Global Market Analysis

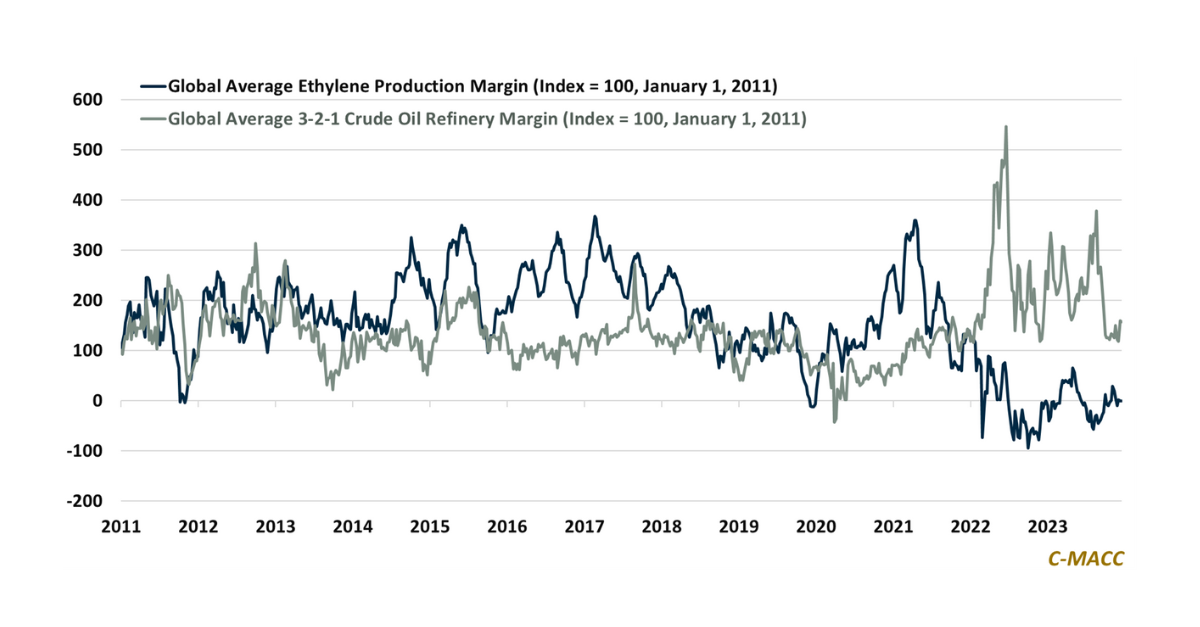

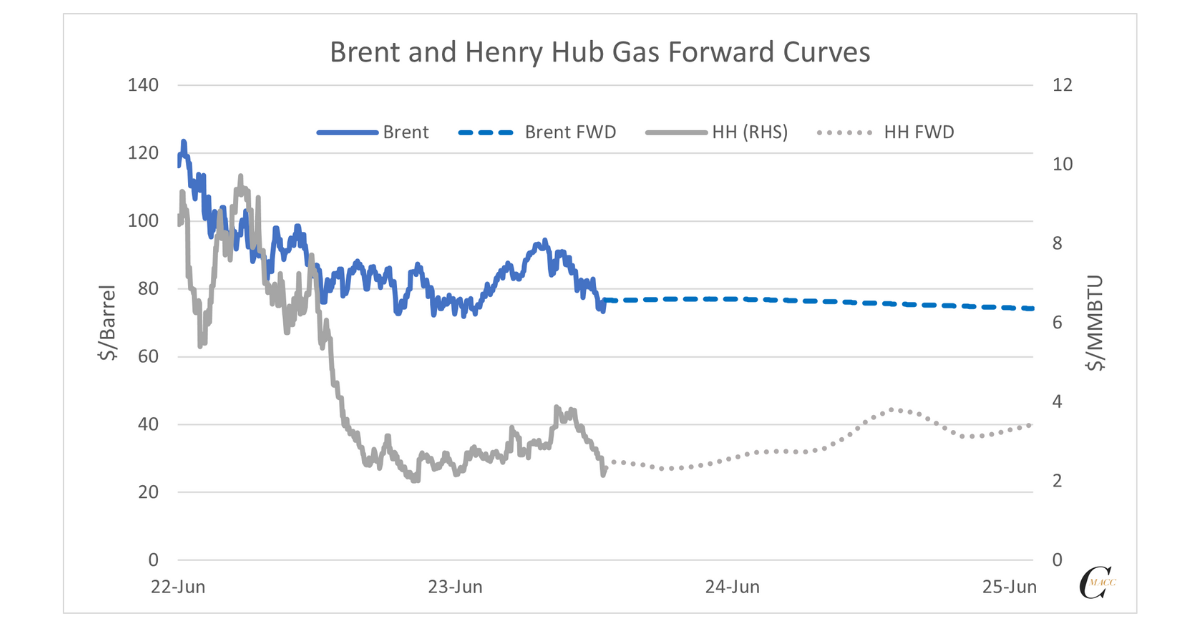

Recent crude oil and Ex-US naphtha price strength suggest downstream refined product and chemical price support that benefits North American producers relative to Europe and

Recent crude oil and Ex-US naphtha price strength suggest downstream refined product and chemical price support that benefits North American producers relative to Europe and

