Sunday Executive Summary

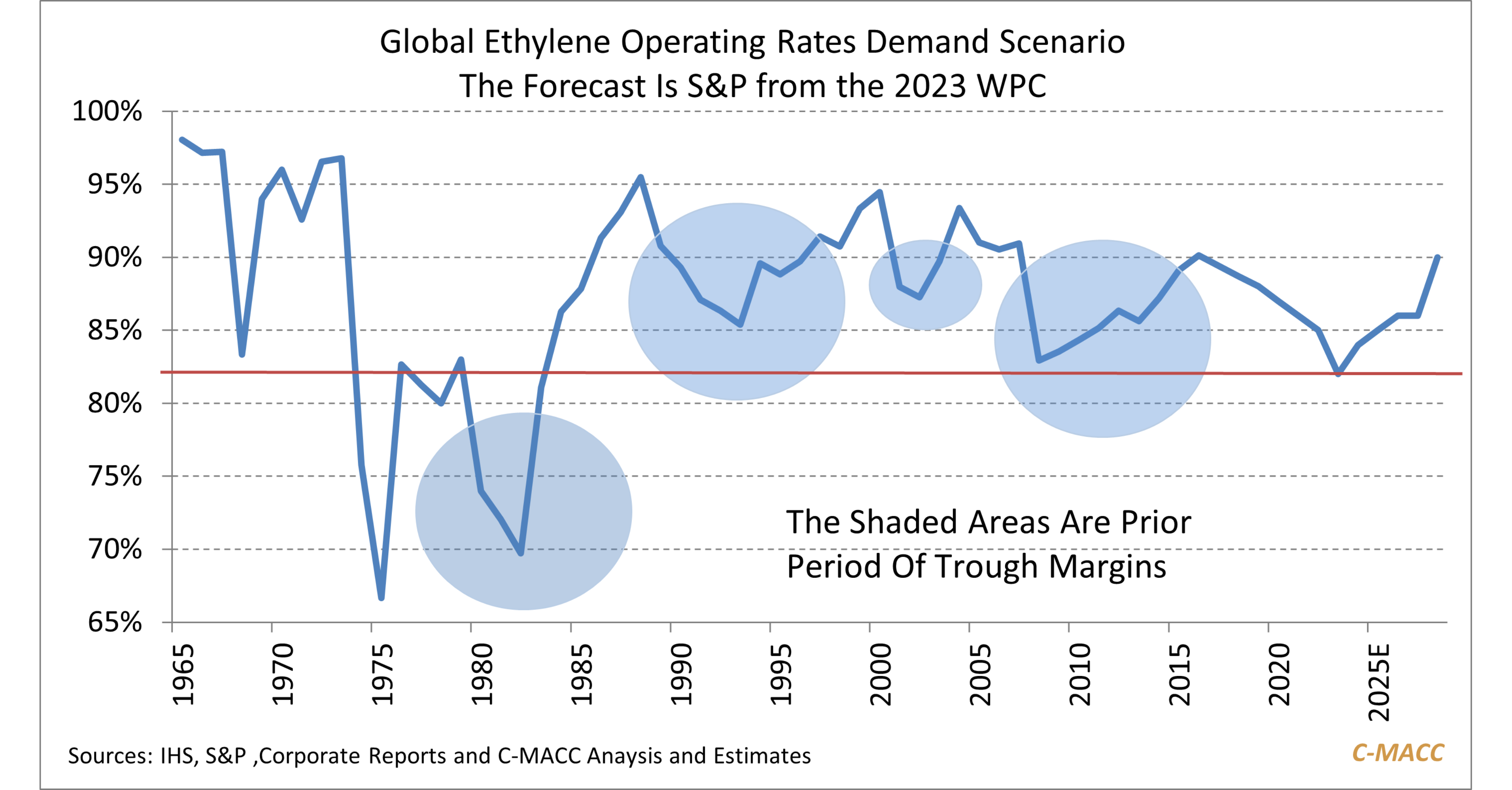

The projection at the WPC this week that polyethylene capacity will only operate at 80% rates in 2023 needs the context that this has not

The projection at the WPC this week that polyethylene capacity will only operate at 80% rates in 2023 needs the context that this has not

Global petrochemical producers outline their market and growth ambitions at WPC. Though all have views, strategies vary, and some bold, risk-adjusted moves lack appreciation in

On average, global polymer prices WoW were unchanged following their 1Q23 run-up. However, global production costs decreased last week, with the US seeing a larger

Both C-MACC co-founders will attend CERAWeek. Our initial view of the agenda suggests a heavy focus on energy transition, but other relevant themes are present.

