Global Market Analysis

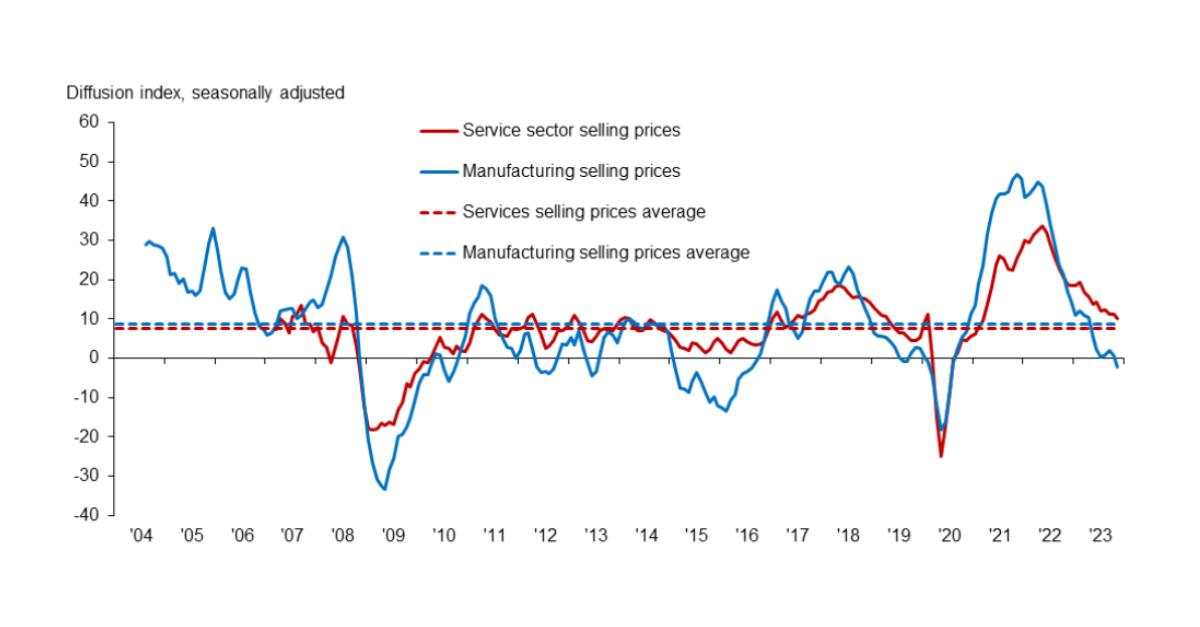

The price of manufactured goods in the US faces downward pressure into year-end amid lower global input costs – crude oil price strength is a

The price of manufactured goods in the US faces downward pressure into year-end amid lower global input costs – crude oil price strength is a

