Global Market Analysis

Corn To Be Wild – Low-Cost Ammonia Producers Set to Enjoy the Dancing, As Corn Buyers Brawl Outside!

Key Findings

- General Thoughts: We maintain a more constructive view of crop prices in 1Q25 than agriculture sector equities overall, and we continue to favor crop input (seed, fertilizer, etc.) providers relative to crop consumers in 2025/26.

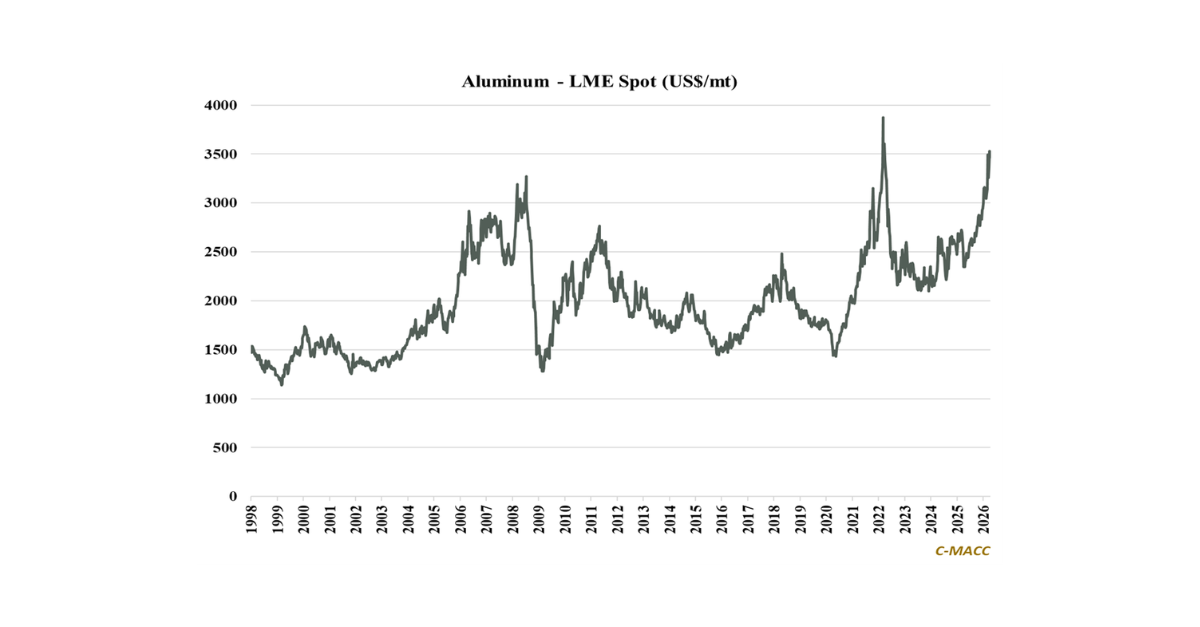

- Supply Chain/Commodities: We flag a few takeaways from the Corteva 4Q24 earnings call and discuss corn price strength and EU natural gas prices rising relative to US levels – positive developments for US ammonia producers.

- Energy/Upstream: We flag BP’s efforts to sell its Gelsenkirchen, Germany refinery and petrochemical assets, including ethylene crackers, and show a general view of the global average refinery and ethylene cracker margins.

- Sustainability/Energy Transition: US ethanol exports set a record in 2024, but policy uncertainty and low-to-no margins have spurred concerns for 2025 – higher ethanol prices to offset corn costs are needed to lift returns.

- Downstream/Other Chemicals: The widening US trade deficit in late 2024 reflects record imports and shifting export trends, with tariff and policy shifts reflecting risk to our commodity, including agriculture, sector view.