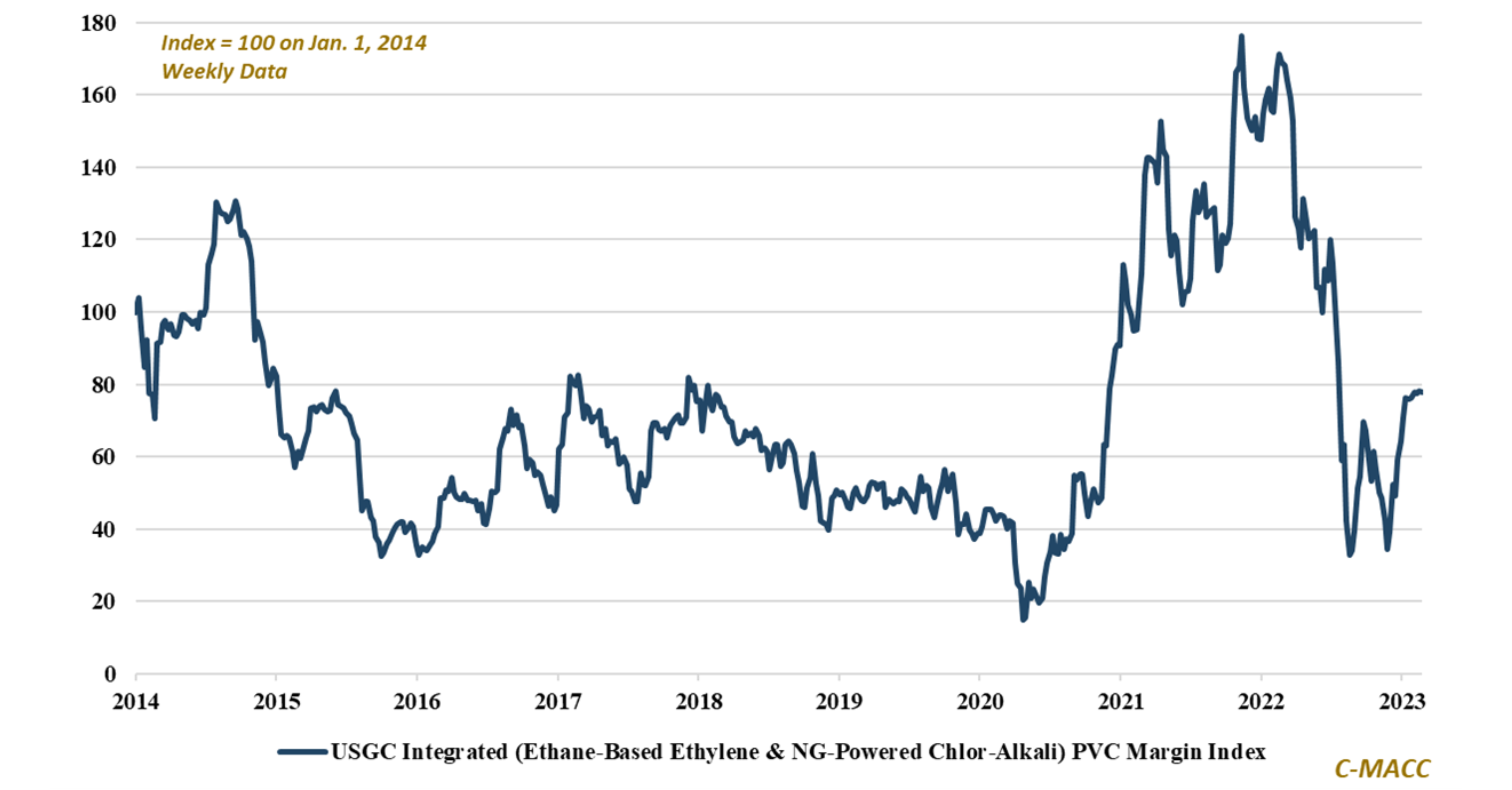

US Chlor-Vinyl margins have increased from 4Q22 lows in 1Q23, and we discuss Oxy views of this product chain in 2023 – we share a

Our theme around the possible need for backward integration for all basic chemical producers as energy transition evolves was validated by INEOS this week.

