Daily Chemical Reaction

Price Headwinds Challenge Global Clean Product Rollouts & Chemical Production Margins in Europe and Asia Ex-China

Key Points:

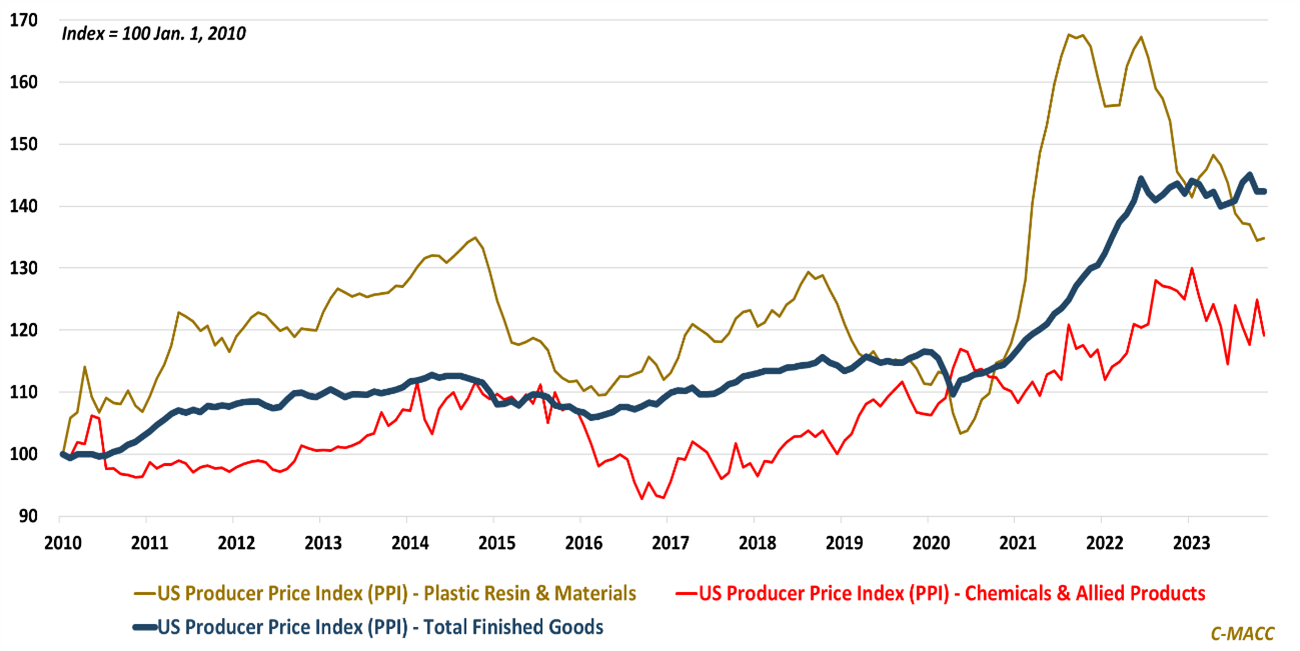

- US wholesale prices were unchanged MoM in November, while plastic and material prices held up more than chemicals and allied product values – this price spread will likely tighten in 2024.

- The price of Singapore naphtha reflects a YTD high relative to Brent Crude, while USGC ethane is near a YTD low relative to US natural gas – a cost curve development favoring North America.

- Recent weakness in chemical feedstocks suggests lower chemical prices into 2024, with new production in China being of notable concern for Europe and Asia Ex-China producer margins.

- We argue that clean power hubs are critical to the economic build-out of green hydrogen, flag the 2023 surge in US cooking oil imports from China, and discuss carbon offsets market growth.

- The ADB estimates China will post the lowest inflation among developing Asia economies in 2024, which we view as a negative for product manufacturers in Asia Ex-China and the West.

Exhibit #1: US wholesale plastic resin & material prices have fallen YTD but reflect relative support to US intermediate chemicals and allied product prices and the overall US PPI index in November.

Source: Bloomberg, C-MACC Analysis, December 2023

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!