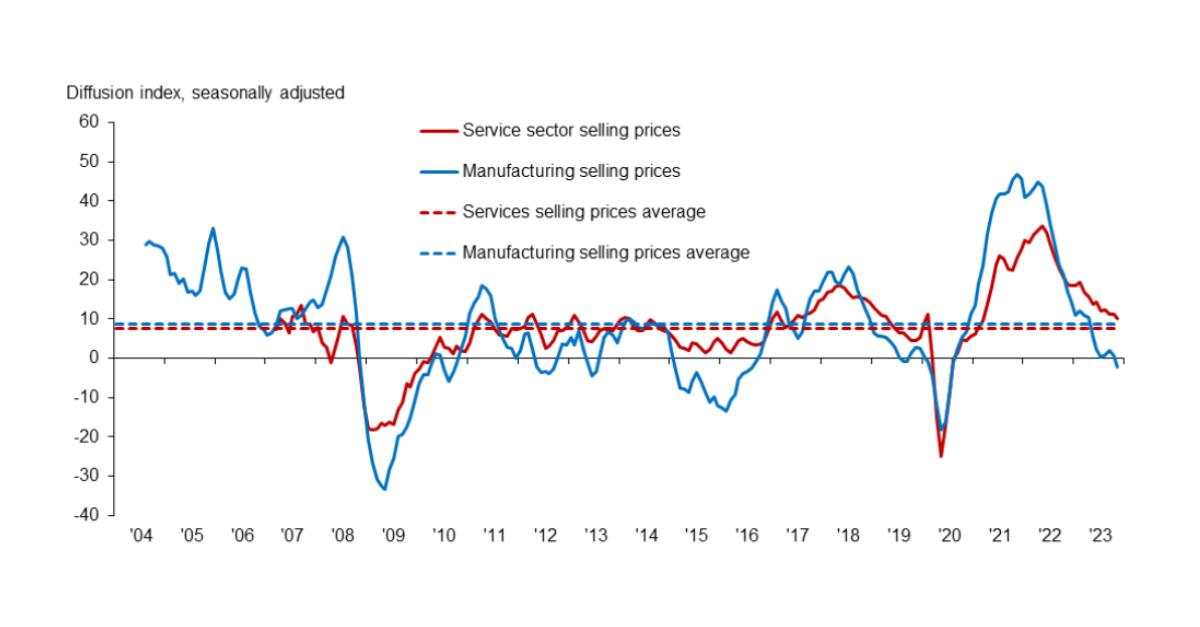

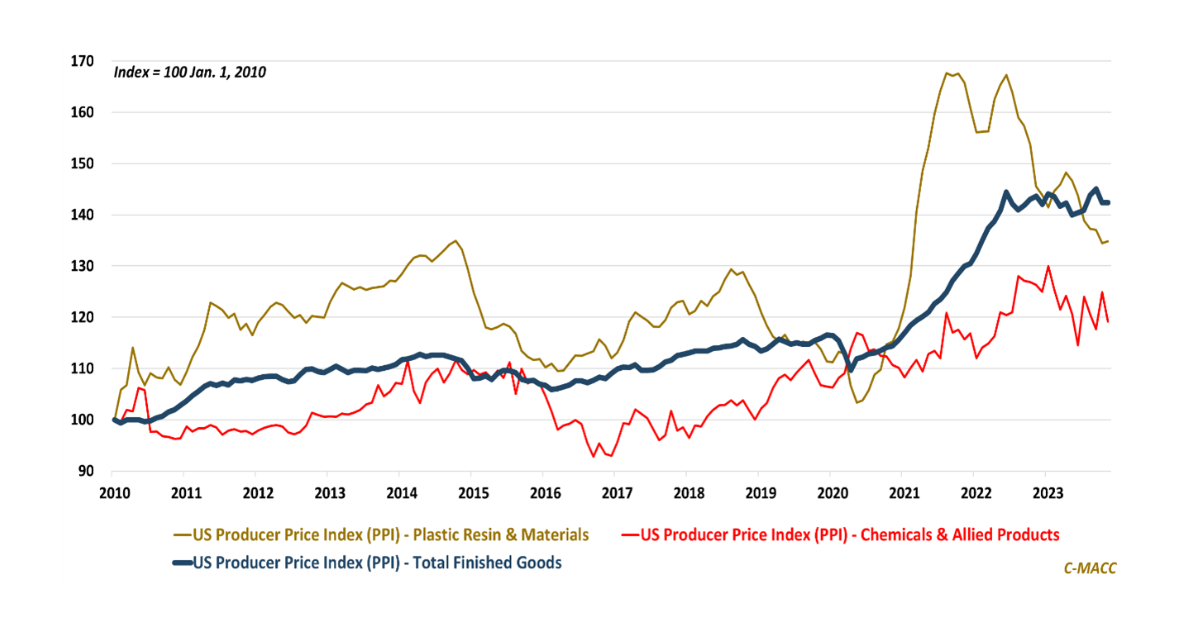

The price of manufactured goods in the US faces downward pressure into year-end amid lower global input costs – crude oil price strength is a

