Ethylene White Paper

European Ethylene – The Elephant in The Room

June 24th, 2024

How to solve the European ethylene cartel claims impasse – a simple quantification approach but one that should drive a consensus and a feasible resolution.

While the current energy, economic, and decarbonization backdrops cry out for restructuring within the European chemical industry, there is a large impediment – a significant unresolved legal matter relating to European ethylene cartel damages claims. These claims matter if you are weighing transaction options, as there are potentially substantial (and some unquantified) assets and liabilities sitting on the balance sheets of the various market players. Companies on both sides of the claims are contemplating potential strategies and are in “need” of a feasible resolution to these claims before they can move forward with other plans.

We, at C-MACC, have decided to weigh in on this matter for several reasons. Over the last four years, we have spoken to several advisers involved in the ethylene cartel claims. As a leading consultancy in the chemical sector, we have clients on both the buyer and supplier sides of the claims who are in the thick of the action. Hence, we have been keenly interested in and closely following the developments of these claims over the past years. I also had hands-on experience assessing unquantified liabilities covering Dow Chemical as a research analyst during the Union Carbide acquisition and the asbestos-related liabilities, which grew over the following years.

In situations like this, while the defendants would like the ethylene cartel claims to go away, everyone needs a feasible resolution. Claimants want to recover their damages in an amicable, expedited, and cost-efficient manner, defendants want a universal “one and done” resolution, and all parties want to save on legal fees, given increasing pressures on internal budgets. We offer our view of where things stand and a possible path to a feasible resolution to these ethylene cartel claims, which is likely what all parties would like to see, fully recognizing that any resolution acceptable to all is one that equally likely leaves everyone a bit unhappy!

Background

The European ethylene cartel damages claims follow on from the European Commission’s (EC) 2020 decision, which found four ethylene buyers guilty and admitting their role in illegally colluding to artificially lower the European ethylene “Monthly Contract Price” (MCP), a widely used pricing benchmark in ethylene and derivatives supply contracts. This cartel conduct occurred over a ~five-year period from December 2011 to March 2017. While the EC levied fines, the extent of the damage to ethylene producers was not quantified in the EC decision.

Ethylene producers harmed by the ethylene cartel conduct have substantial claims for damages. Despite four years since the EC decision, little progress has been made in recovering these damages. To date, we have only seen a couple of concrete moves: Shell’s claim in the Netherlands and a second claim, also pending before the Dutch courts, brought by a claims vehicle on behalf of an anonymous group of corporate entities. Only Shell’s claim quantifies damages at this stage, asserting €1.026bn (not including interest). We think this number is too high, as we explain below. If the ethylene buyers have to resolve the existing and other expected damages claims at these levels, it could completely disrupt the European ethylene market and potentially bankrupt certain major market players. Therefore, achieving a fair and feasible resolution is the only way to maintain a stable, well-functioning European ethylene market, which is crucial to the entire European chemical industry.

Quantification

As we understand it, the quantification approach being taken in the Shell claim is that, as a significant ethylene seller, it was disproportionately impacted by the infringement compared to other producers. We, and other producers, disagree with this assertion, as the ethylene MCP is an integral part of settlements for most ethylene derivatives – affecting everyone in the market much more equally. Such a damages quantification methodology creates a considerable impediment to resolving claims across the whole of the market, because factoring in Shell’s market share in terms of capacity (rather than third-party sales), its claim of €1.026 billion would suggest a ballpark overall sum of around €14 billion in total damages across the entire European ethylene market. The defendants simply cannot afford to lose this legal battle, or they face possible bankruptcy. Hence, their only option will be to fight in the courts for as long as it takes.

Drawing on our extensive market experience, specifically in European ethylene trading while working for a European producer (albeit a while ago), we believe the quantification methodology underlying the Shell claim, which we understand may be underlying other expected claims, contains inherent flaws. Not only does the claimed €1.026bn figure for Shell appear excessive in the context of the defendants’ European business, but it is also excessive relative to the actual harm that might have been suffered. We explain.

