Sustainability & Energy Transition

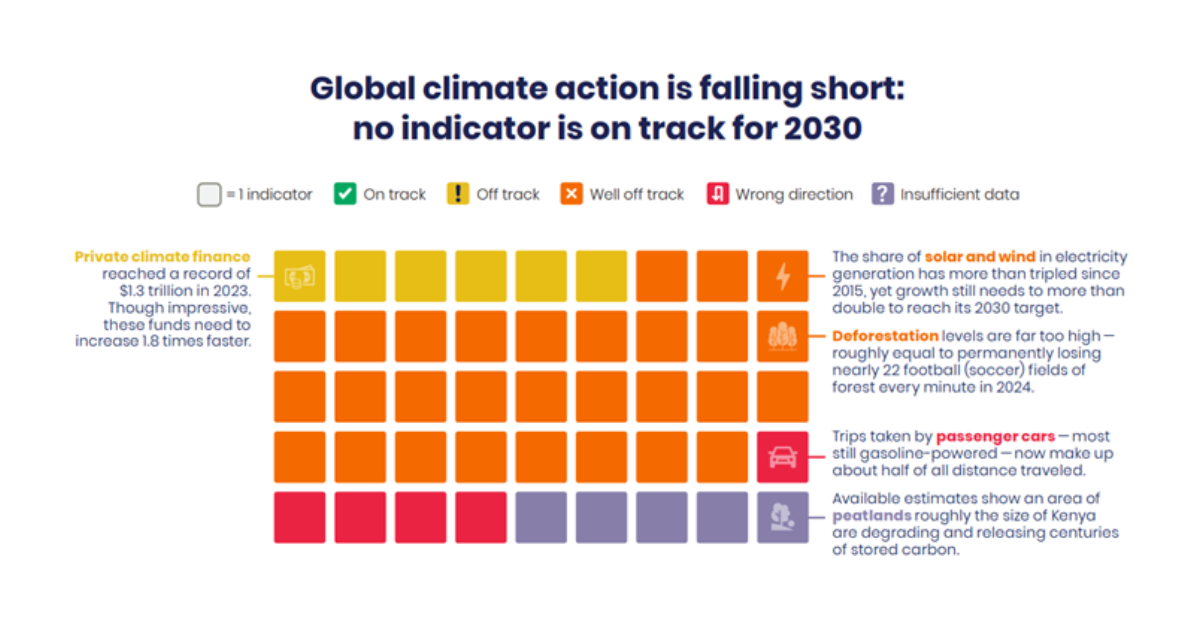

1st Topic of the Week: With COP30 exposing more global policy and compliance fractures, capital deployments across most climate strategies carry elevated risk, promoting selective

1st Topic of the Week: With COP30 exposing more global policy and compliance fractures, capital deployments across most climate strategies carry elevated risk, promoting selective

Both C-MACC co-founders will attend CERAWeek. Our initial view of the agenda suggests a heavy focus on energy transition, but other relevant themes are present.

