Sunday Executive Summary

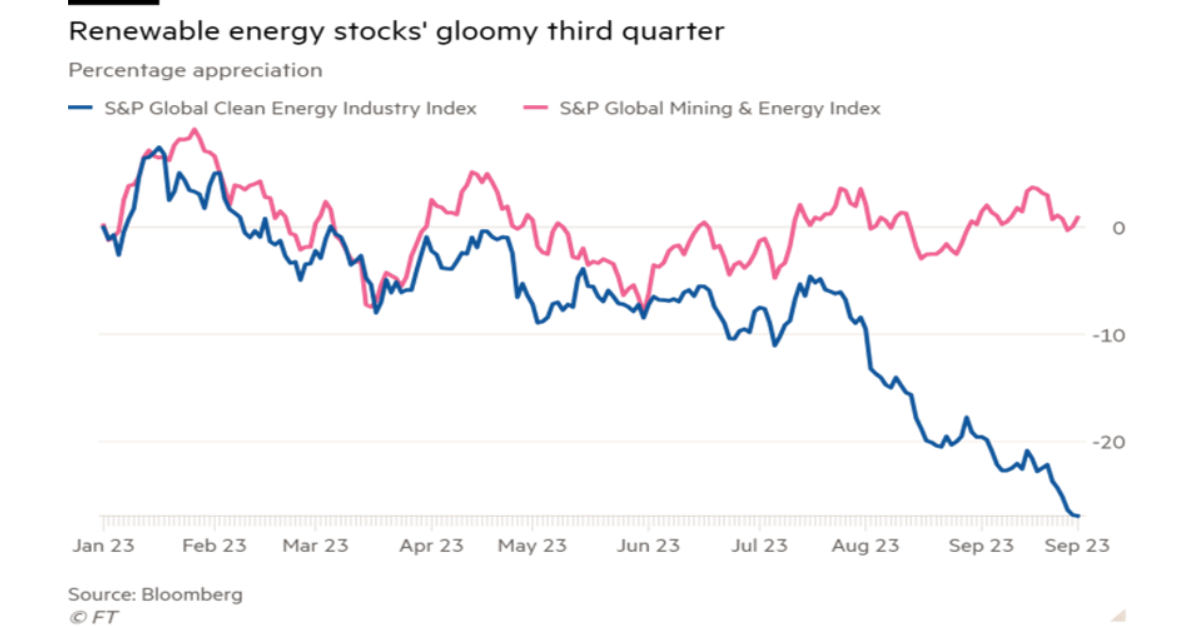

In our view, those calling for a quick end to fossil fuel use and simultaneously vilifying the oil and gas industry are likely condemning energy

In our view, those calling for a quick end to fossil fuel use and simultaneously vilifying the oil and gas industry are likely condemning energy

