Global Market Analysis

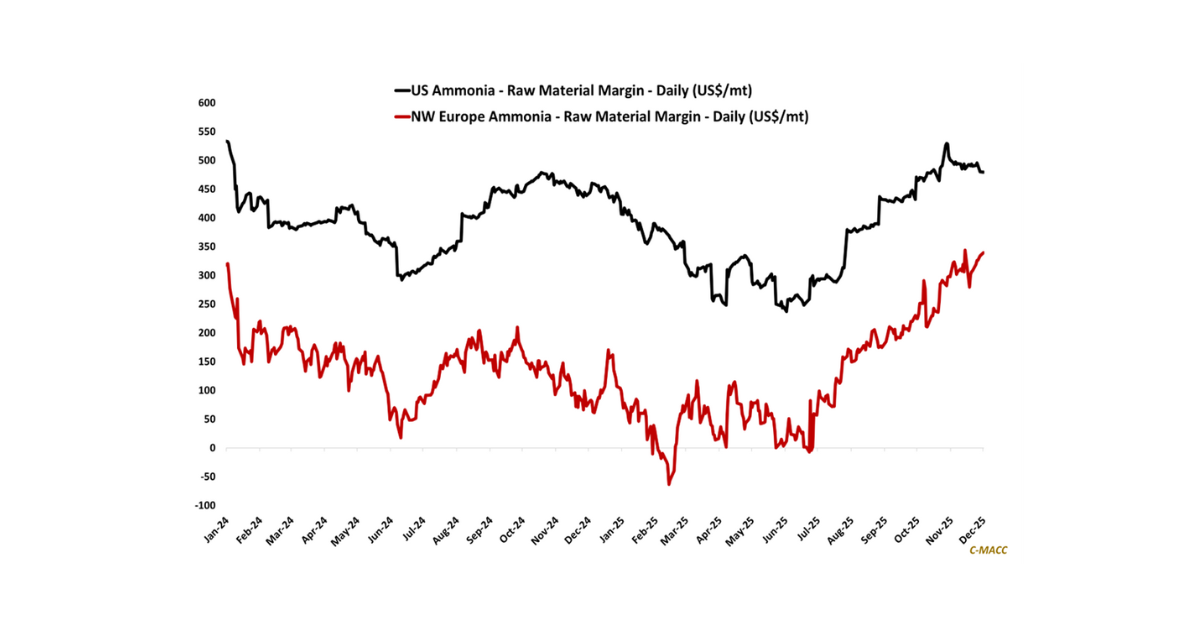

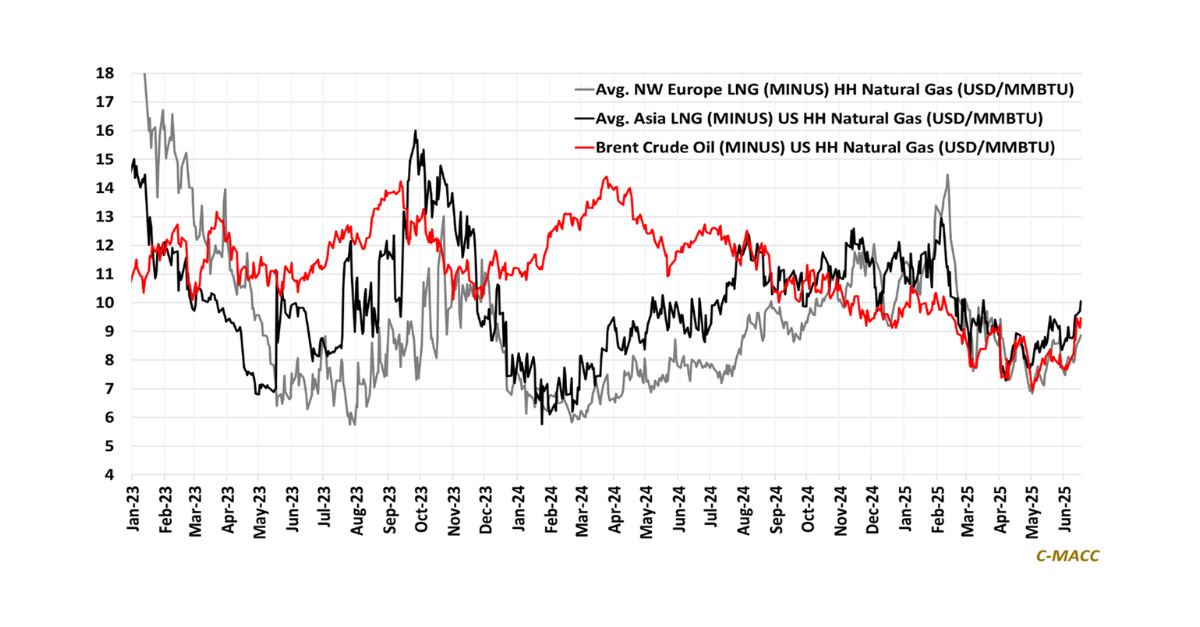

General Thoughts: Ammonia prices have surged to 2025 highs, while European and Asian natural gas prices have fallen to YTD lows relative to US levels,

General Thoughts: Ammonia prices have surged to 2025 highs, while European and Asian natural gas prices have fallen to YTD lows relative to US levels,