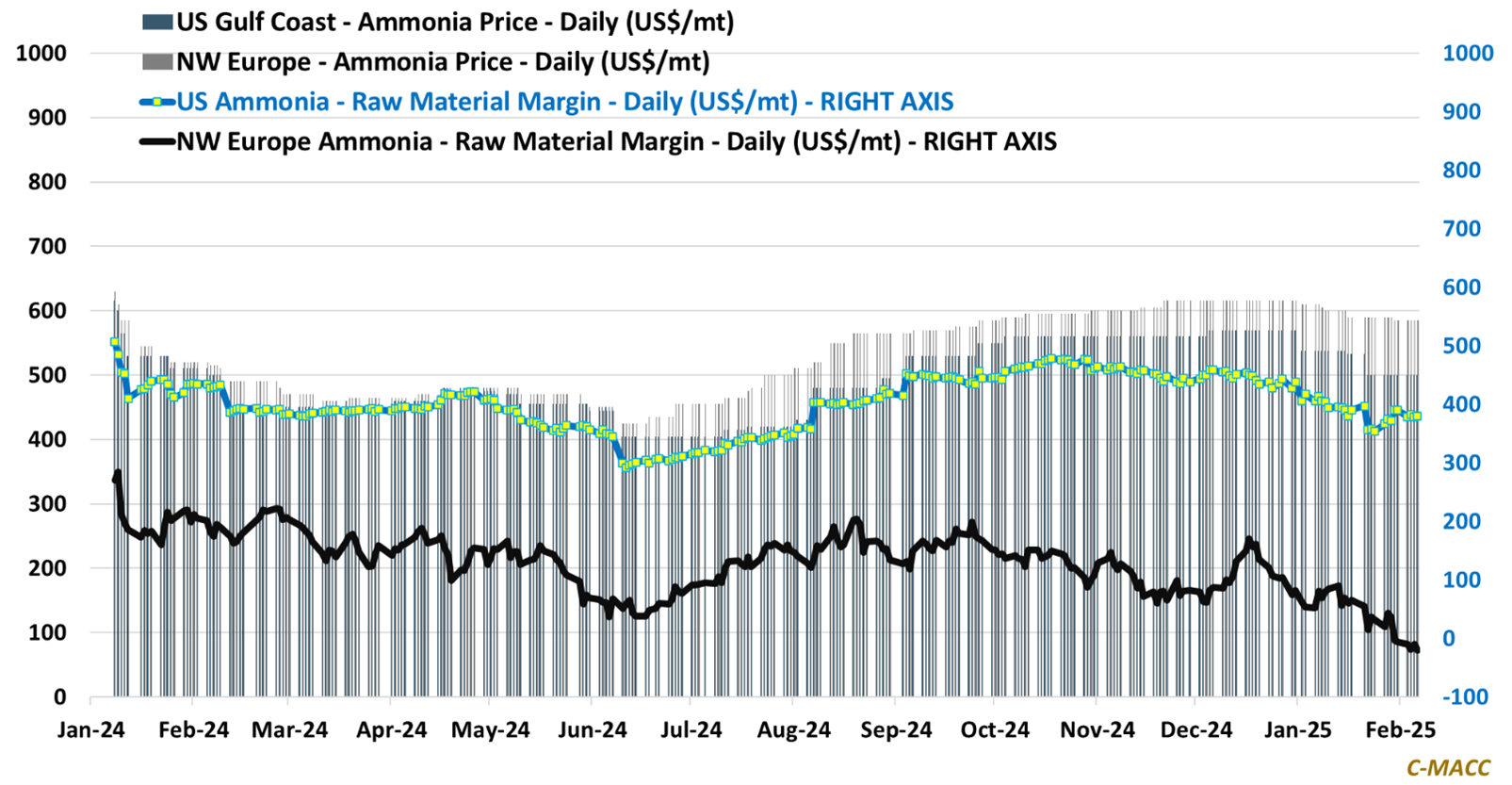

Exhibit 1: US ammonia producers could see another year of outsized margins, a plus for domestic investment.

Source: Bloomberg, C-MACC Analysis, February 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!