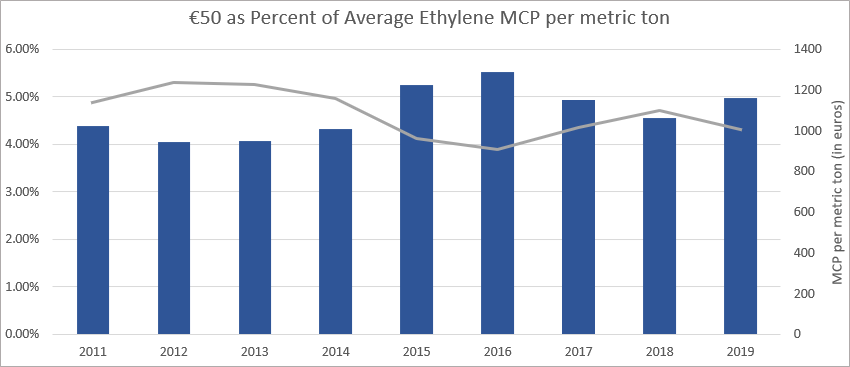

We believe that since most ethylene and derivatives sales during the cartel period were based on contractual formulas tied to the manipulated MCP, all producers across the market were equally impacted by the cartel conduct. Furthermore, the manipulation of the MCP cannot have been as severe as implied by the Shell claim, first and foremost, because the sophisticated parties involved, with their knowledge of the ethylene market, would have spotted extensive pricing inconsistencies, especially over the prolonged cartel infringement period of over five years. In fact, given how the ethylene MCP was set, we would be surprised if the gains for the buyers were more than €50 per metric ton of ethylene on average – which would be equivalent to 4.1-5.5% of the MCP for the period 2011 to 2019 – see chart below.

In each of the years during the cartel infringement, the European ethylene market capacity was roughly 20 million metric tons a year. Applying the reasonable assumption that the gain for the buyers was unlikely to have exceeded €50 per metric ton results in market-wide damages of ~€1bn per year and ~€5bn in total across the whole cartel infringement period. In our view, this is a much more reasonable total damages figure that more realistically reflects how the ethylene market operated, and it could also be a more likely starting point for any discussions to resolve the impasse over these ethylene cartel claims.

A pathway to a feasible resolution

While the immediate reaction to the above analysis may be that it is too simplistic, we note that the goal here is to create a framework and a pathway that leads to a feasible resolution. So, the simpler, the better! A starting point of €5bn in total damages will likely get both sides of the claims to a discussion table. In comparison, €14bn in total damages will keep the existing and potentially new claims stuck in the courts of multiple European jurisdictions and could take 10+ years to resolve. Indeed, the defendants stated in recent public filings that they ‘firmly reject the allegations’ in the ethylene claims and they ‘intend to vigorously defend their rights’.

In addition, once an acceptable damages figure can be agreed upon, any feasible resolution would also require a pragmatic solution as to how the total damages should be split, in terms of contribution from defendants and distribution amongst claimants. We believe the answer to both lies in publicly available capacity data found in the CMA “World Ethylene Analysis”. This is not because capacity is the most accurate figure (production would be more precise), but, again, because it forms a basis for reaching a consensus, and, importantly, would not require the disclosure of confidential and possibly commercially sensitive production data from the ethylene sellers. For defendant contributions, the CMA analysis shows their capacity to consume ethylene each year, by company and asset. Hence, this would be the least contentious way of arriving at a resolution acceptable to all.

It all seems too easy, but an all-party settlement needs to be straightforward with a mechanism and logic that everyone can agree on instead of each company trying to posture for better relative positioning among its peers. Our conversations with various European ethylene industry players have shown that everyone likely wants a solution to the current impasse. Given that the four ethylene buyers are jointly and severally liable for the infringing conduct and harm caused and their choosing to fight the claims collectively, it signals to us that there is room for a settlement. A feasible resolution would allow all parties to move on and pursue new opportunities or ventures without the uncertainty of these ethylene claims.

We propose a common-sense approach, considering the realities of the European ethylene market, which should appeal to all parties and can be independently handled through mediation to provide an amicable, expedited, and cost-efficient resolution.

We are more than happy to discuss possible next steps with anyone involved.

Loading…

Loading…

More About Chemical Market Analysis & Consulting Company (C-MACC) – www.c-macc.com

Disclaimer: ©2024 C-MACC, 939 Queen Annes Road, Houston, TX 77024. All rights reserved. The information contained in this report has been obtained from sources believed to be reliable, and its accuracy and completeness are not guaranteed. No representation or warranty, express or implied, is made regarding the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and other information provided are subject to change without notice. This report is issued without regard to any specific recipient’s specific investment objectives, financial situation, or needs. It is not construed as a solicitation or an offer to buy or sell securities or related financial instruments. Past performance is not necessarily a guide to future results. Sources: Corporate Reports, Bloomberg, Government Publications.