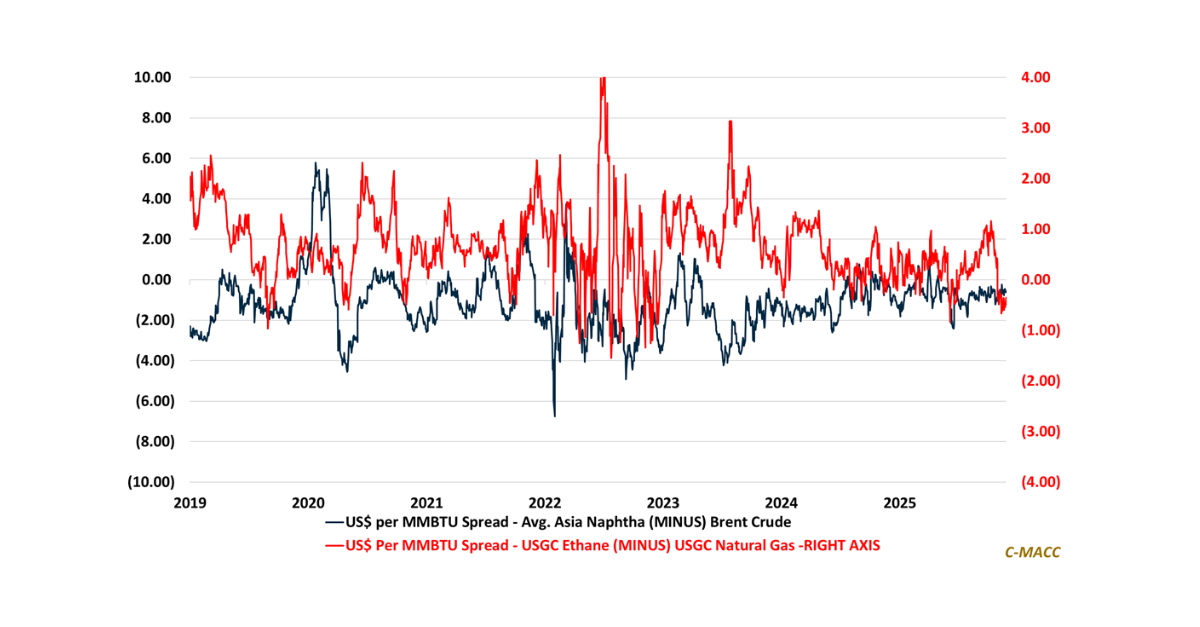

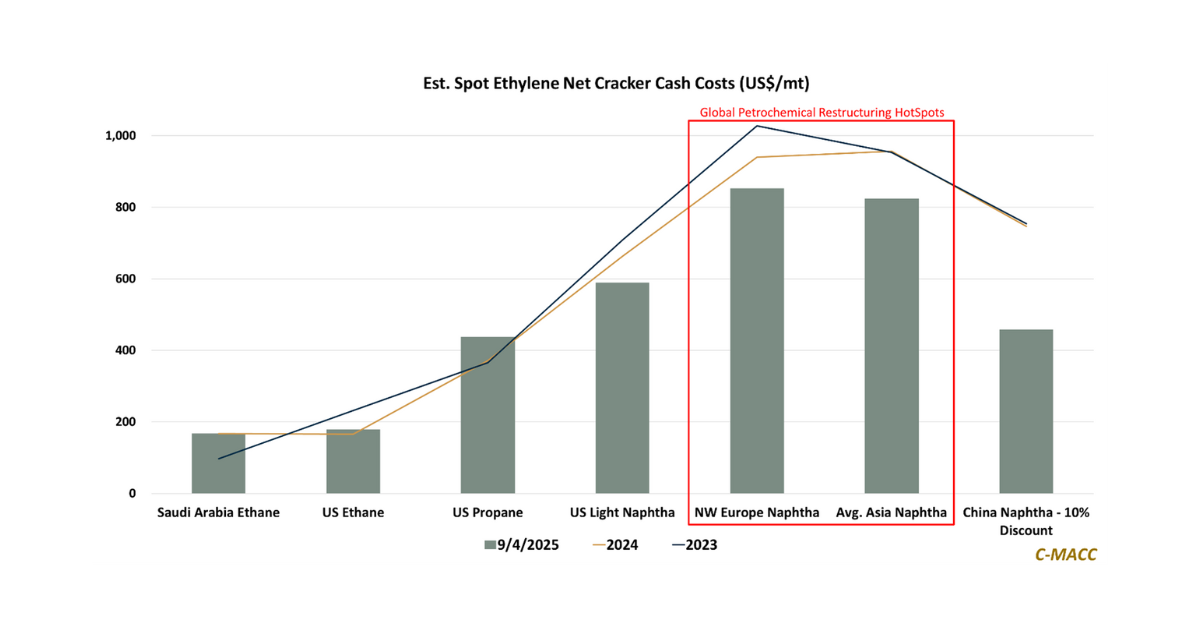

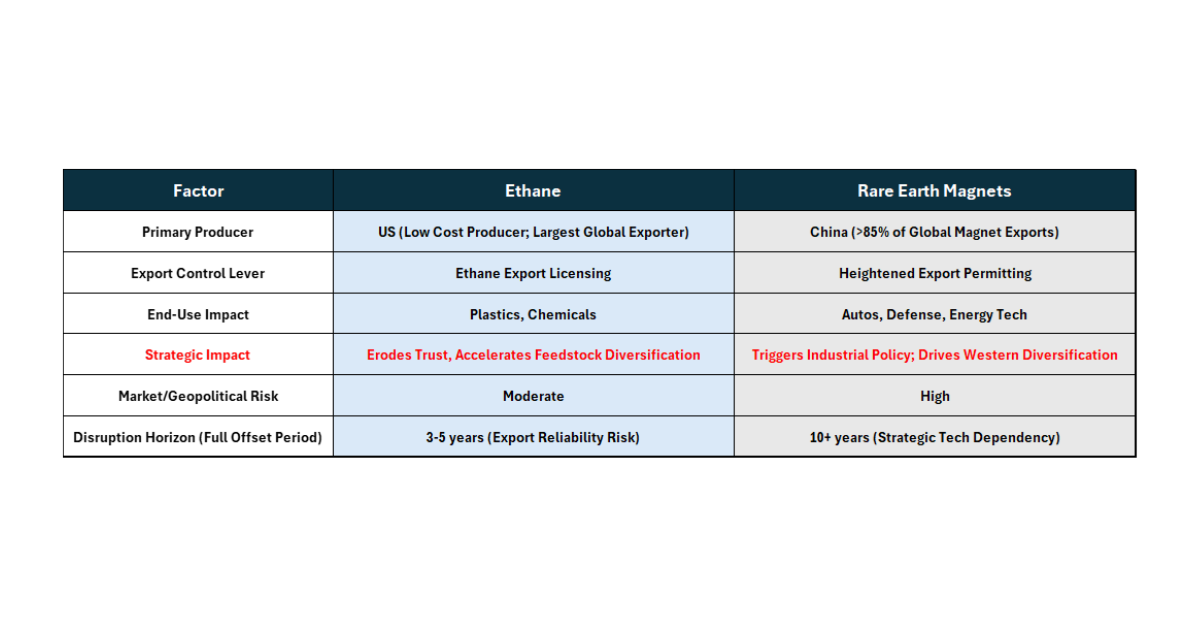

General Thoughts: Feedstock convergence, rising USGC ethane risk, and disappearing European carbon buffers accelerate petrochemical restructuring, squeezing INEOS Project One and advantaged Asian ethane importers.

Procurement-led synergy engines, not scale alone, are increasingly becoming the primary determinant of industrial competitiveness in a high-cost-capital, low-growth world increasingly defined by structural volatility.