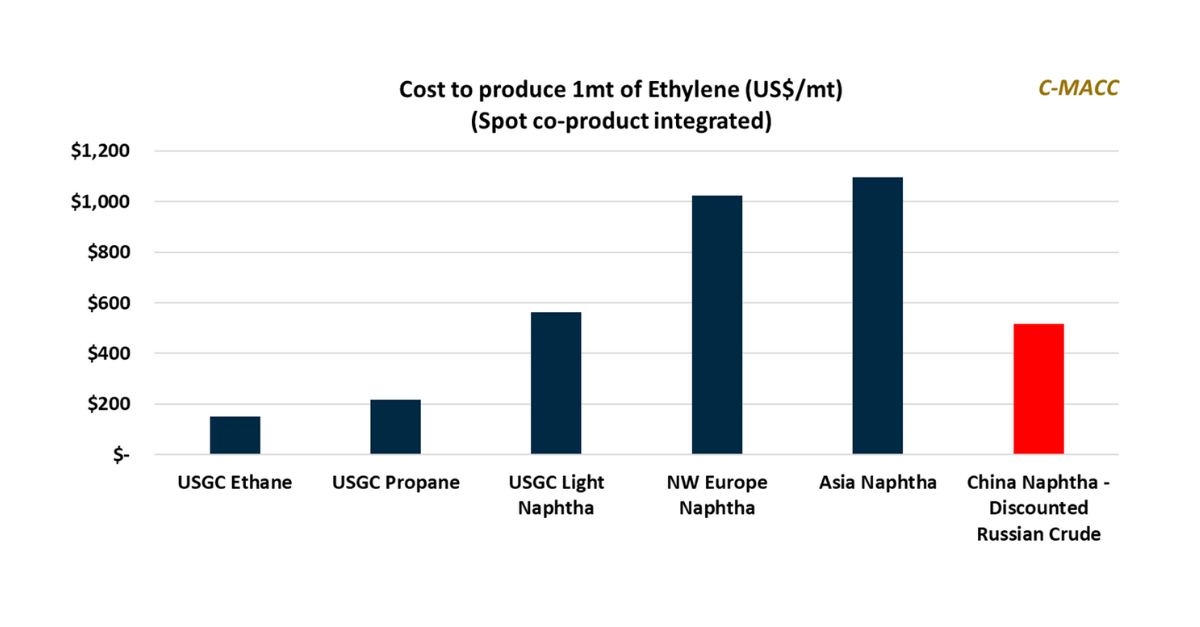

China has imported ~20% more discounted Russian crude oil YTD in 2023 compared to 2022, a benefit to its global petrochemical production cost position and

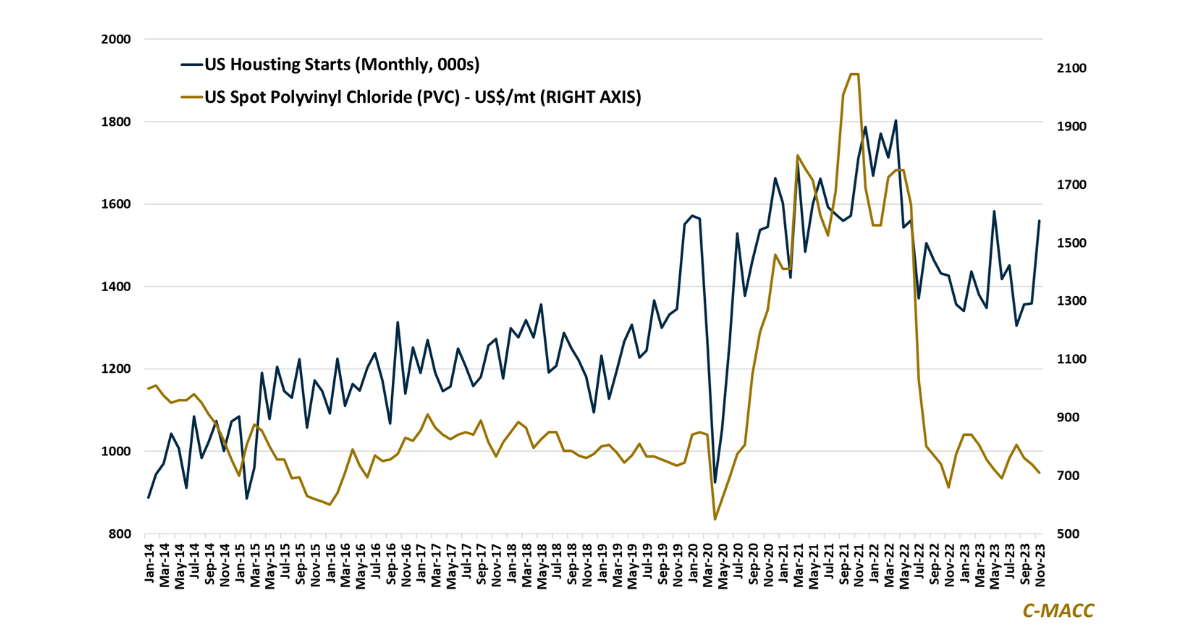

Falling mortgage rates and loosening but still tight domestic home supply are spurring housing market activity that could extend into 2024 and prove constructive for

