Global Market Analysis

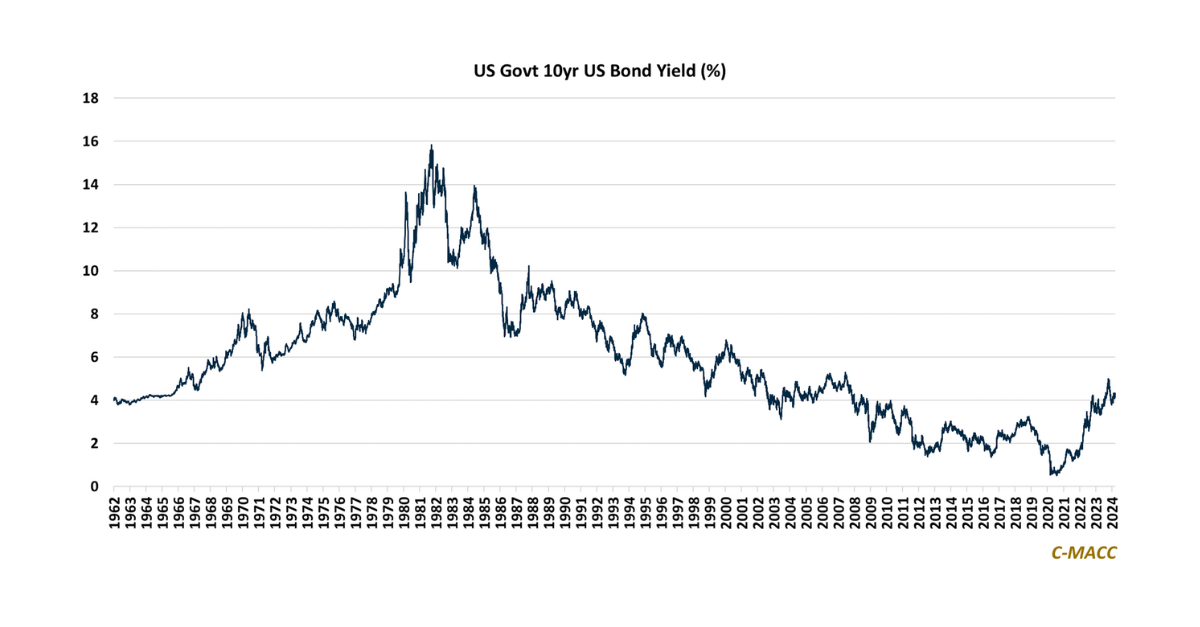

General Thoughts: Our meetings at CERA differ from last year, as our discussions are now less about concepts and more about project return challenges –

General Thoughts: Our meetings at CERA differ from last year, as our discussions are now less about concepts and more about project return challenges –