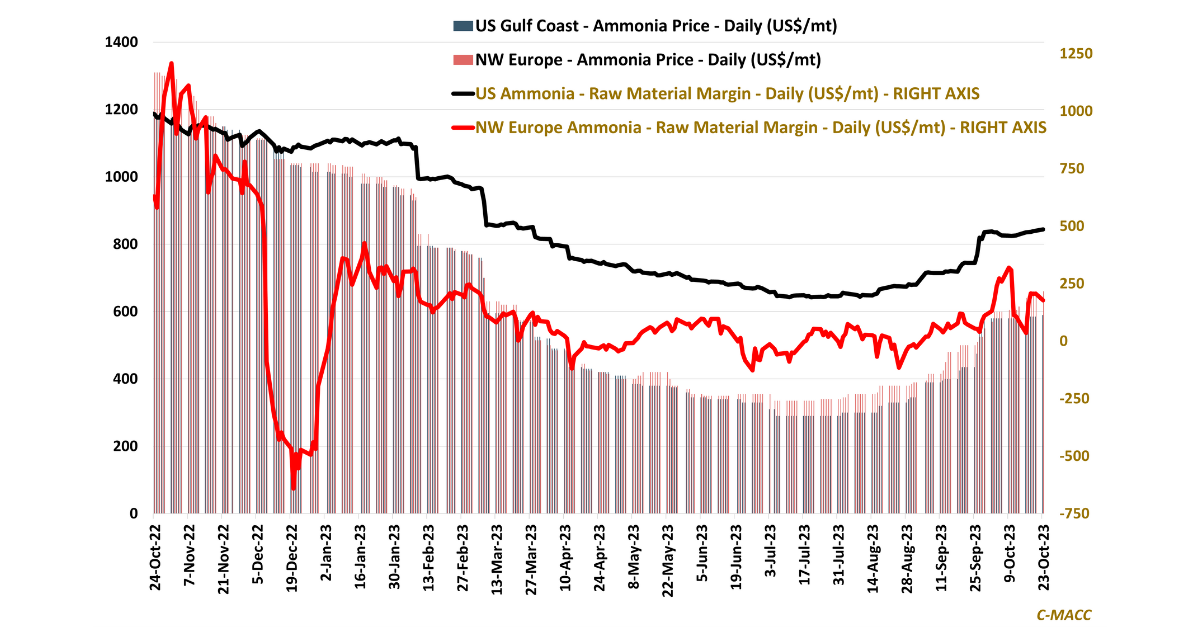

Global ammonia prices have risen QTD in 4Q23, led higher by supportive end-demand and increased Ex-US natural gas costs relative to US levels. We view

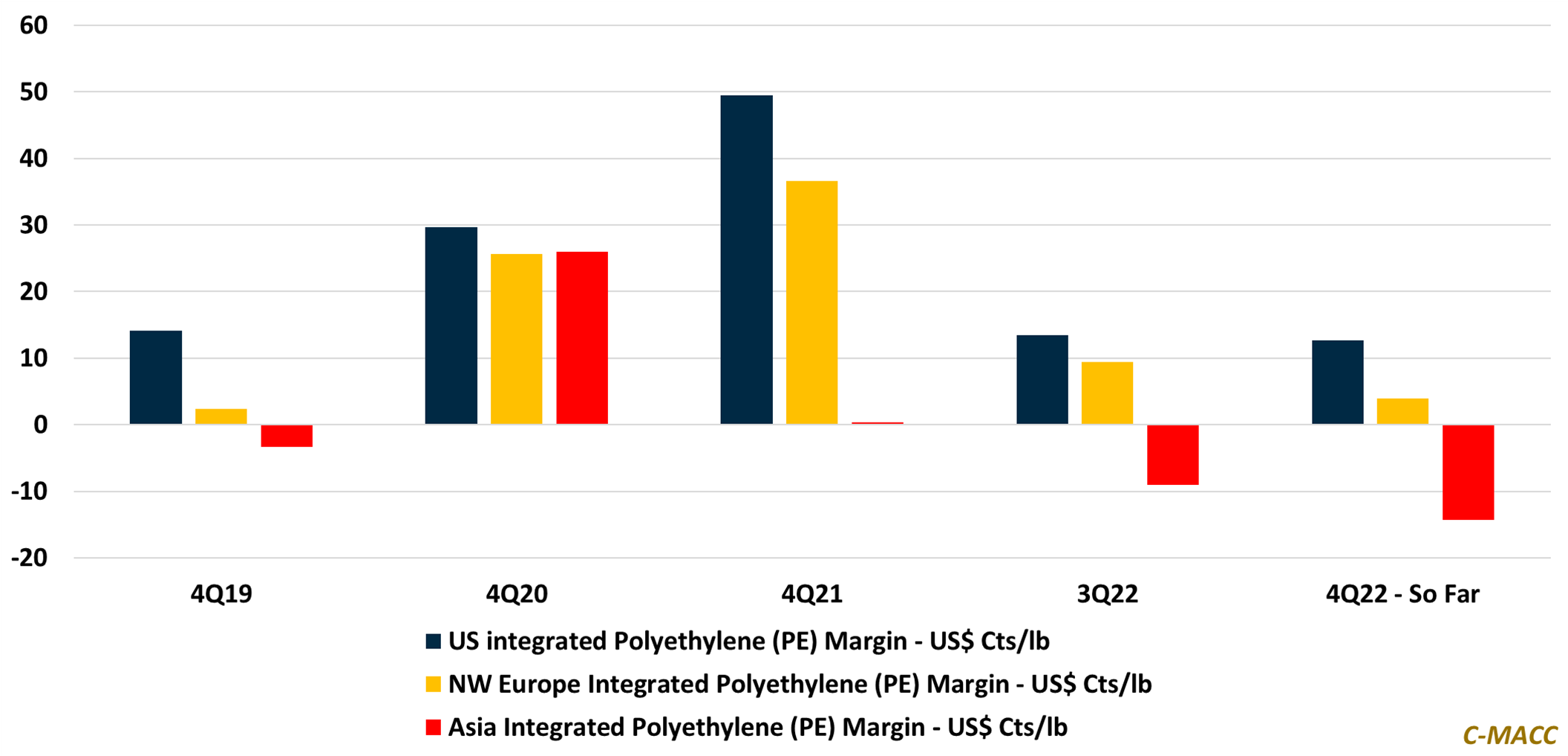

2023 is off to a bad start with low margins (but maybe not low enough) and global operating rates reflecting significant oversupply, which could worsen.