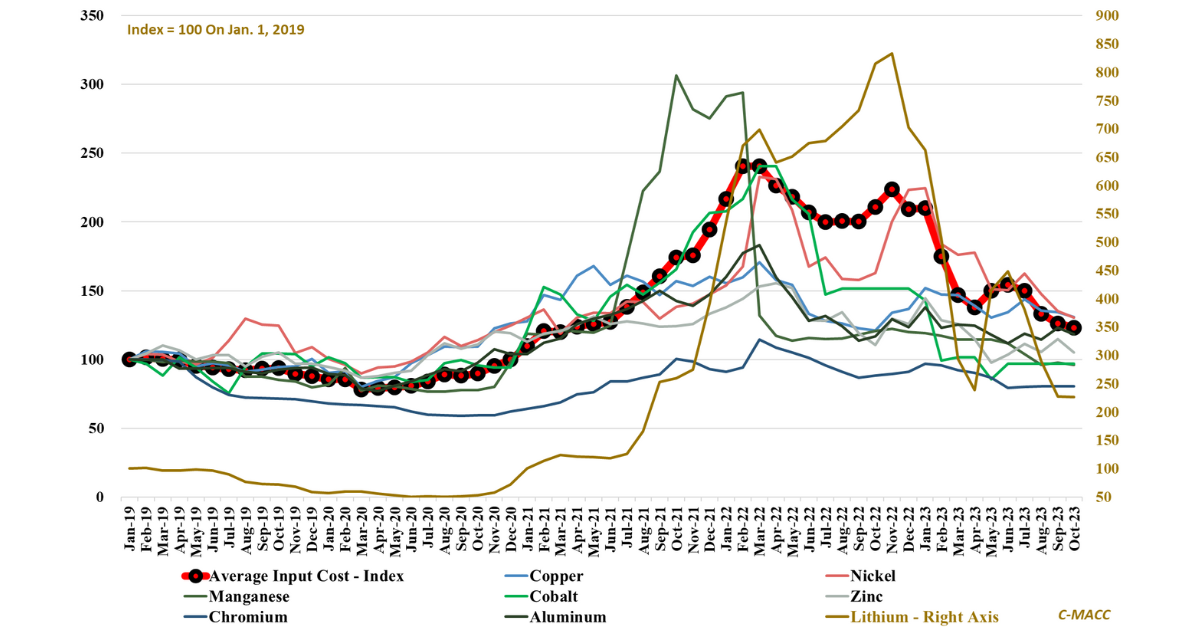

The C-MACC Clean Energy Mineral Index fell to a new YTD low in November, as weak economic conditions influence demand more than energy transition growth

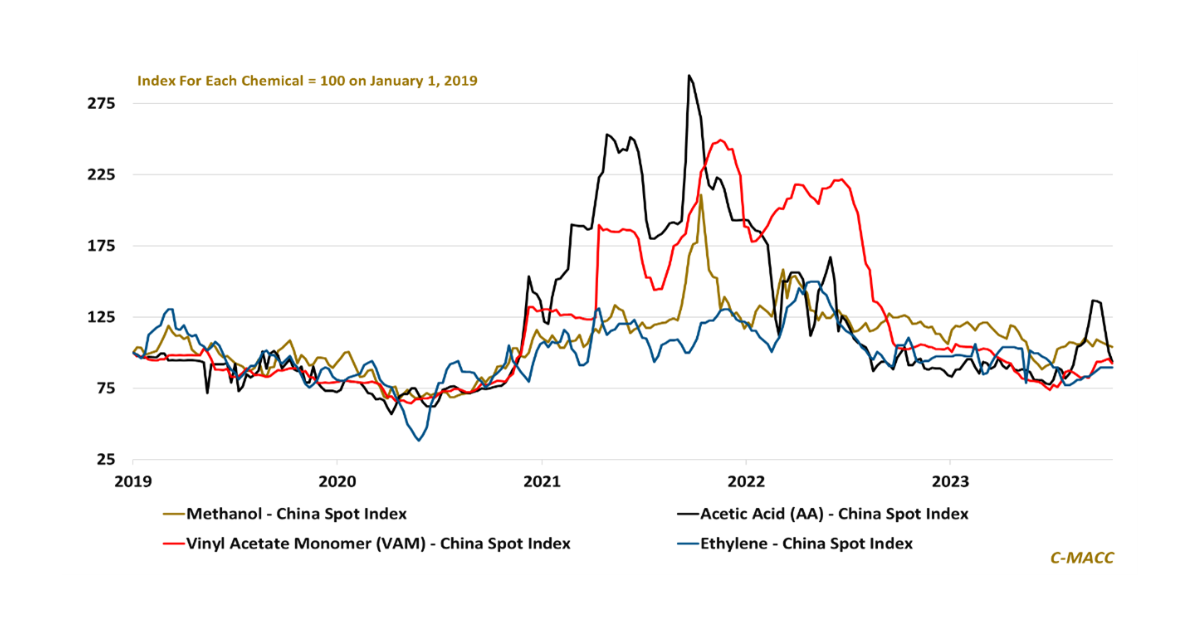

Since mid-year, the acetyl chain has experienced substantial volatility, with low-cost producers benefiting upstream and downstream benefits mixed contingent on pricing power and demand.