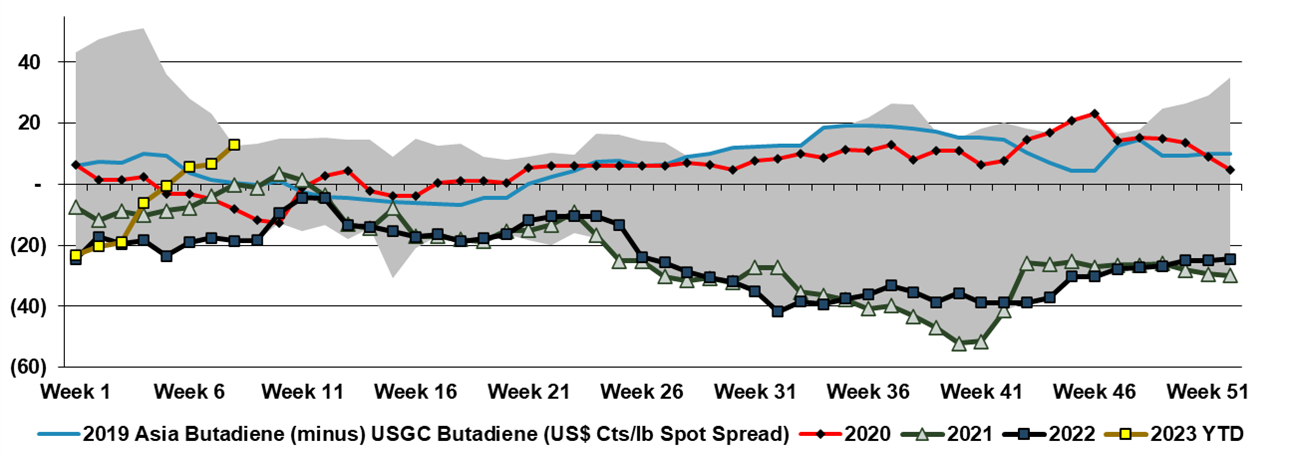

Asia spot butadiene (BD) prices have increased YTD on an absolute basis and relative to US values. We discuss the strength in BD derivatives and

Weakness in Western natural gas prices favors chemical production, lifting oversupply risk in many products, especially in areas with overly optimistic demand outlooks.

We discuss

Near-term global concerns with demand and product oversupply are overtaking the appreciation of cost curves and competitive positioning – this will eventually change.