INEOS

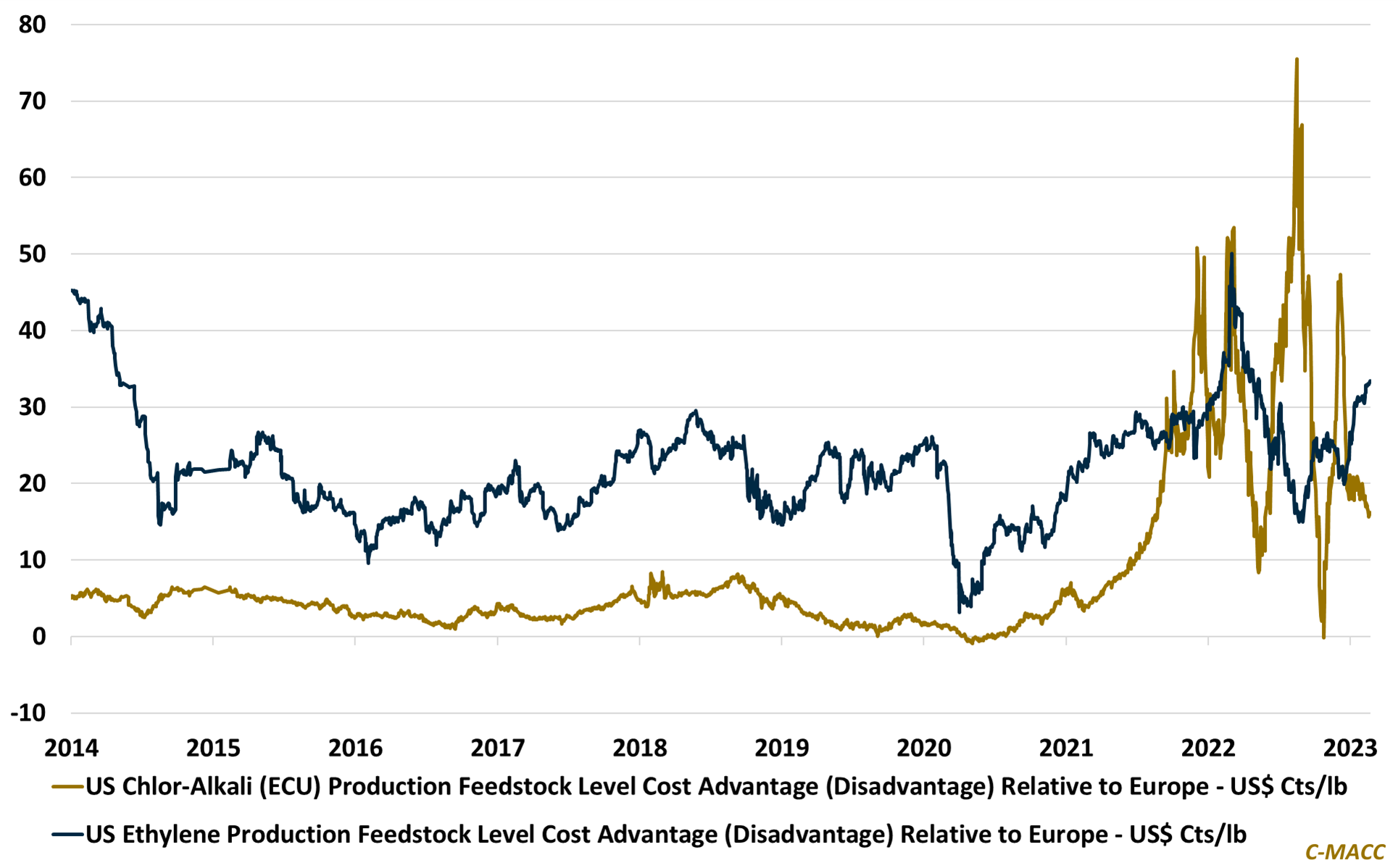

We highlight US cost advantages in Chlor-alkali and ethylene relative to Europe (and Asia), and why we take a constructive view of domestic vinyl producers,

