C-MACC Sunday Thematic & Weekly Recap 196

Origin Materials: Making Tough Choices Many Others Are Avoiding

- As the global financial backdrop deteriorates for those needing capital, large and small, cash management has become more critical – it is not a time to run out!

- Further, with the possibility of any Trump administration rolling back some of the IRA programs, the risk of investing in something grant- or incentive-driven rises.

- Among newer sustainability-focused companies, mostly SPACs, Origin Materials screens well, as cash conservation is a focus and products are cost-competitive.

- We see a typical year-end softness in most commodity markets, energy, chemicals & crops, with international natural gas the hold out around winter fears.

- Otherwise, we look at US natural gas production rising to meet LNG demand and discuss the now more complex path for hydrogen, plus ExxonMobil’s ambitions.

Last week, we discussed 17 Chemicals and Related Products and 72 Companies.

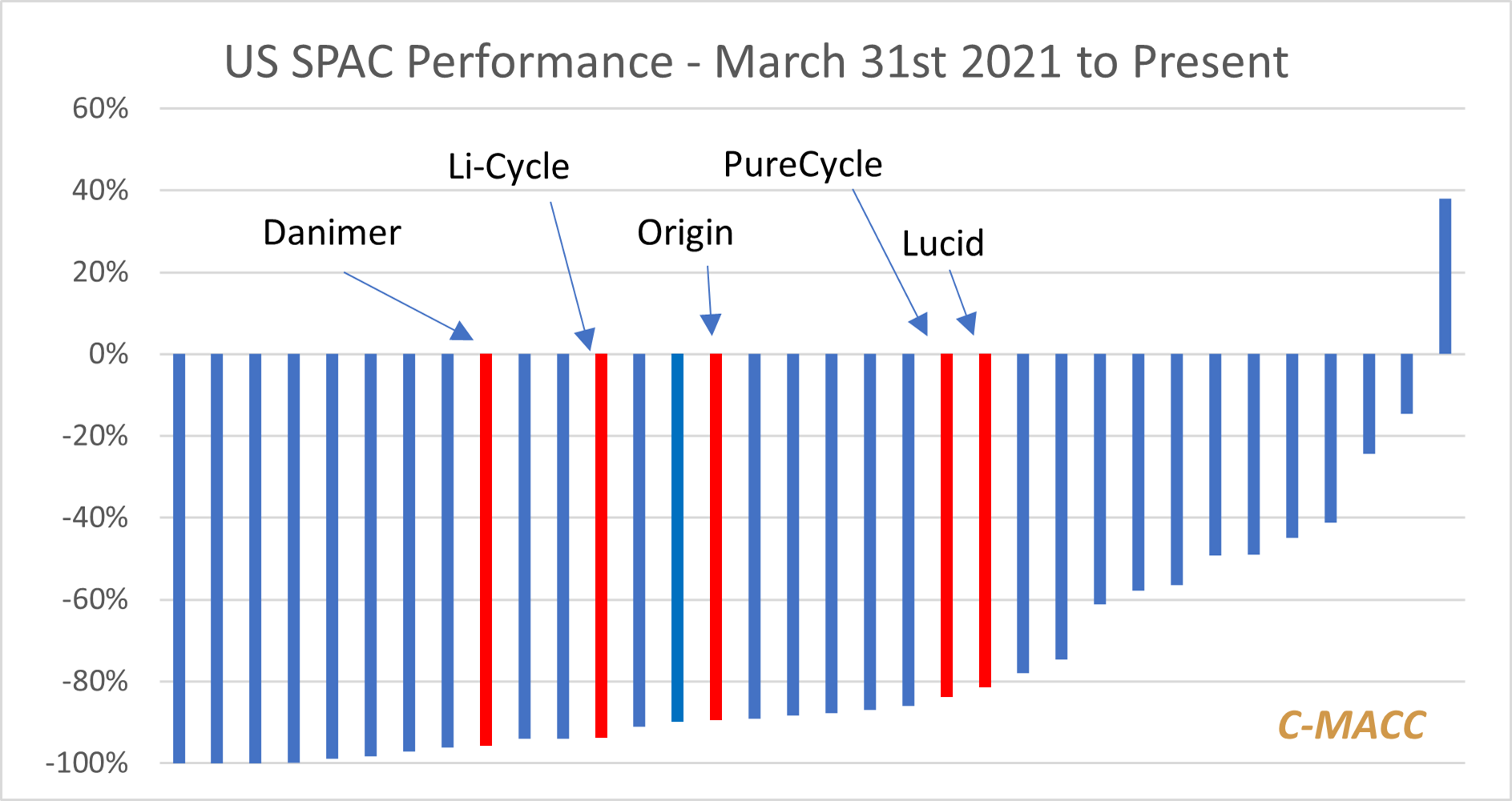

If you have lost more than 80% of your value since your 30-month high, it is safe to say that investors do not feel the same way about your story as they did! For many of the newer companies in the sustainability and energy transition sectors, regardless of whether you launched as a SPAC and appear in our chart below, your outlook is much less sunny than it was a year or so ago. This backdrop is no different from the one that much larger and more established companies feel. Still, a lack of balance sheet strength and diversification exposes any transition strategies from the smaller companies. The oil and gas majors that are pulling back their transition plans are not doing so because the market has lost faith in the pure plays – there is just no money in it. Whether investors’ concerns relate to project cost inflation and interest rate hikes, or current incentive structures that might change, those companies with new technology need to find a path that is not reliant on more borrowing and possibly not dependent upon government handouts – especially in the US. In the analysis/discussion below, it is hard to ignore Origin as the company is making moves to ensure that it can avoid expensive debt or dilution and is competitive without incentives – there are none for renewable materials, and few users will pay more.

Exhibit 1: A selection of SPACs that we follow in our Sustainability work.

Source: Capital IQ, C-MACC Analysis, November 2023

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!