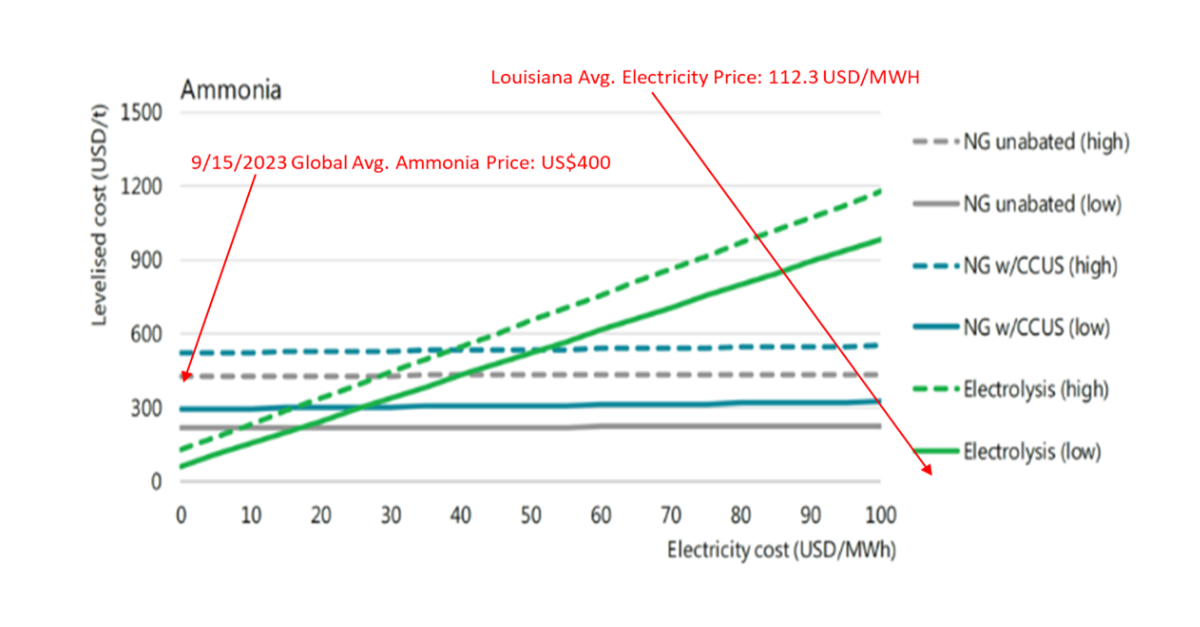

The development of clean energy globally faces considerable risk if the cost of deployments rises while fossil-fuel alternatives get cheaper – we discuss a few

