C-MACC Weekly Sustainability and Energy Transition Report

Fueling 2024; Why Renewable Fuels May Dominate The Year

- While we see many reasons why some segments of energy transition investment could disappoint in 2024, renewable fuels, especially SAF, is not one of them.

- Demand is almost endless, and European mandates look set to challenge production globally, especially given that construction costs are rising.

- We see fuels as an area with investment growth in 2024, even with some of the political and economic challenges globally – not the case with other segments.

- We look again at critical mineral challenges in the light of recent moves from China – we see no quick fix here – investment needs to start elsewhere today.

- Otherwise, we question the Biden Energy win claims and evaluate accelerating carbon capture in Europe, more failed SPACs, and China’s renewables growth.

First: Renewable Fuels Have The Incentive and Demand Edge in 2024

We have written several recent pieces that suggest slowing transition-related progress in 2024, in part because of permitting challenges and in part because of escalating costs and upside-down project economics. While this may be true for hydrogen, carbon capture, and renewable materials, renewable fuels are likely to be the exception, and we could see an acceleration of investment in 2024. This is because incentives in place today are sufficient to drive investment, and global demand is likely to be insatiable, especially for sustainable aviation fuel (SAF). The risk of a change in incentive policy in the US, post the next election, is still there, but demand in Europe is high, and we are increasingly seeing investment cases in the US based on exports to Europe rather than demand in the US. With lower-cost materials and energy in the US, there is an advantage to making the fuels in the US and exporting, and should we ever get carbon capture permits, this will lead to low-carbon power and other key inputs like hydrogen. But challenges also remain for fuels, with limited easy-to-access inputs, driving more creativity, higher costs, and the need to find clean hydrogen and power to achieve “net-zero” labels. Buyers may have to buy “better” before “perfect”.

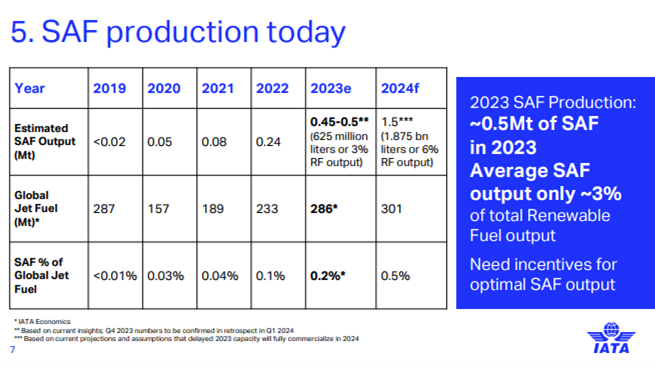

Exhibit 1: This IATA table shows how small SAF production is versus demand.

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!