Global Market Analysis

Corn To Be Wild – Low-Cost Ammonia Producers Set to Enjoy the Dancing, As Corn Buyers Brawl Outside!

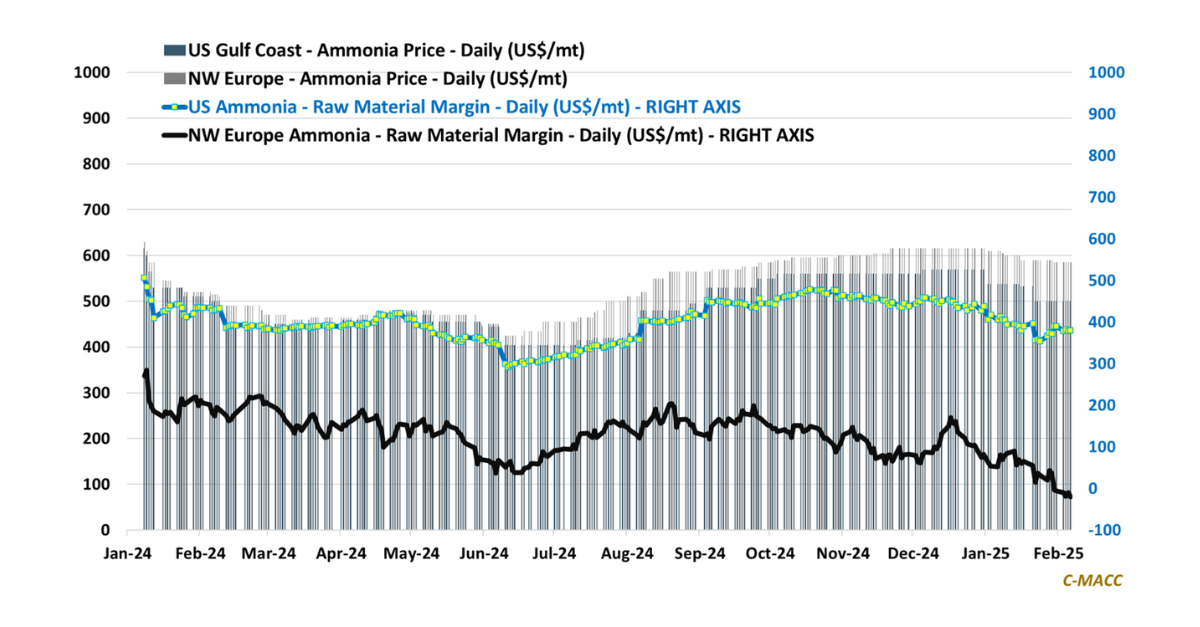

General Thoughts: We maintain a more constructive view of crop prices in 1Q25 than agriculture sector equities overall, and we continue to favor crop input