Daily Chemical Reaction

Holding Back The Tide – Production Cuts Will Sink Inventories But May Drown Some Cost Relief Views

Key Points:

- Initial chemical sector 4Q reports and outlooks support consensus views of commodity weakness and non-integrated derivative producer benefits. Risks vary by region.

- US natural gas and ethane prices have trended considerably lower relative to Brent Crude and Ex-US naphtha relative to 2H22 highs, and we discuss early 2023 trends.

- North America (and US) chemical rail traffic trended lower in late 2022 and early 2023, supporting the case that chemical producers curbed run rates to normalize inventory.

- We highlight lofty estimates for renewables to increasingly displace natural gas and coal power generation and mounting efforts to drive circular product developments.

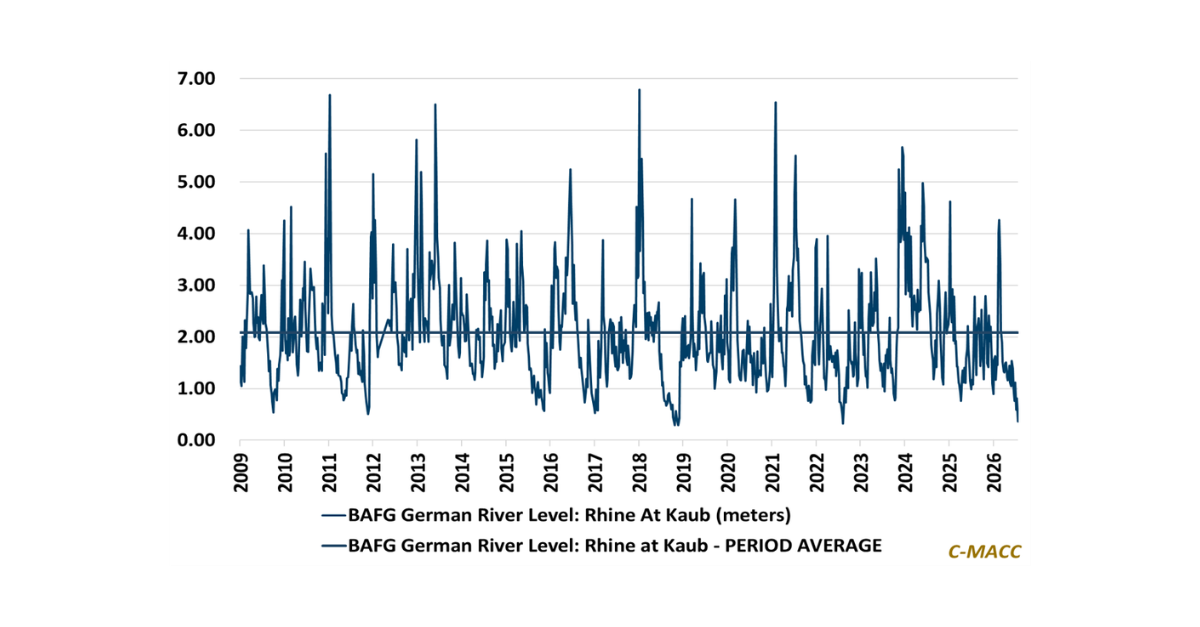

- We discuss the high hopes of a Chinese demand revival in 2023 and implications for the global chemical sector, and we flag a few relevant European demand trends.

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!