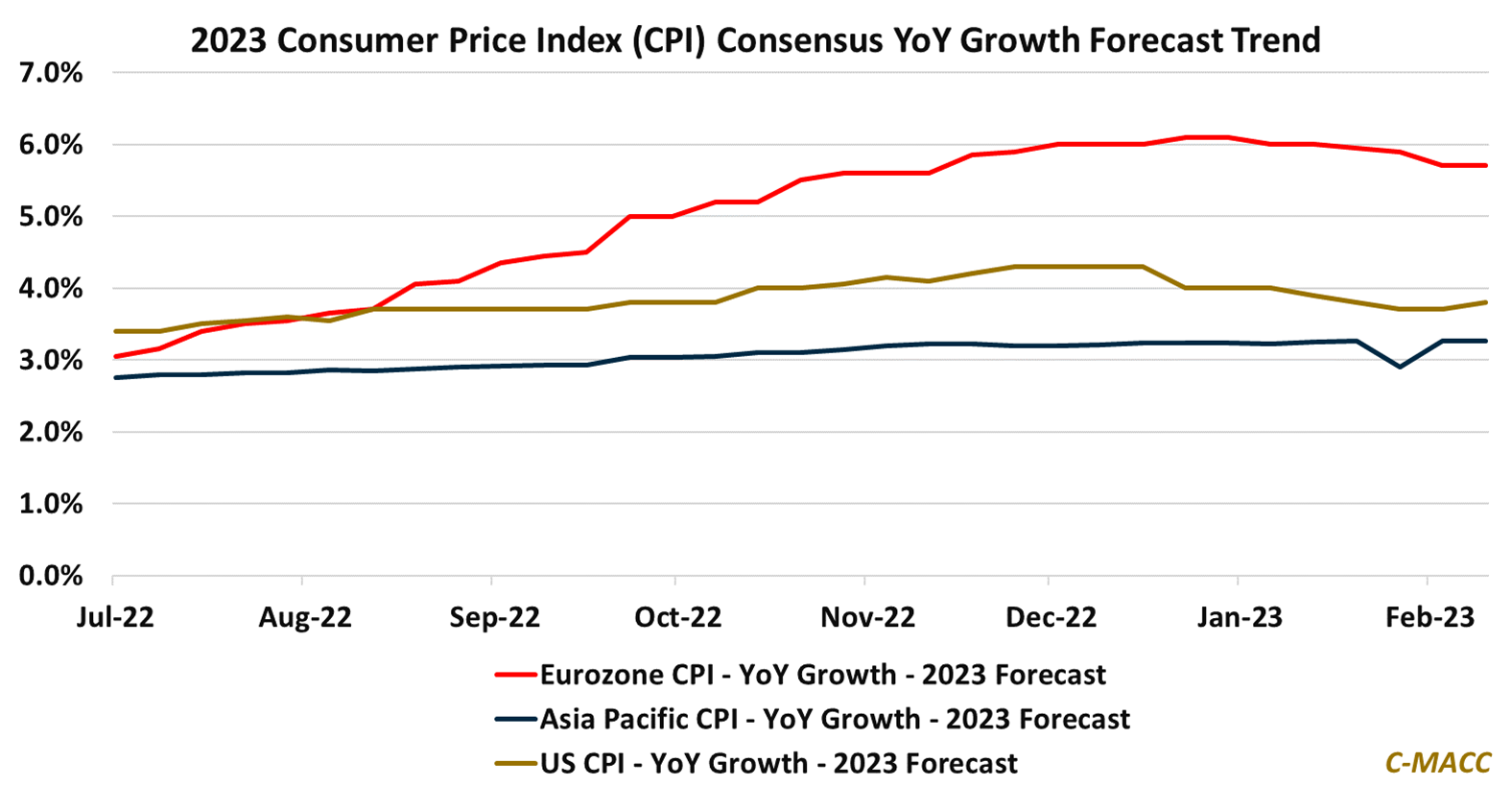

Western consumers will likely face another year of higher prices relative to Asia, but it puts European producers most at risk with its cost disadvantage

Multiple US petrochemical producers highlight that margins have bottomed with their 4Q business reports, but a sector supply response could reverse recent improvements.