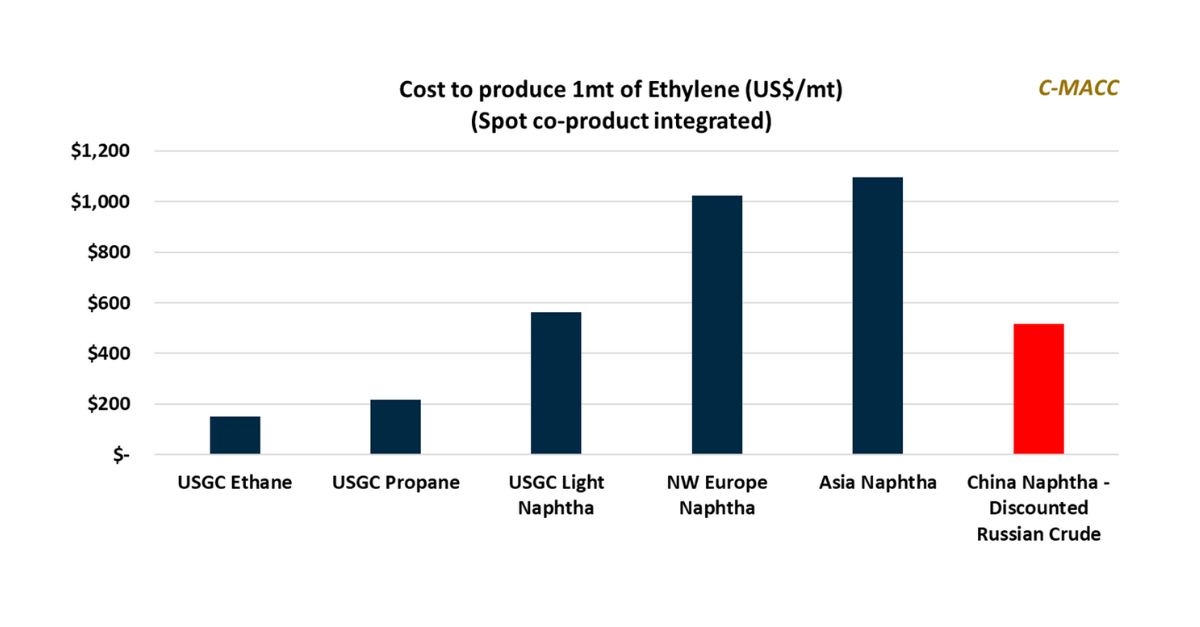

China has imported ~20% more discounted Russian crude oil YTD in 2023 compared to 2022, a benefit to its global petrochemical production cost position and