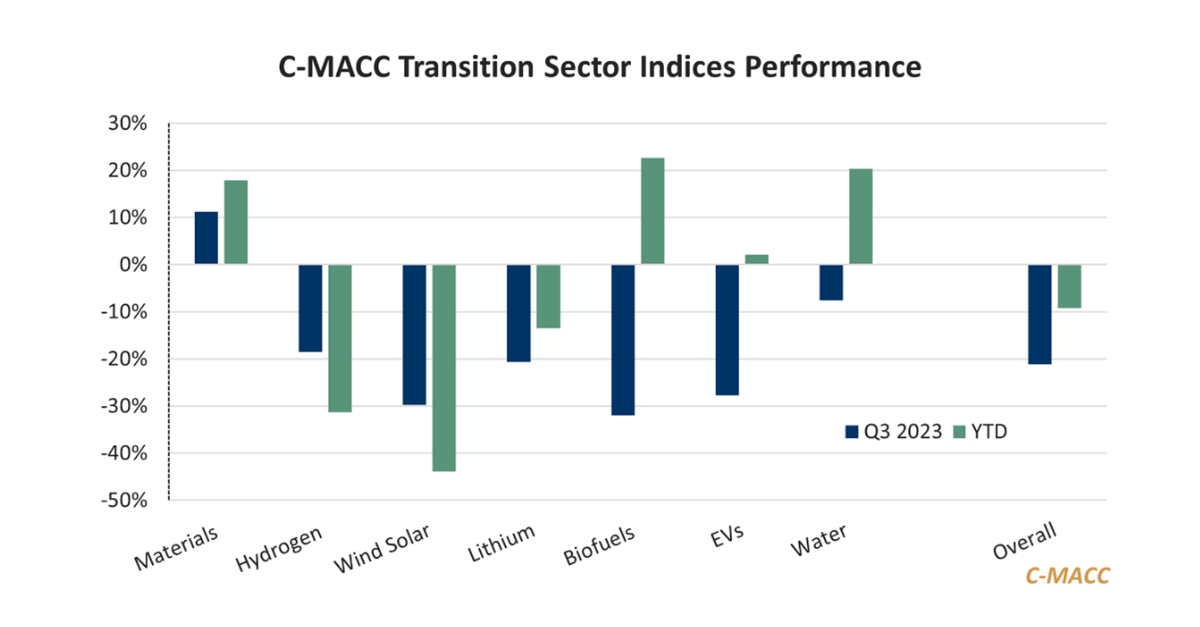

Low prices and high financing costs are stalling energy transition and chemical sector growth investments in a weak macroeconomic setting, increasingly relying on consumers for

As we approach COP28 we see the usual pick up in opinions, with multiple agencies and advisors wanting to be the most discussed view at

The decline in critical mineral prices suggests that the macroeconomic backdrop has influenced demand more than energy transition growth. Lower prices favor stalling growth investments.

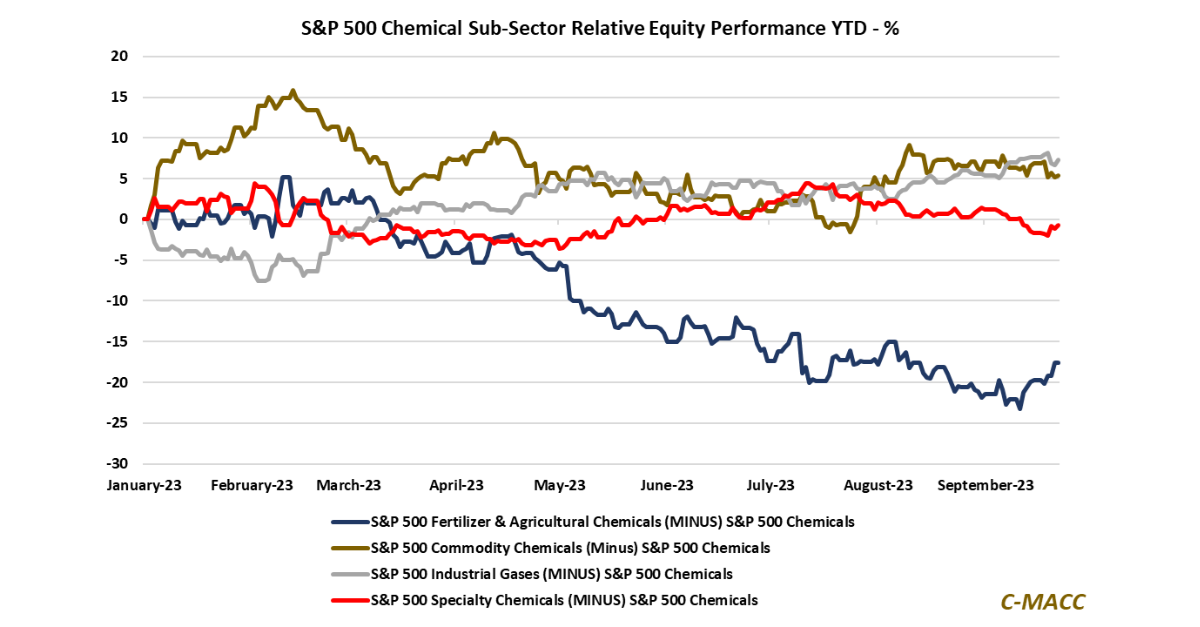

Fertilizer and agricultural chemical equities have bounced from recent lows relative to the overall S&P Chemicals index, led by rising underlying commodity prices, such as