General Thoughts: Global capital abandons volume obsession for systems resilience, rewarding platforms integrating process, certification, and proximity, transforming supply security into monetized strategic advantage.

Supply

General Thoughts: Global petrochemical markets are fragmenting into low-cost survivors and policy-backed strongholds, with capital fleeing high-cost regions and shifting to logistics, insulation, and strategic

General Thoughts: The US-EU trade deal could quietly fracture EU cracker economics by taxing co-products, lifting integrated costs, and triggering accelerated rationalization across Europe’s naphtha-based

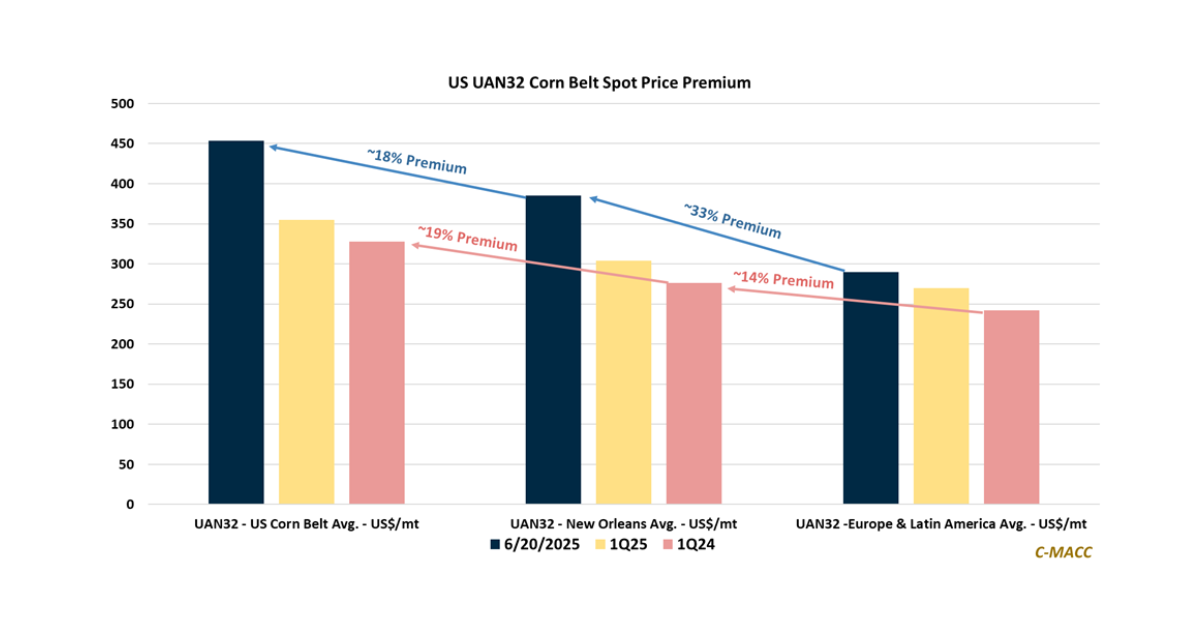

General Thoughts: Volatility demands agility in agri-energy markets, amid policy shifts and crop price fluctuations, which create headwinds likely to hurt ammonia market sentiment, despite