We

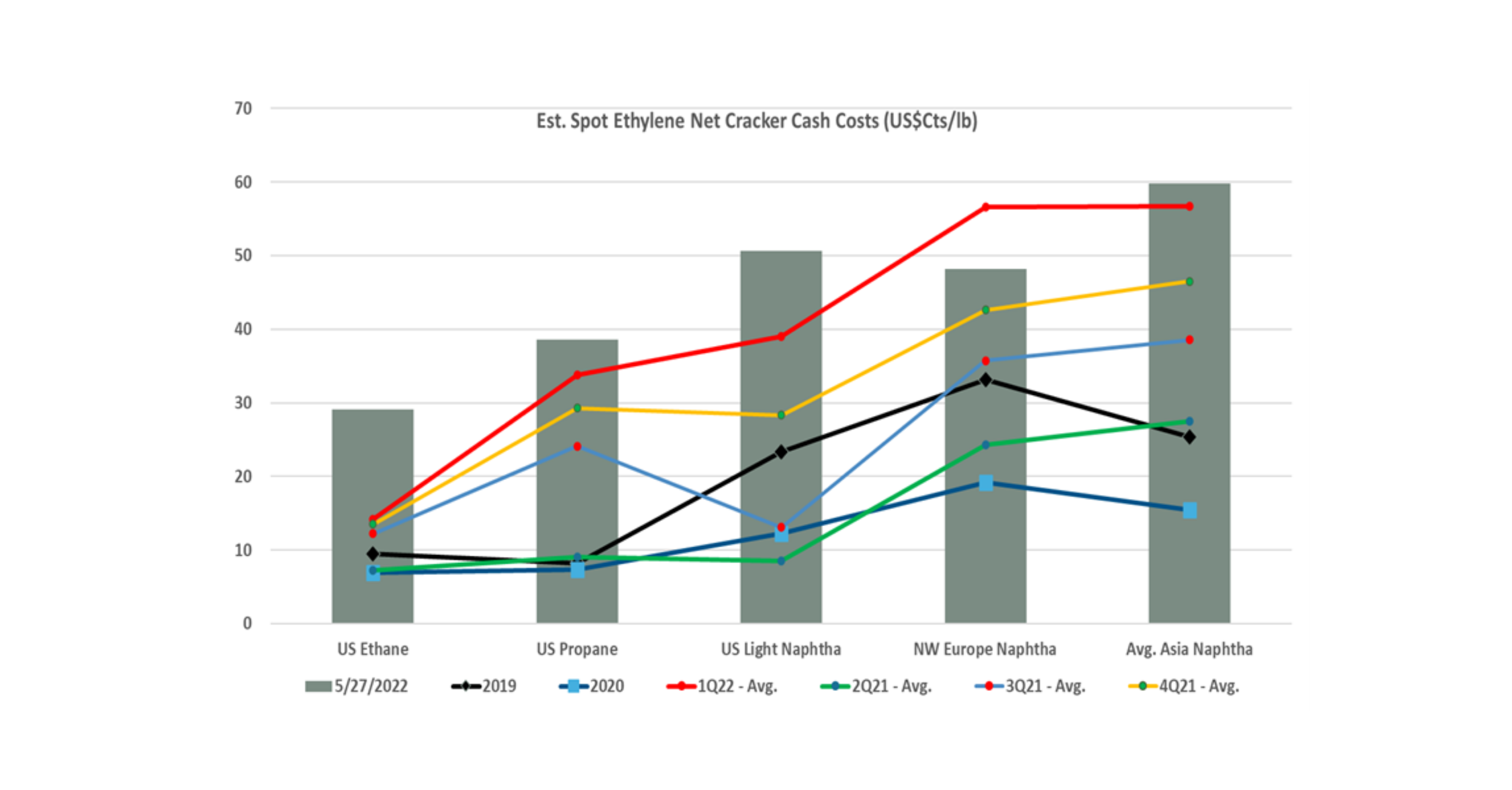

US chemical production costs on average remain advantaged relative to Ex-US peers. We discuss potential projects in Orange County, TX, recent global sector M&A, and

