Global Market Analysis

Scarcity, Sovereignty and Security – Can Energy’s Strategic Imperatives Align?

Key Findings

- General Thoughts: Despite anticipated post-conflict oil and gas price easing, steepening global feedstock cost curves enhance US petrochemical export potential, while high-cost Asia and Europe face margin compression.

- Supply Chain/Commodities: Big Oil’s Smackover plays and direct-lithium extraction (DLE) expansions position to capture resource premium margins, undercutting higher-cost rivals and reshaping critical-minerals supply chains.

- Energy/Upstream: The IEA estimates that petrochemical feedstocks will rise from 15.8% to 17.4% of global oil consumption by 2030, reflecting their importance as a driver of oil demand and in energy sector strategic reviews.

- Sustainability/Energy Transition: Low headline $/MWh masks the low effective load-carrying capability of and grid upgrade burden of renewables, compelling a mix of intermittent and firm-power sources for resilient supply.

- Downstream/Other Chemicals: The pending July 9 tariff cliff threatens 50% duties, driving EU exporters to front-load shipments to the US. The ifo Institute expects Germany’s GDP growth to show modest gains through 2025.

We will not publish a report on Thursday, June 19, as it falls on the Juneteenth holiday in the United States.

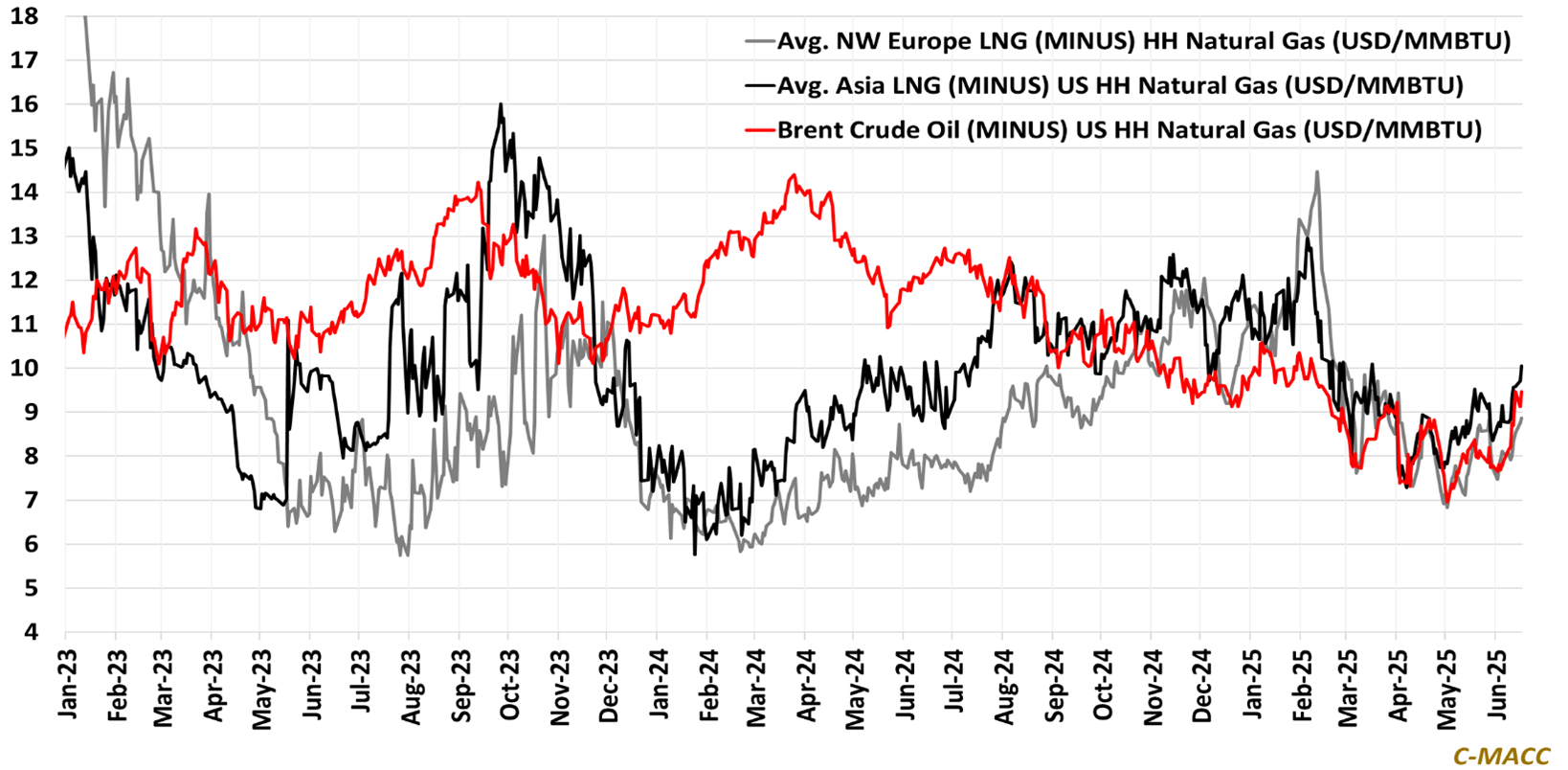

Exhibit 1: Global chemical feedstock movement implies a steepening cost curve, a plus for North American chemicals.

Source: Bloomberg, C-MACC Analysis, June 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!