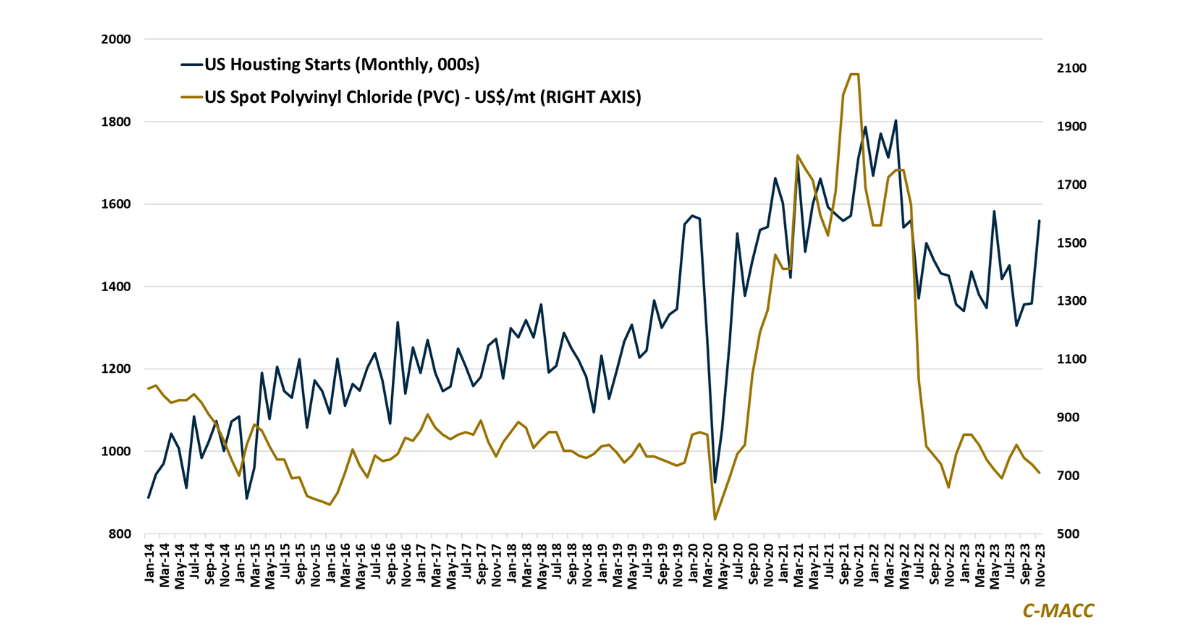

Falling mortgage rates and loosening but still tight domestic home supply are spurring housing market activity that could extend into 2024 and prove constructive for