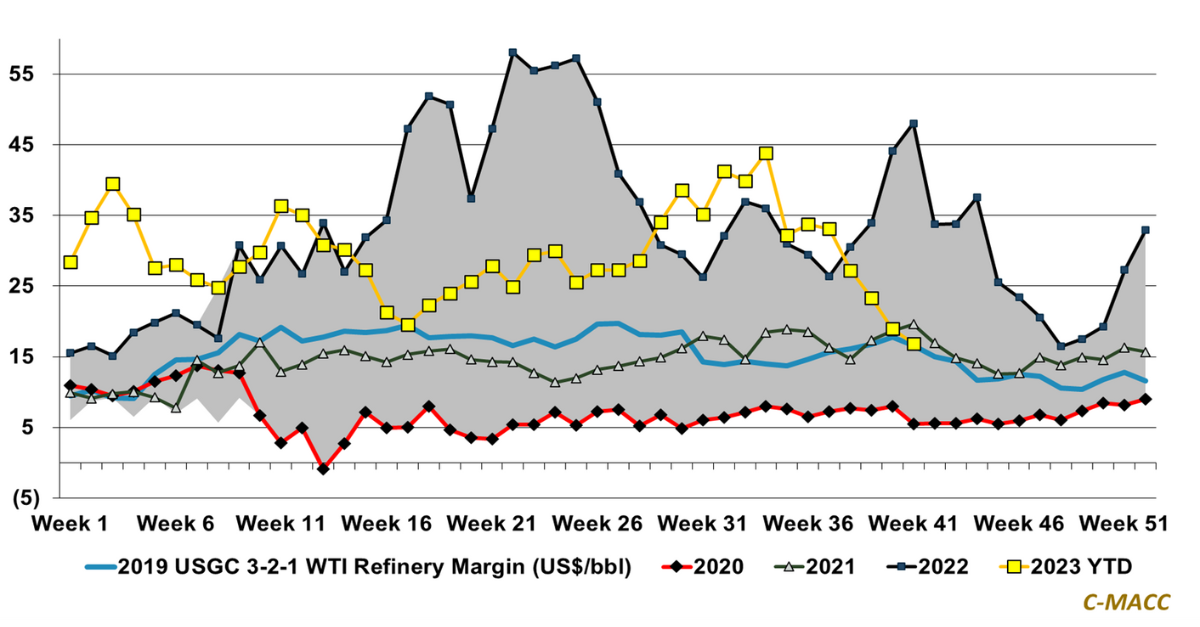

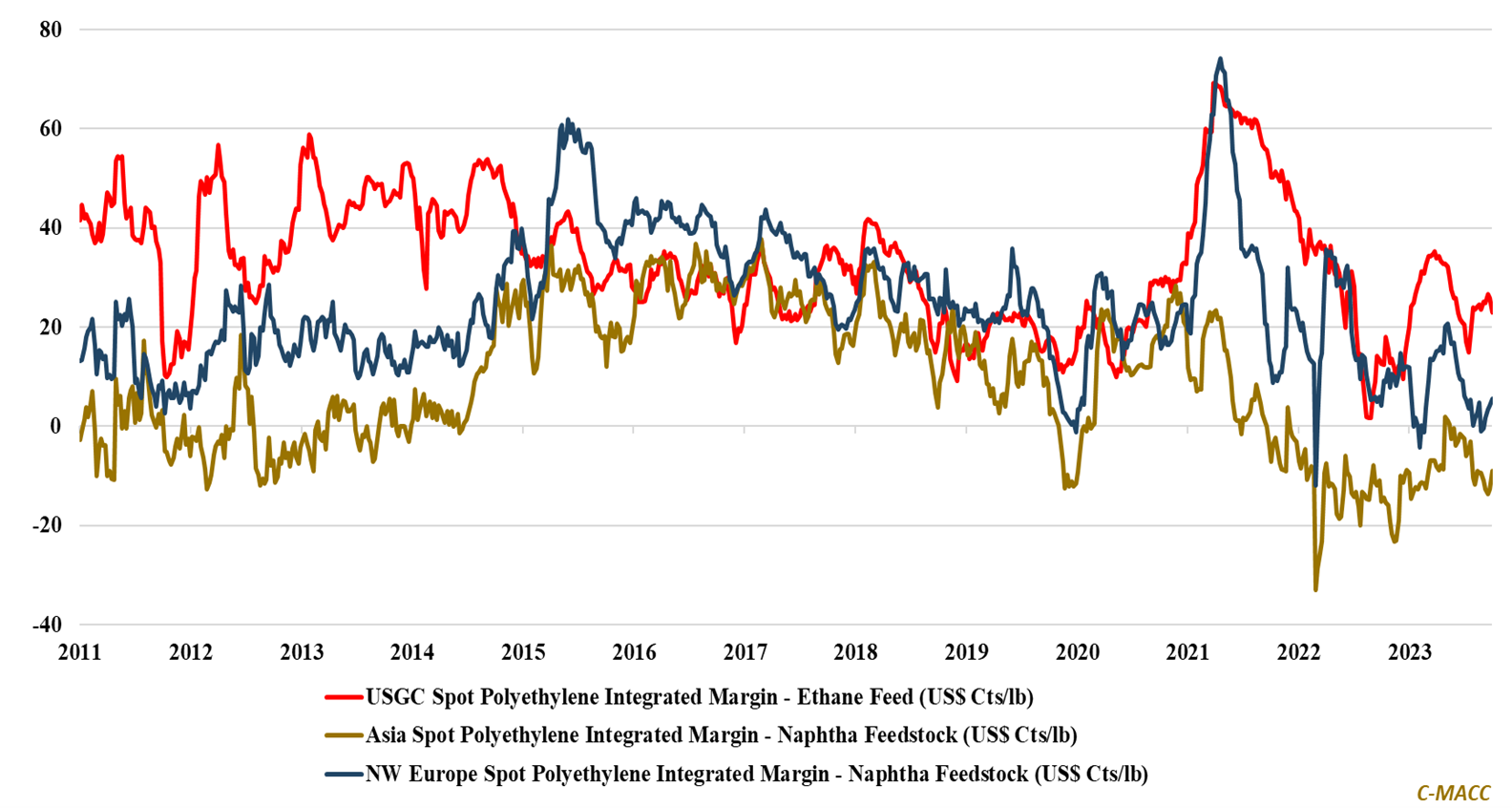

The global impact of 2H23 oil market shifts on regional integrated commodity chemical profit is less difficult to gauge than for non-integrated commodity and derivative