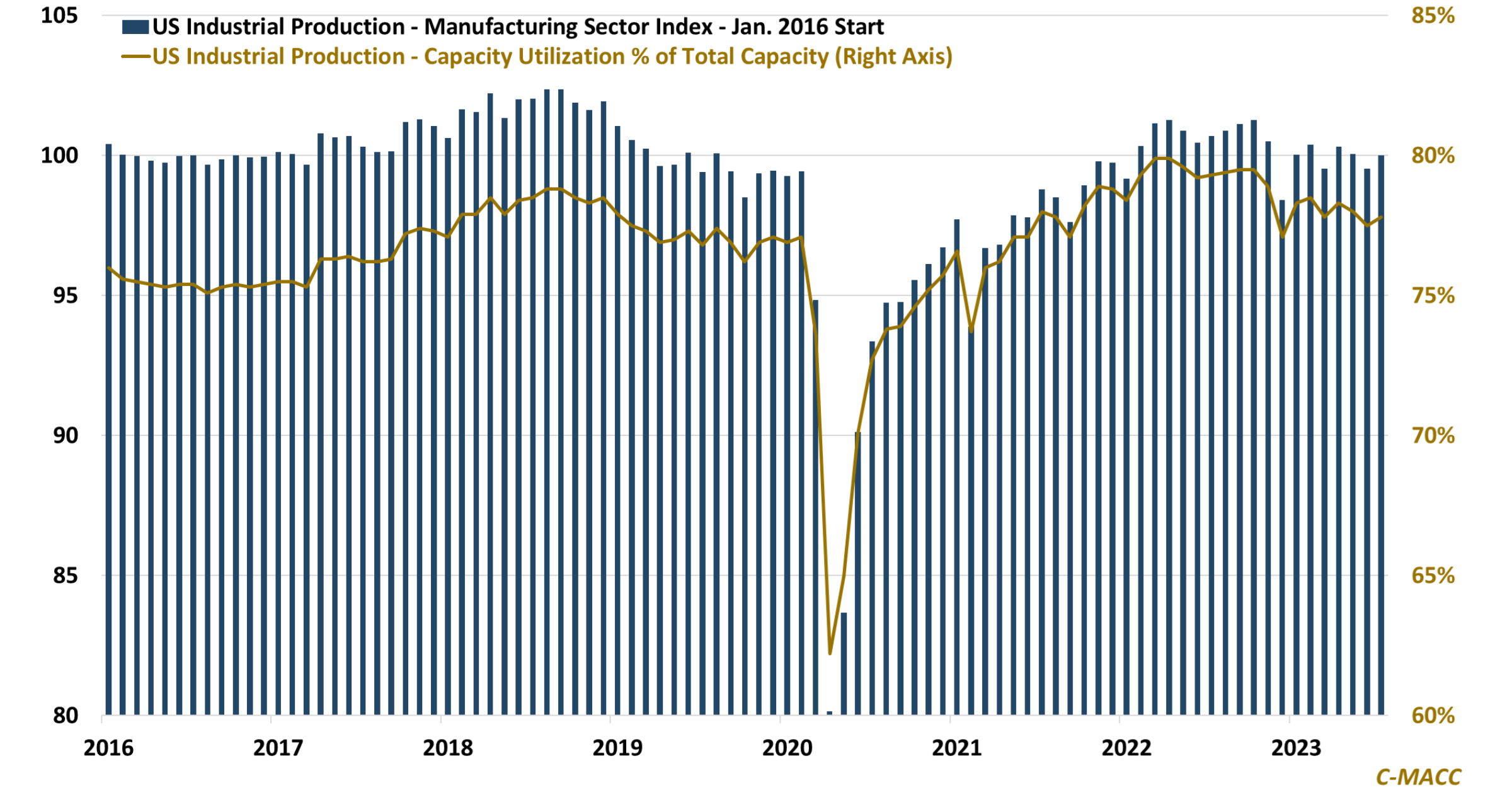

US industrial production remained lower YoY in July due to oversupply overshadowing its energy-advantaged cost position – Europe and Asia run rates are lower for