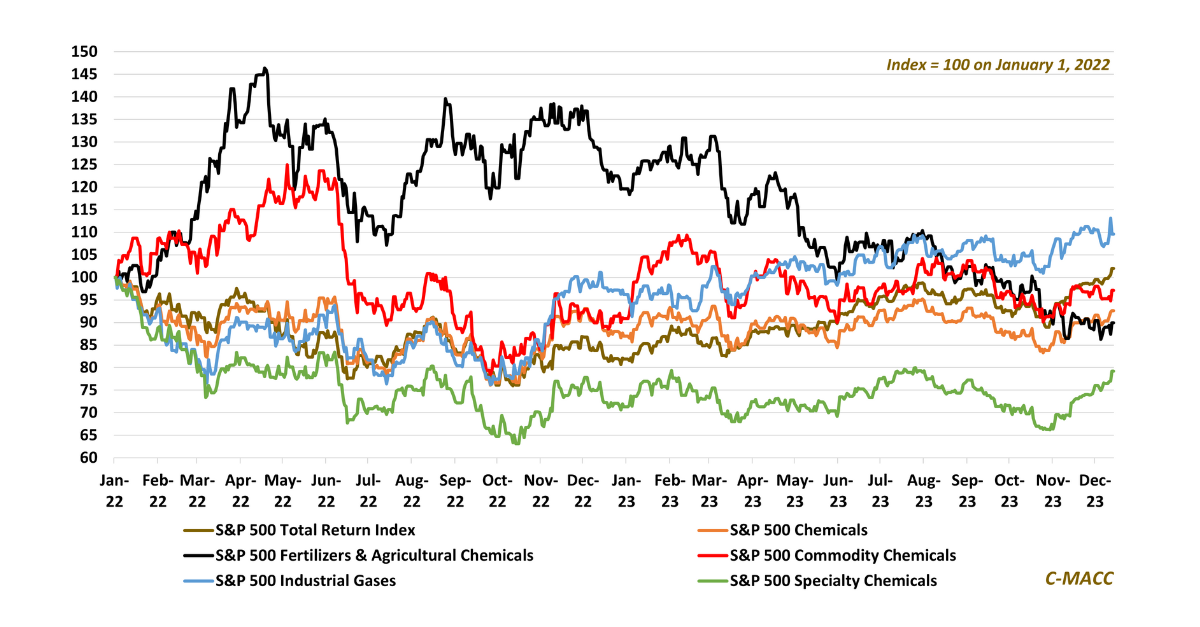

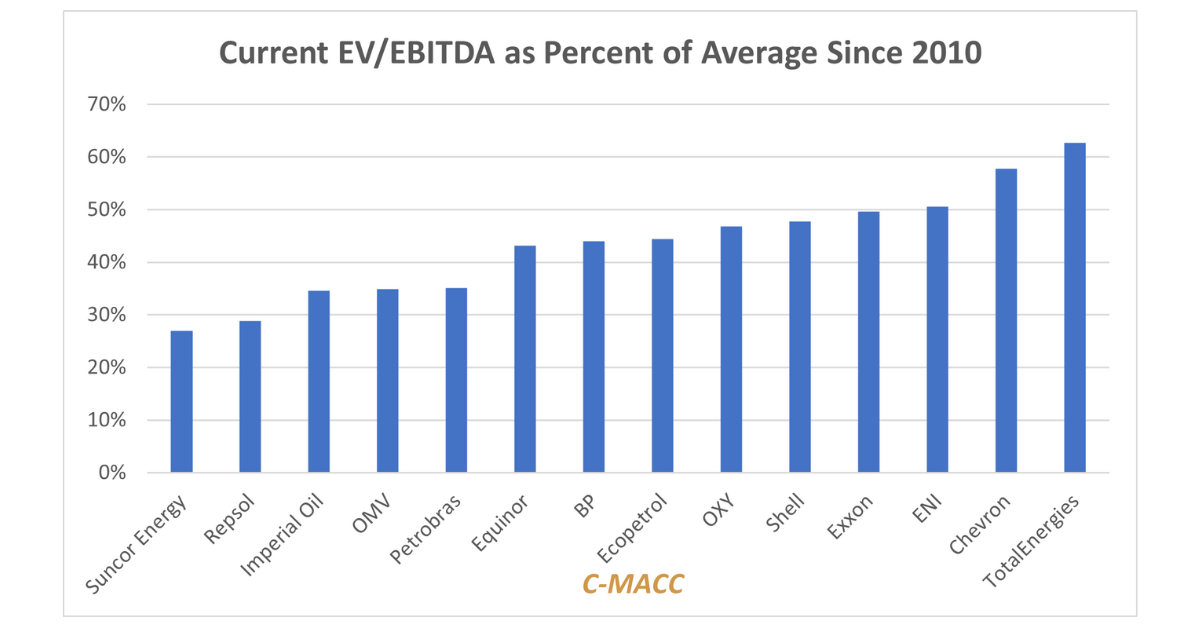

Stock valuations in general suggest a better year for chemicals in 2024, driven by estimates that expect growth over 2023 – oil prices will impact