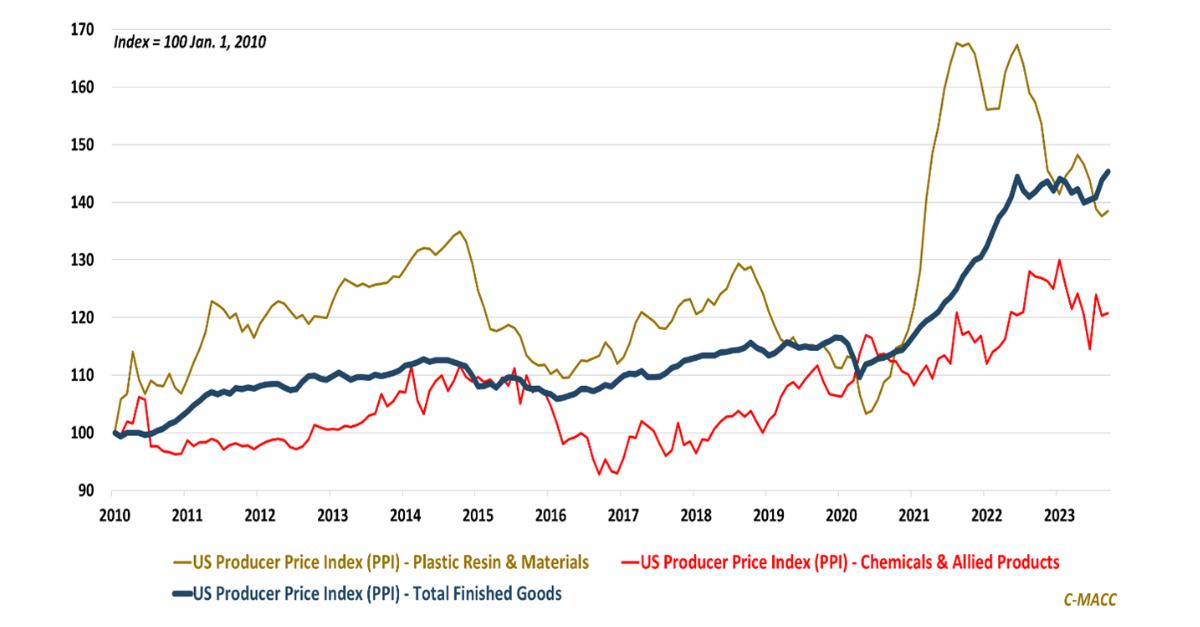

US wholesale prices rose in September due to higher energy and food costs, benefiting North American agricultural and commodity chemical producers relative to peers in