European chemical producer cutbacks will unlikely offset oversupplied Asian markets to support prices into 2023, limiting US cost benefits and forcing a battle from within.

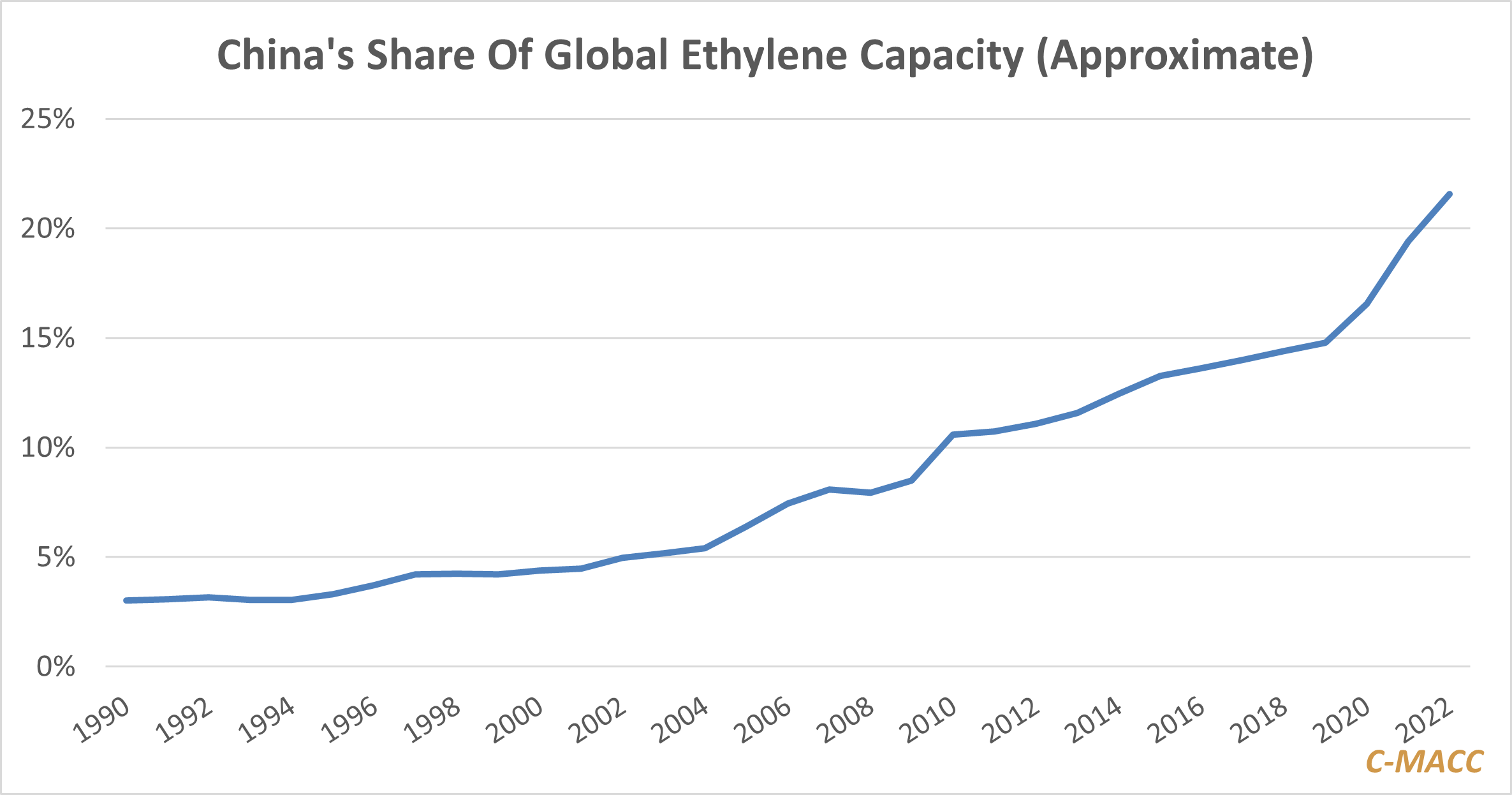

Our concerns around the fate of the global chemical industry for 2023 are now consensus, and while we are looking for what could go right