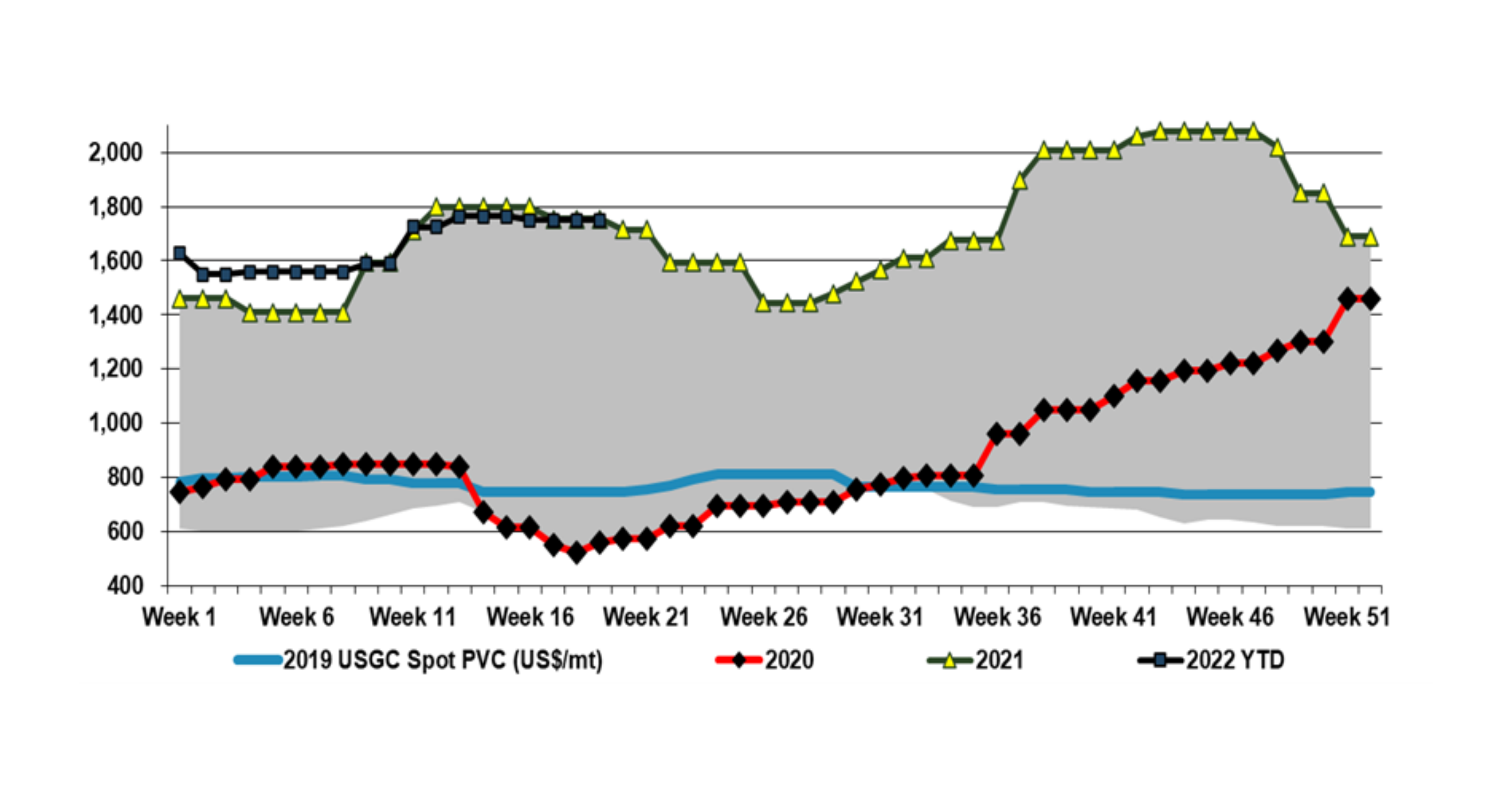

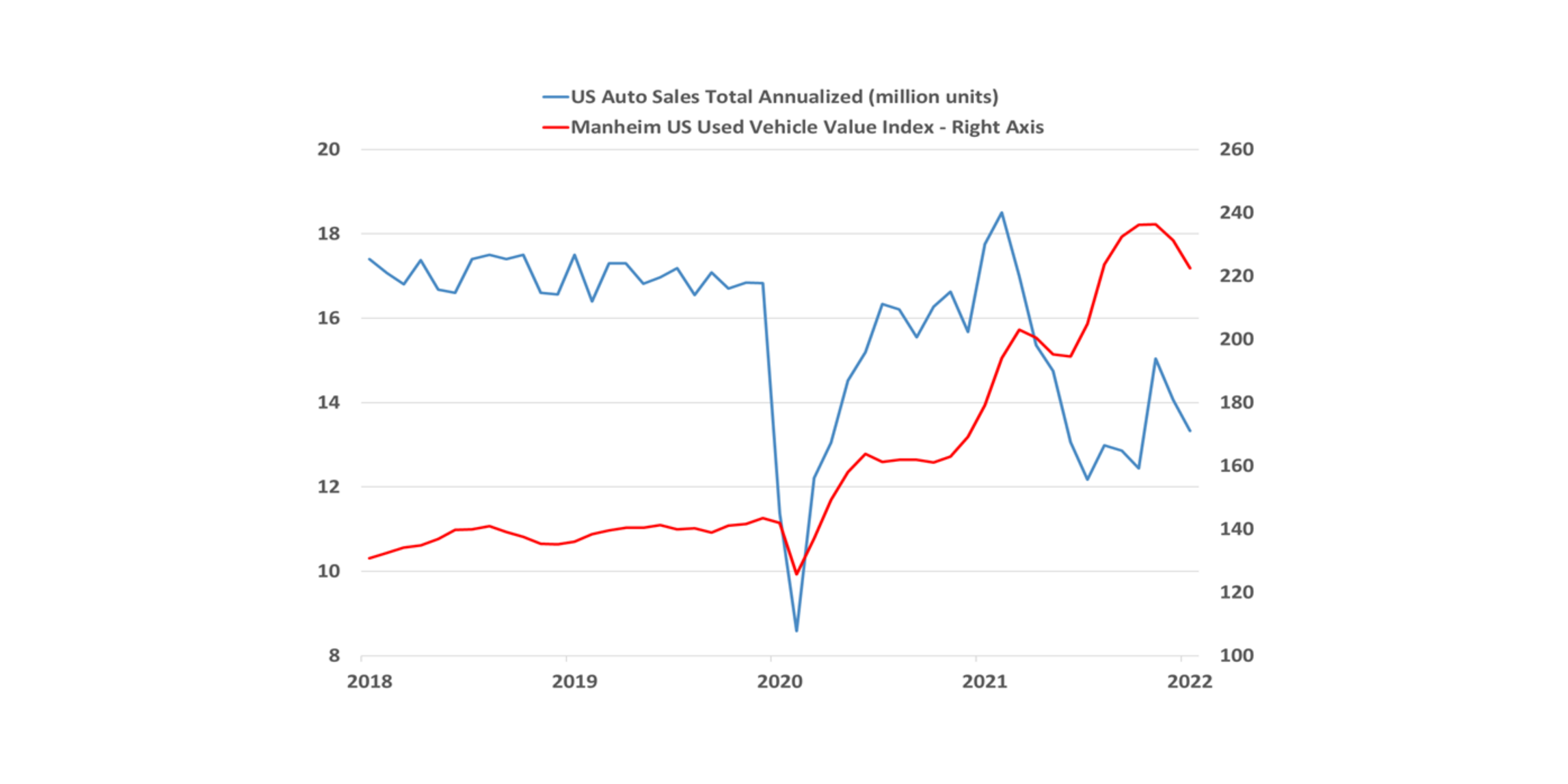

Chemical product chain profitability mostly turned negative in 1H22 due to higher costs not being fully factored into lagging end-product prices. We highlight a few

Chemical price hike initiatives to recapture margin amid cost inflation and material shortages are in motion while consumer demand headwinds continue to mount. We discuss