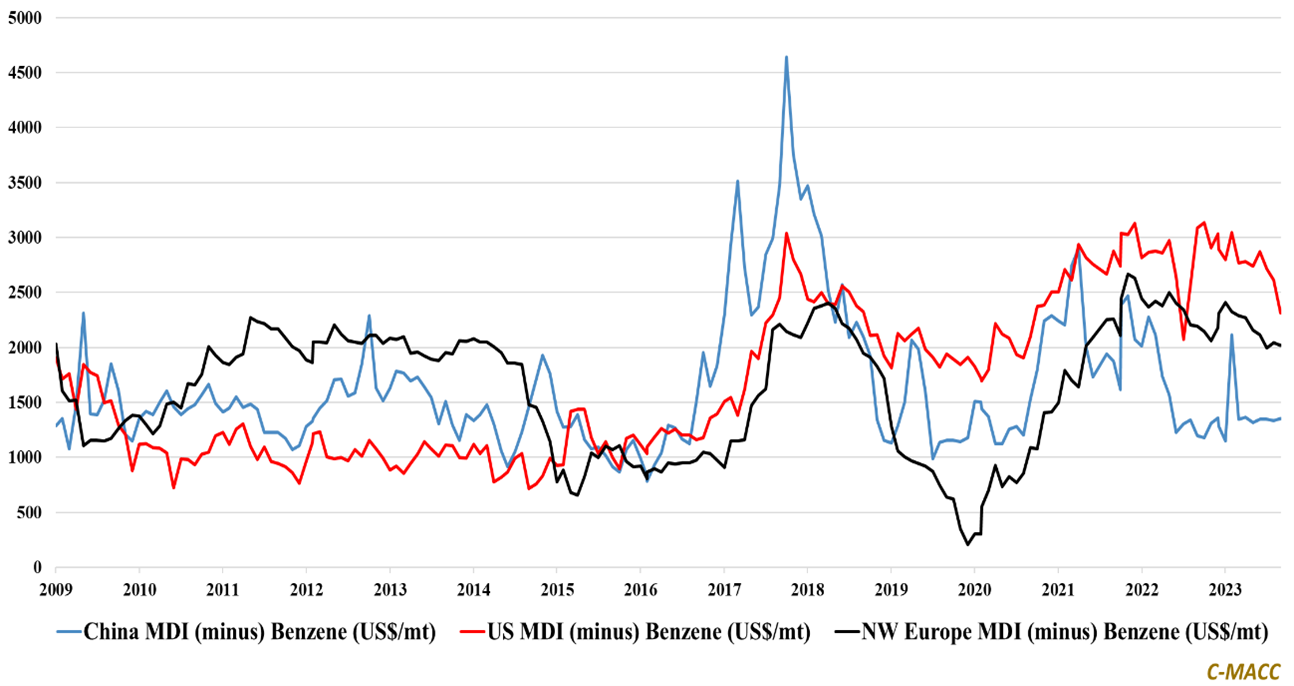

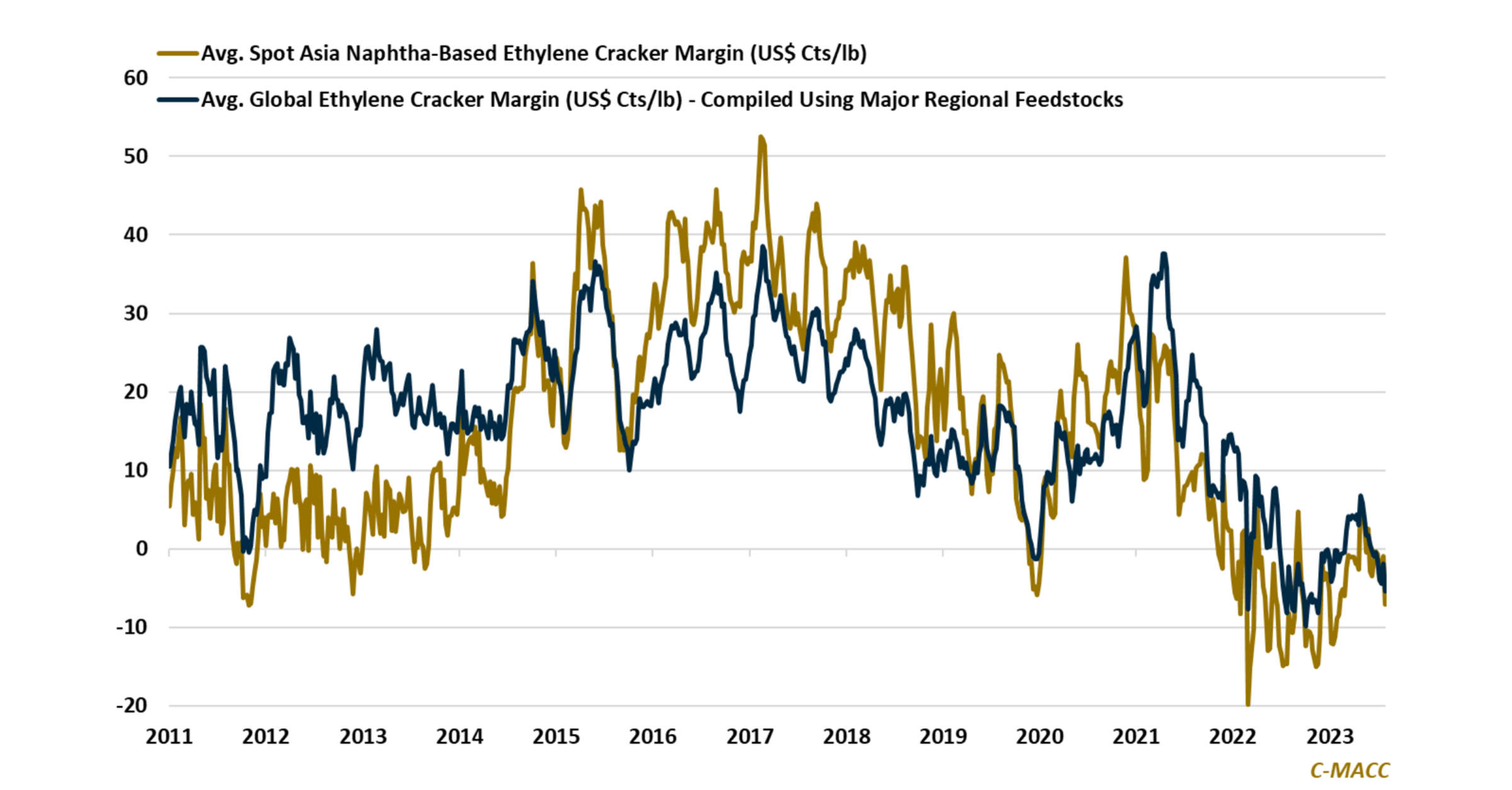

Global feedstock values shifted in favor of a flatter global chemical production cost curve in the first week of 4Q23, putting downward pressure on recent

The sustainability push across the chemical industry is underway, and all agree that higher prices are needed to drive growth – will it come forth?