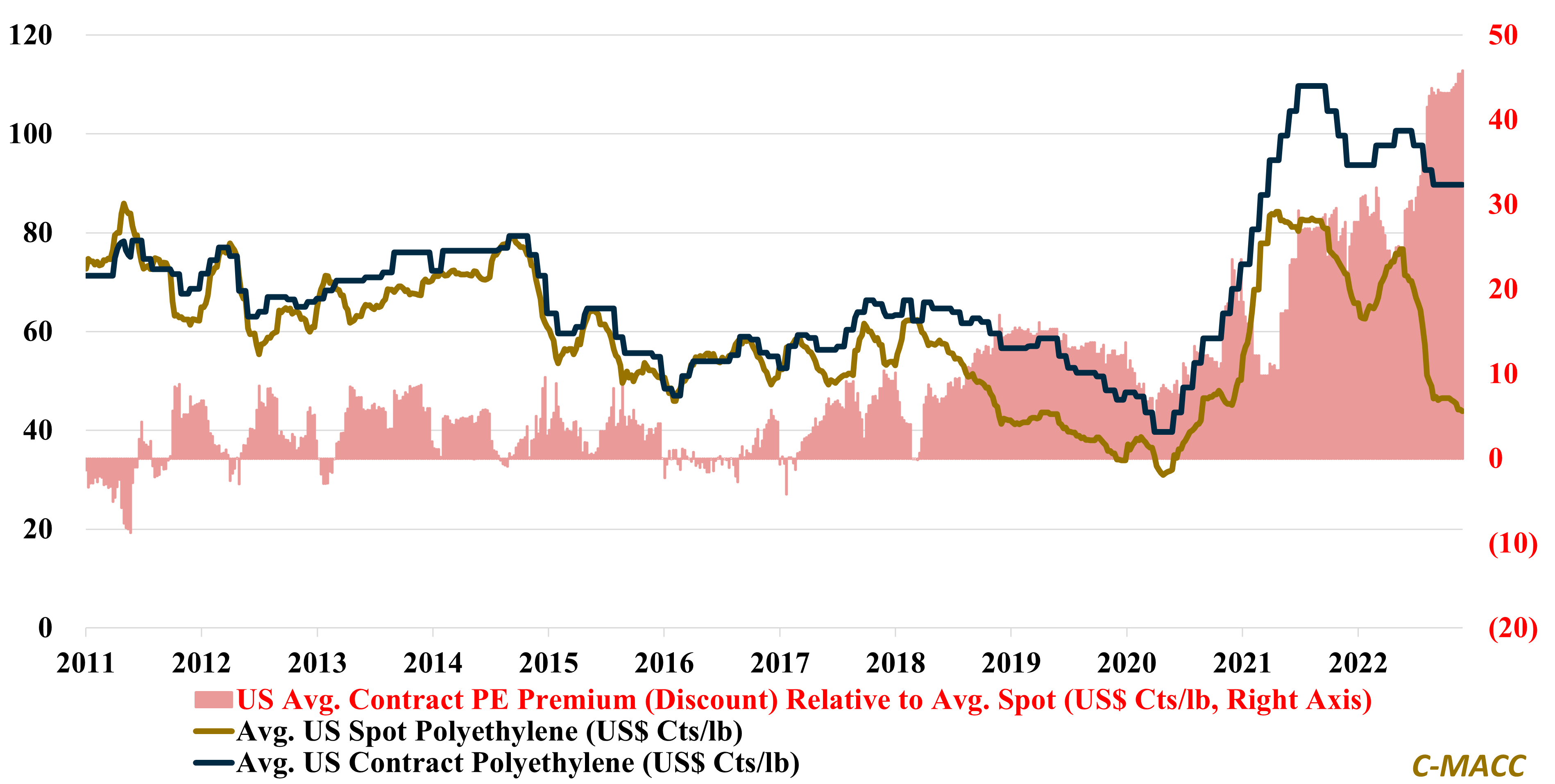

US polyethylene (PE) contract price support relative to US spot prices in 4Q has pushed the contract premium to more than a 10yr high, and