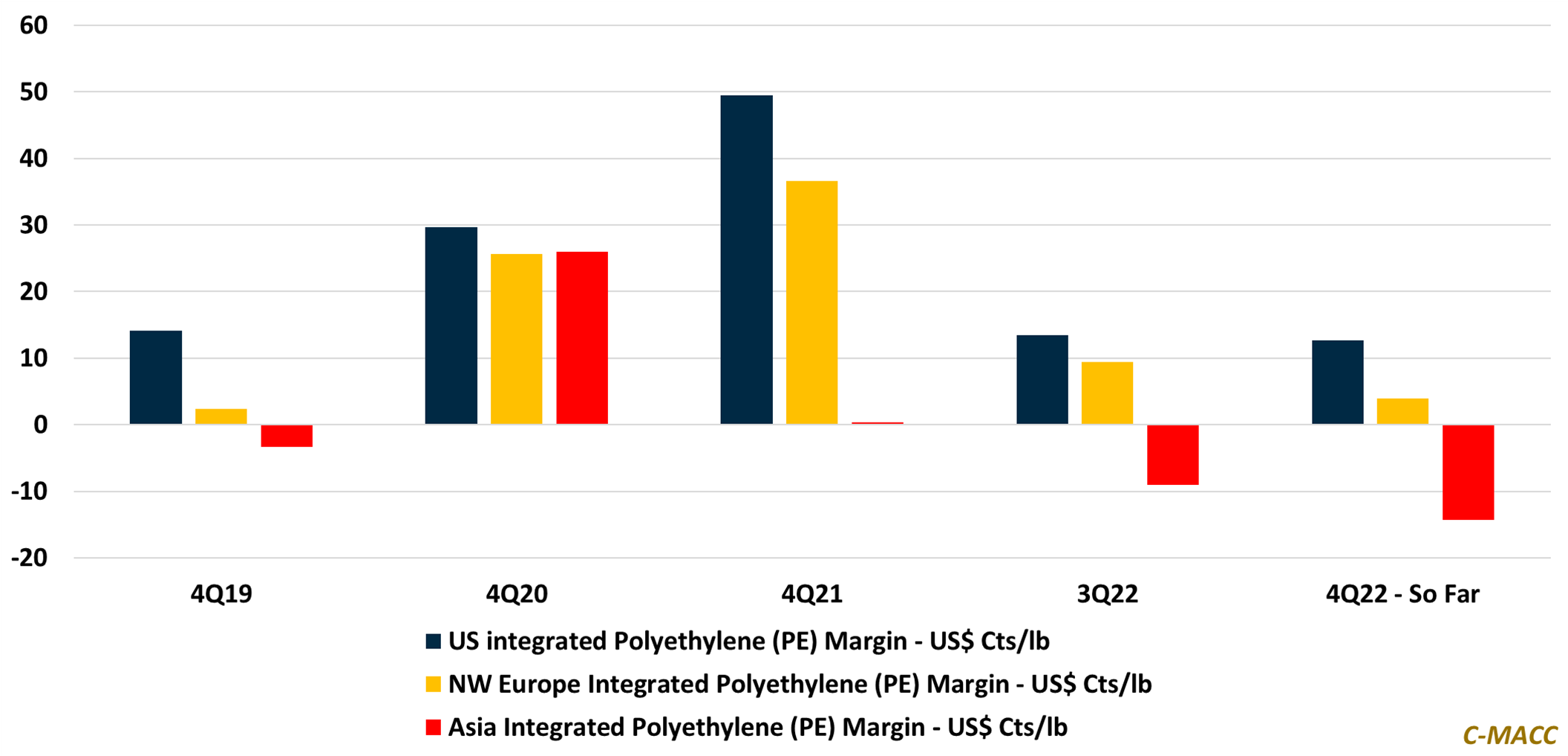

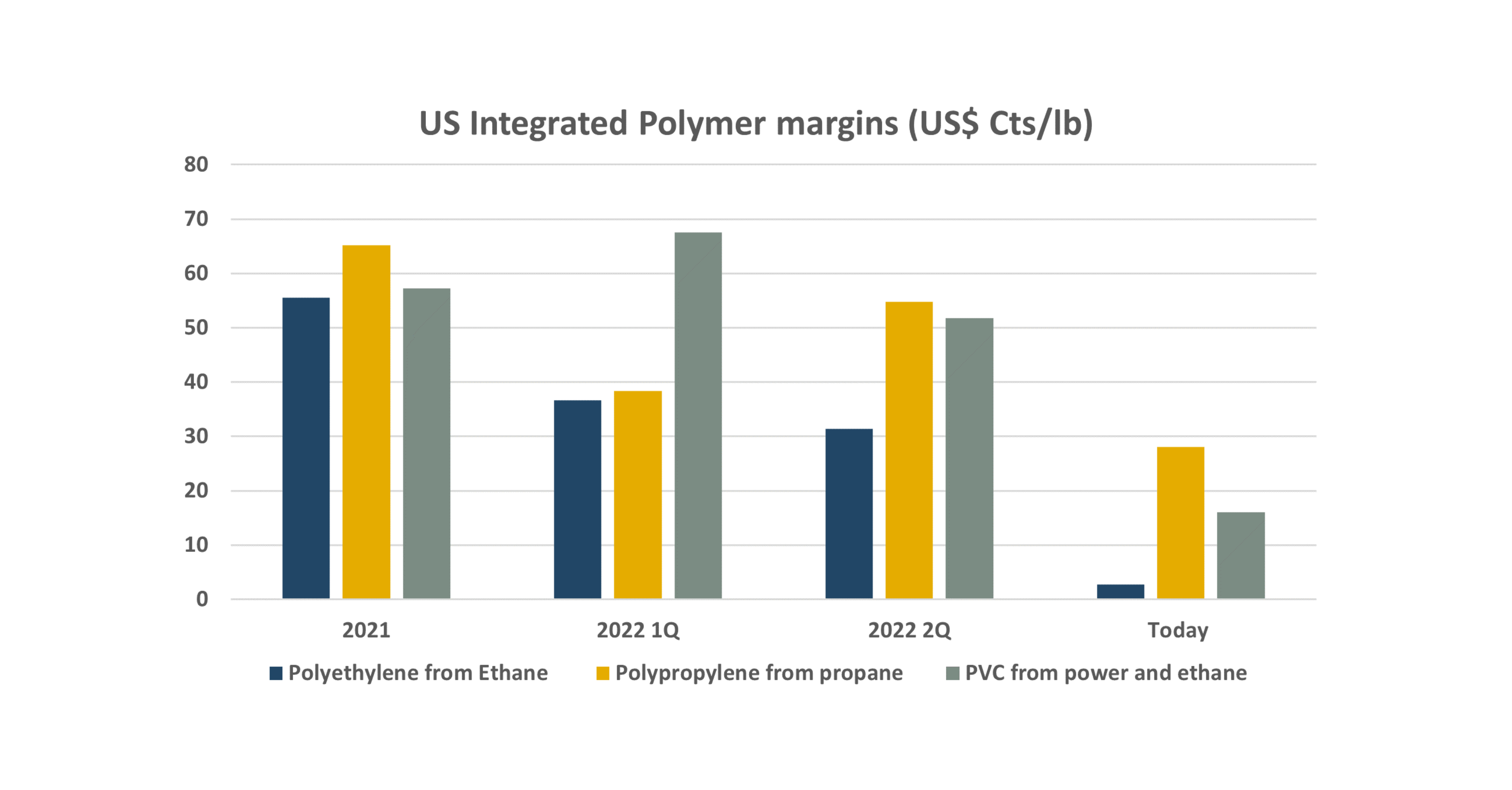

Global polymer prices have declined significantly relative to 1H22 highs, and we discuss the collapse in US premium polymer prices compared to Asia since 2Q22.<br

Chemical producers are increasingly cutting 3Q profit expectations but fail to give 4Q views despite Street estimates likely being too high – this is a