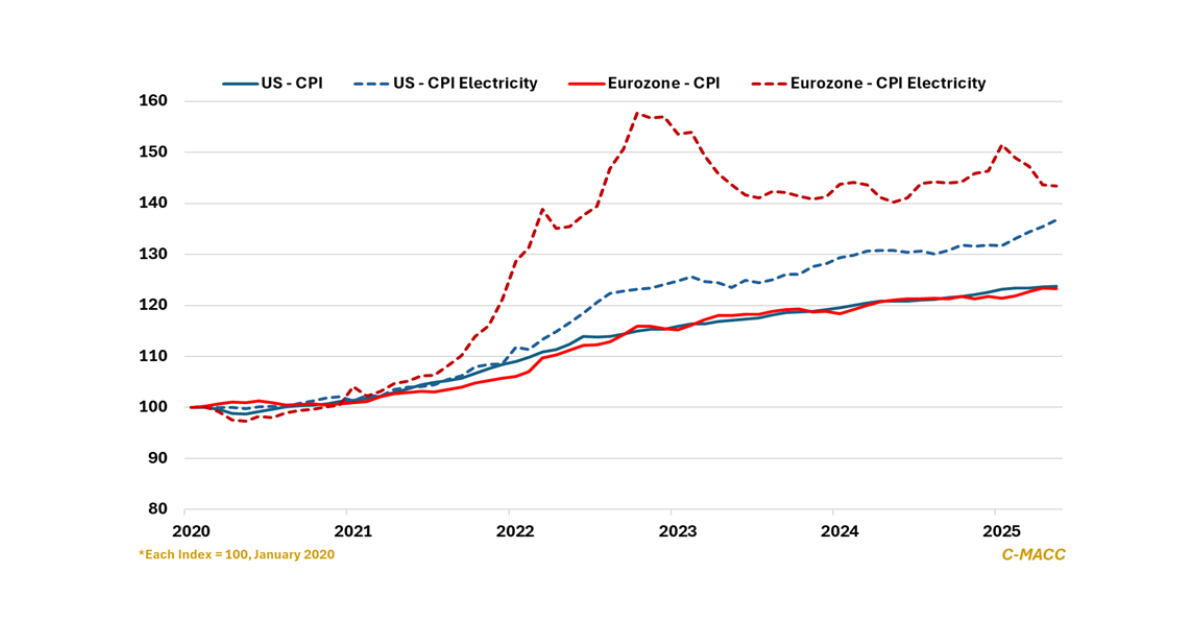

Despite a ~70% natural gas cost advantage and a robust renewables build, the US electricity CPI has climbed since January 2020 to nearly parallel that

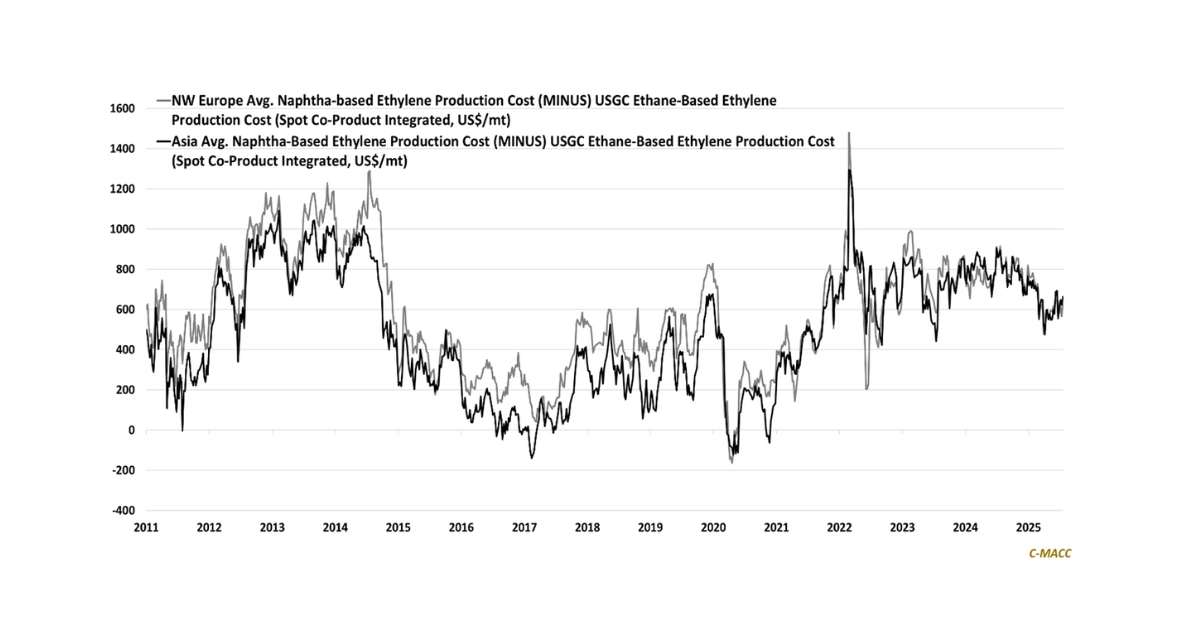

General Thoughts: Despite anticipated post-conflict oil and gas price easing, steepening global feedstock cost curves enhance US petrochemical export potential, while high-cost Asia and Europe

General Thoughts: Well-capitalized firms will capitalize on policy-driven dislocations, as increasing resource nationalism fosters global supply chain diversification, rewarding scale, trust, and strategic optionality.

Supply