We discuss

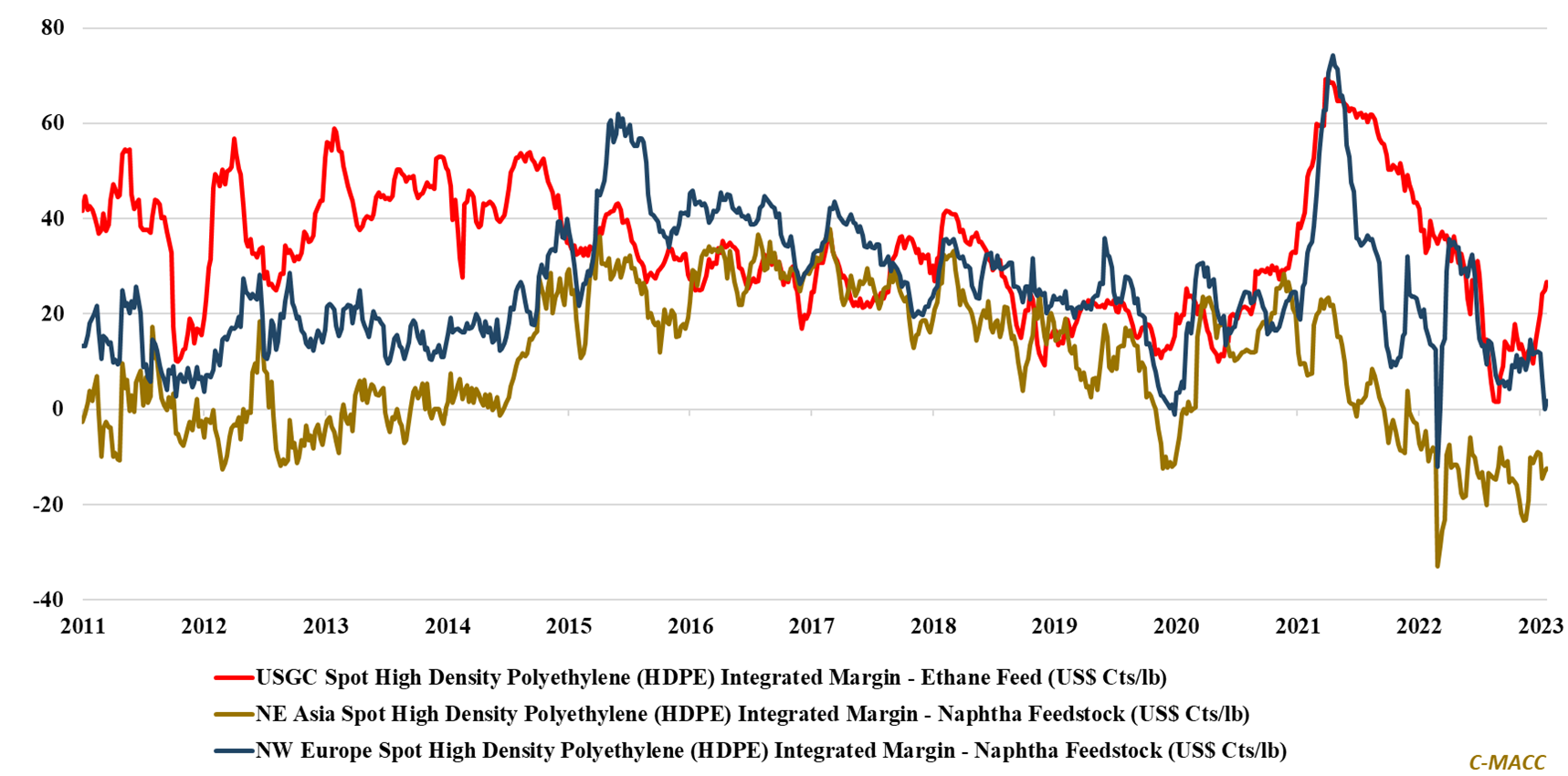

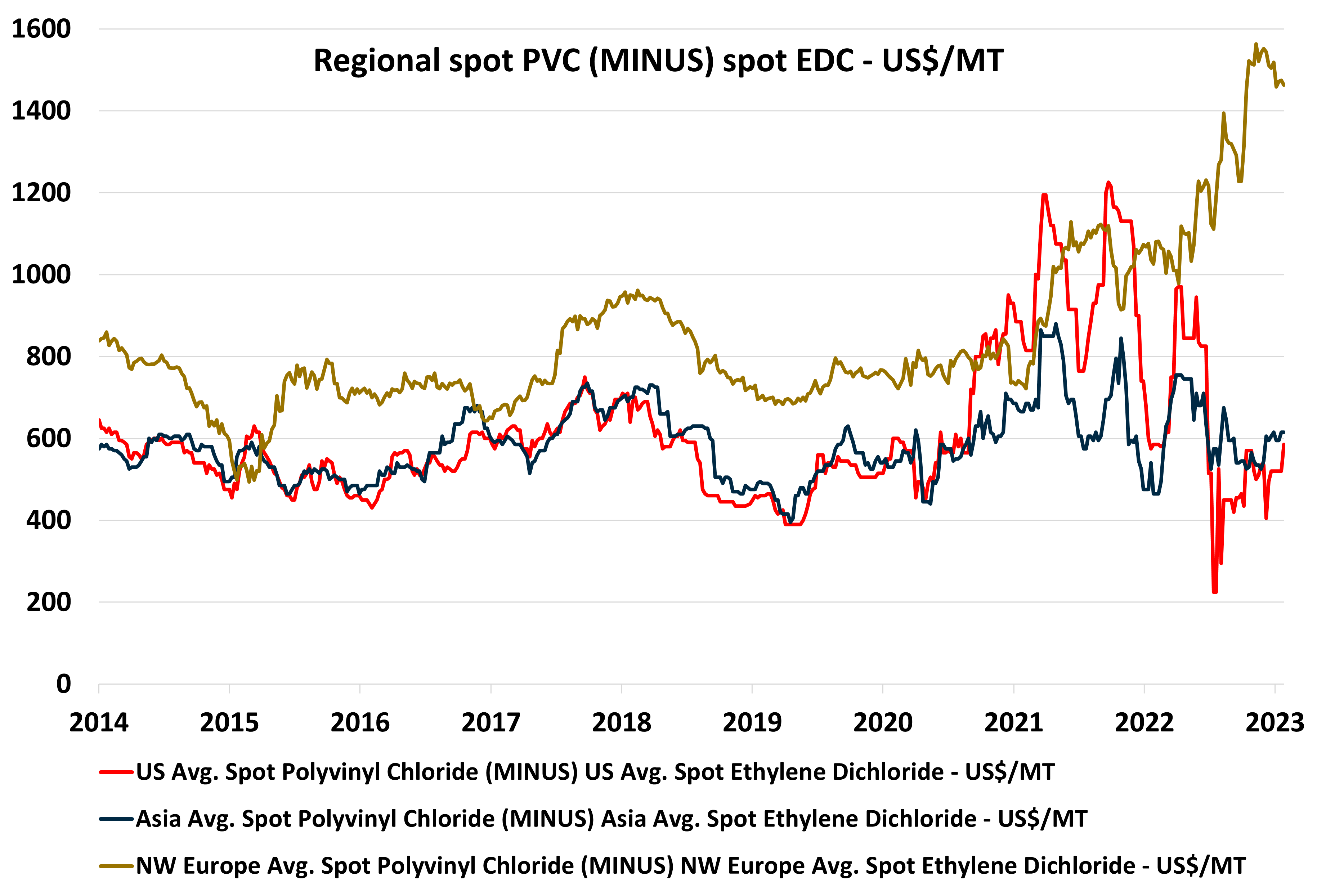

Spot intermediate chemical raw material spreads/implied margins do not always give clear regional profit pictures. Elevated European PVC-to-EDC spreads help show its issues relative to