C-MACC Sunday Thematic & Weekly Recap 198

Pent-Up M&A: Expect a Surge When the Playing Field Is Understood

- Many companies will evaluate transaction options over the next few years, but valuation mismatches and unclear regulations could produce significant hurdles.

- US oil and gas has, and will have, fewer hurdles than non-US oils and gas and all chemicals and metals, in our view, although we may see asset vs company sales.

- European oil & gas companies appear undervalued on a cash flow basis, but buyers will need deep pockets and willingness to focus on assets outside Europe.

- Chemical margins have risen with falling oil and gas prices, but the downward pressure remains, and the gap with inputs will close – the US advantage is wider.

- Otherwise, we look at ExxonMobil’s ambitious conventional and low carbon plans, the BASF restructuring, blue hydrogen, and failing ESG investing.

Last week we discussed 23 Chemicals and Related Products and 124 Companies.

Regardless of altruistic objectives that may or may not influence corporate behavior, economics will generally rule the day. This view applies to the decisions around capital budgets – high for the oil and gas industries because margins look good and falling for the chemicals and metals sectors because margins look much less interesting. The same simple economic rules apply in the M&A market, and one of the reasons why activity in the chemical space this year has been so limited is because the economics have not made much sense – buyers and sellers are too far apart on valuation and major economic uncertainty around potential regulatory changes. By contrast, for the US oil and gas industry, there appears to be a lot more agreement on value and the drivers of value – this is encouraging stock-based acquisitions, and the activity could pick up even further in 2024, especially given the gap that is appearing between the returns and growth of those that have real scale and those that do not. Valuation is a mess in the chemical space and international oil and gas, which will constrain large-scale M&A. It is easier to trade properties in these sectors; we see that with another Ineos deal this week. We look at the recent BASF move to run three of its divisions almost at arm’s length and wonder whether this is aimed at getting a higher conglomerate multiple or potentially separating the business completely – or maybe it’s just about carbon accounting.

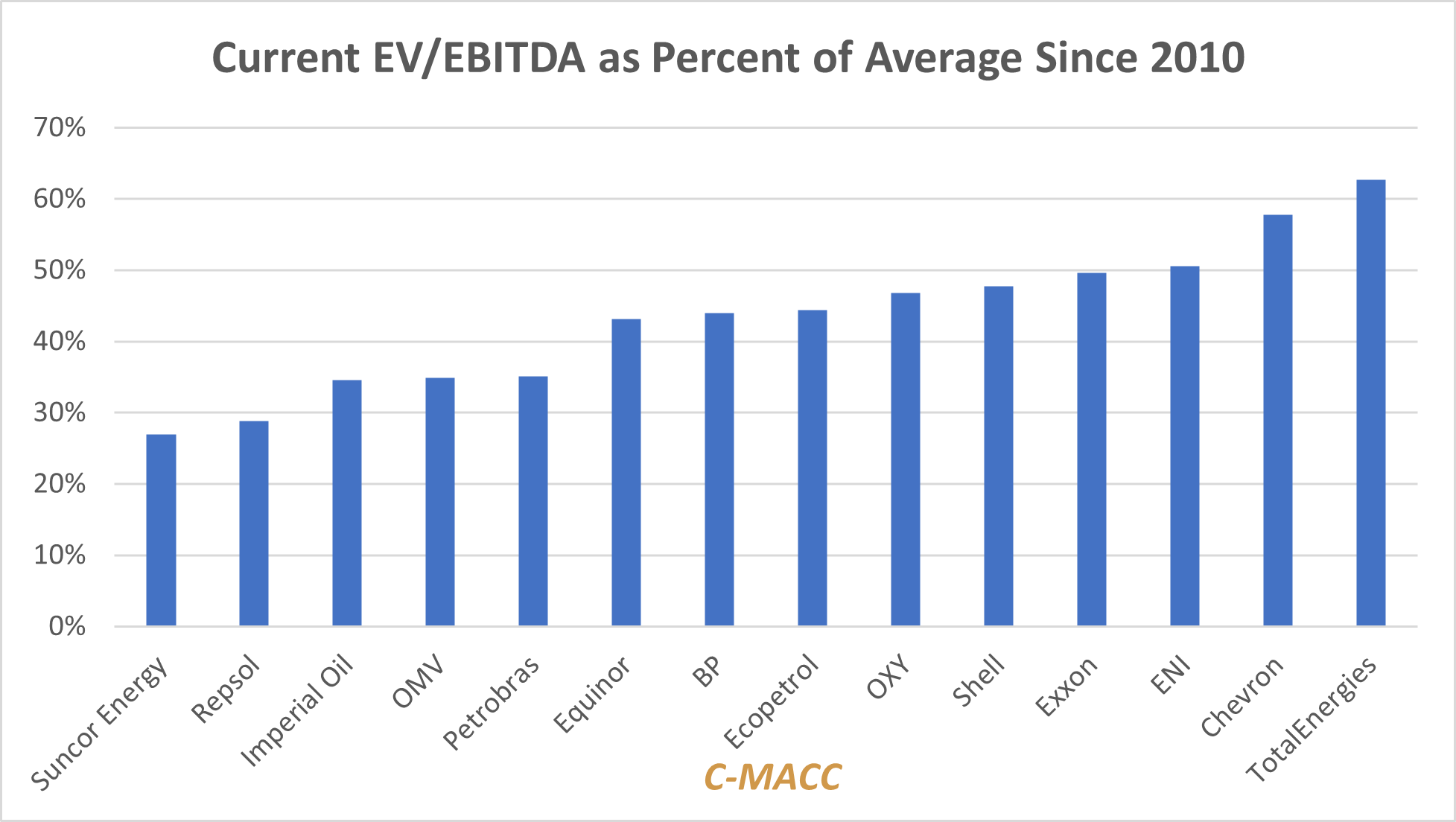

Exhibit 1: All Integrated Oil stocks are now at steep discounts to average values.

Source: Capital IQ, C-MACC Analysis, December 2023

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!