Global chemical oversupply will likely worsen into year-end as North America’s cost advantage and China’s unrelenting production push will overtake cutbacks that will likely occur

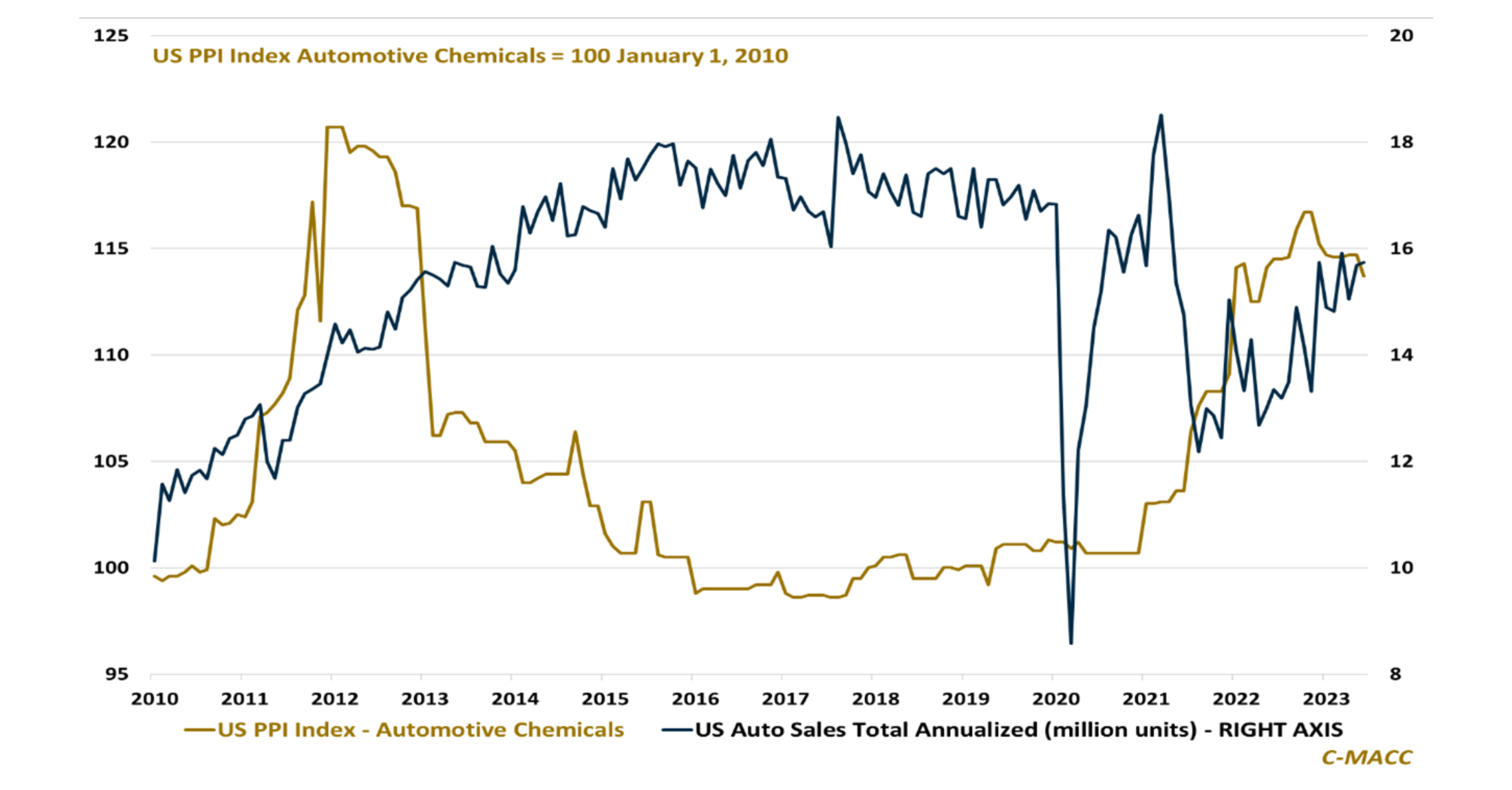

Automotive chemical suppliers have benefited from rising auto production in 2022/23, partly due to inventory rebuilding – we think significant headwinds will face auto chemical