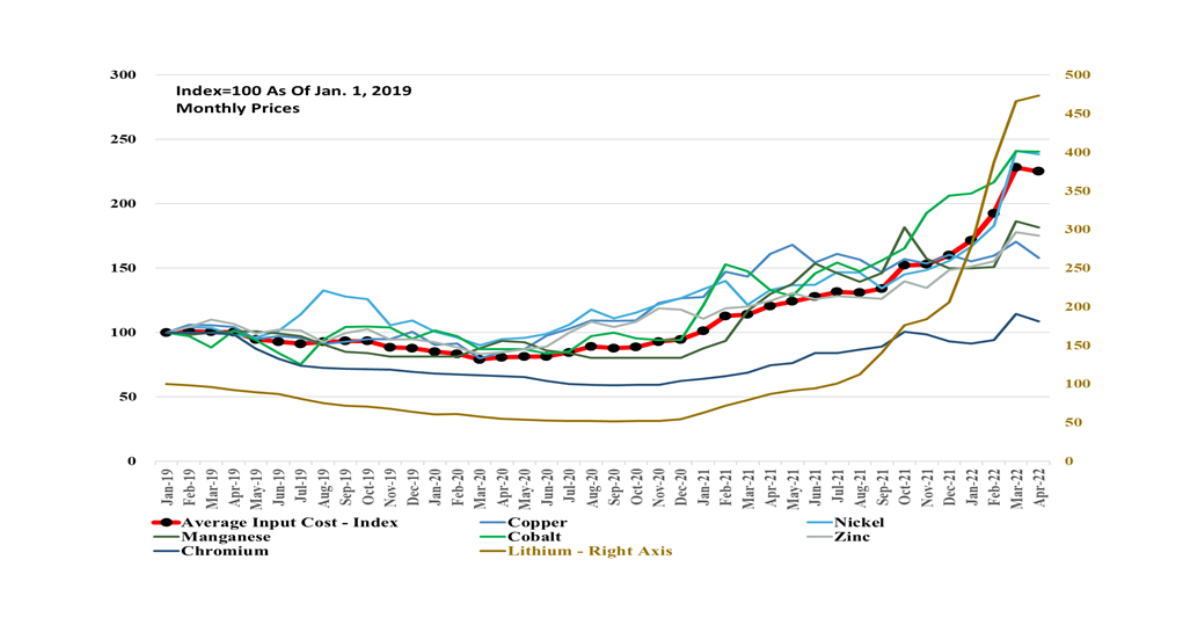

Our clean energy mineral price index declined MoM in April, following significant sequential strength since 3Q21. We update our broader market views and flag several

Industry reports continue to target strong demand, tight supply chains, & input sourcing issues, but some end-market health indicators are cooling off. We discuss recent