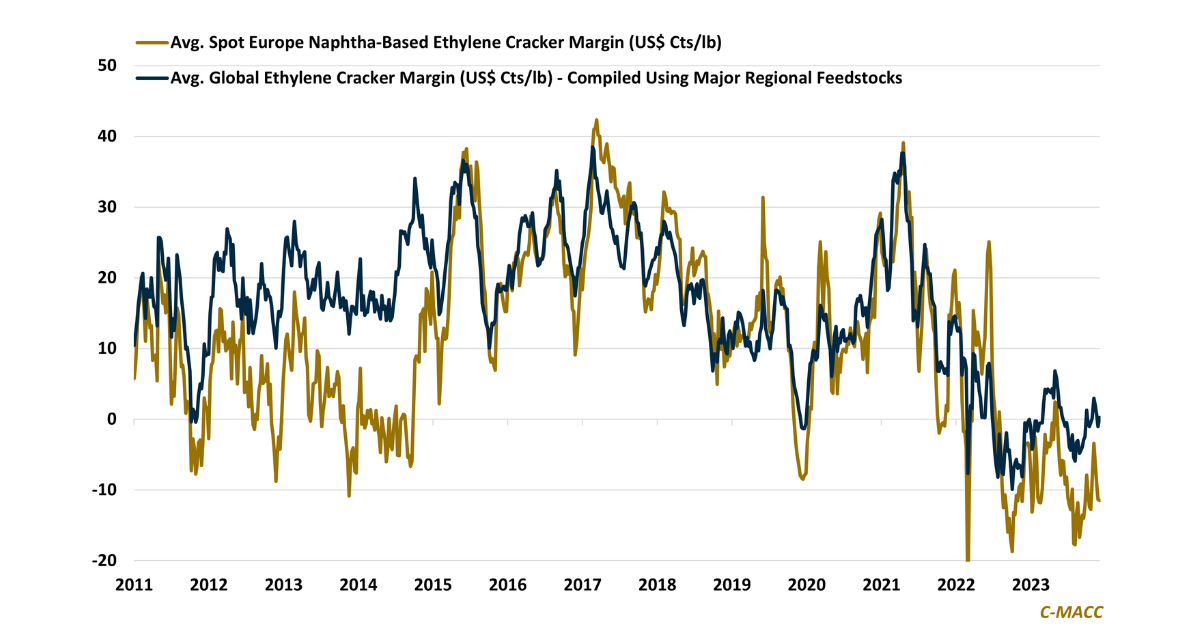

European chemical producers face the challenge of high-cost production positions in globally oversupplied markets, and current trends suggest the region will underperform again in 2024.

Specialty chemical companies have faced myriad demand and cost concerns during the past two years, which has kept equity values in check – cost improvement

US wholesale prices were unchanged MoM in November, while plastic and material prices held up more than chemicals and allied product values – this price

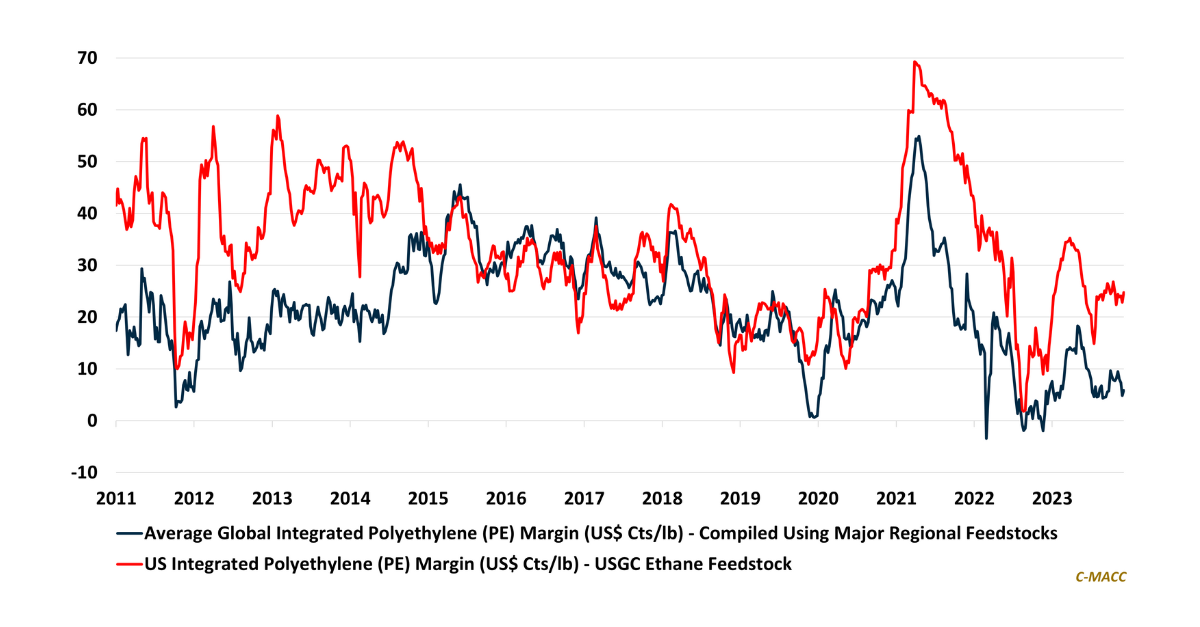

US integrated polyethylene (PE) producer margins reflect strength relative to the global avg. producer margin in 4Q23 – US PE prices have fallen, but its

Many companies will evaluate transaction options over the next few years, but valuation mismatches and unclear regulations could produce significant hurdles.

US oil and gas