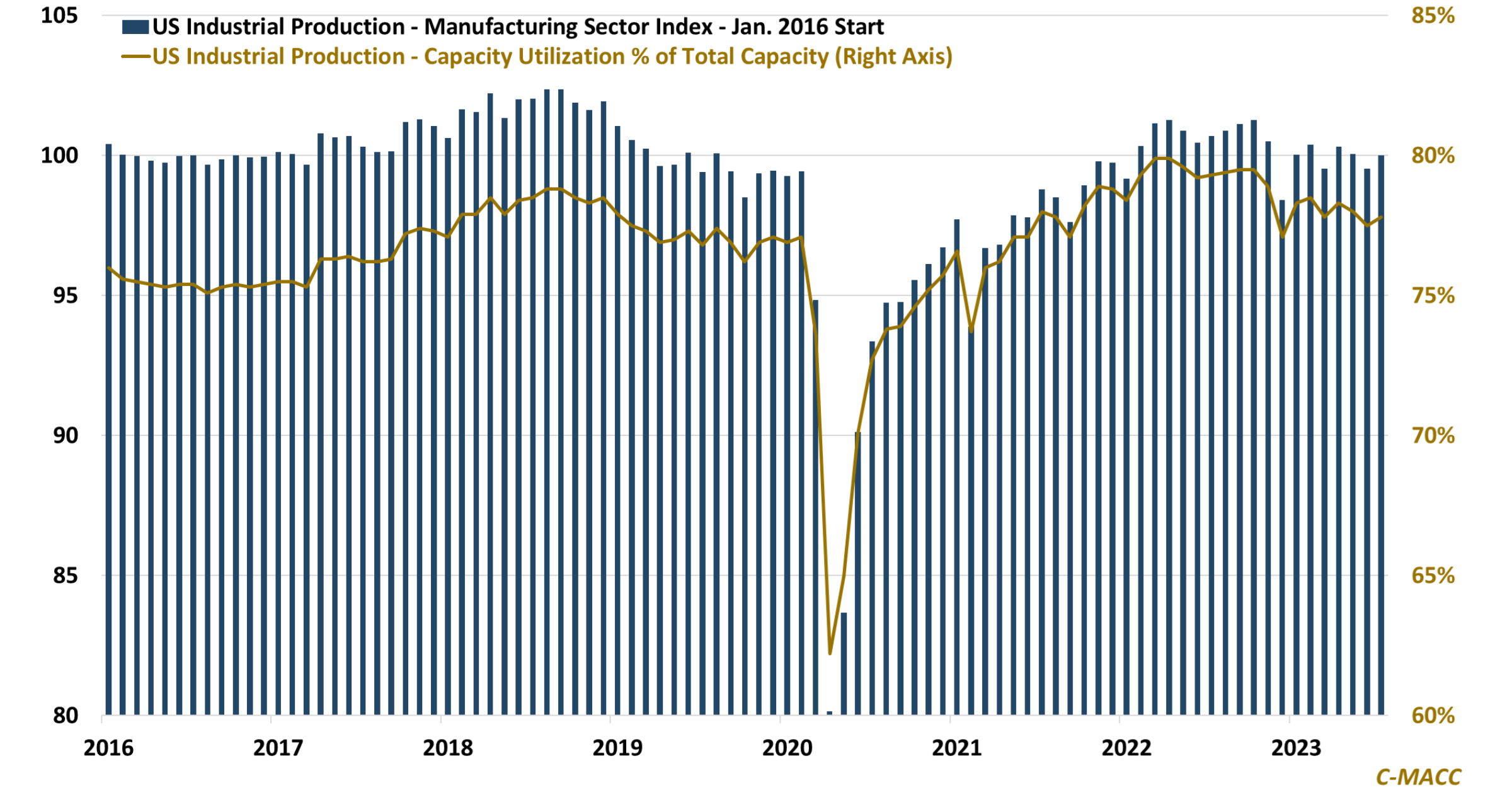

US industrial production remained lower YoY in July due to oversupply overshadowing its energy-advantaged cost position – Europe and Asia run rates are lower for