C-MACC Hydrogen 2023 Summary

Too Fast and Too Furious – It Won’t Happen Just Because You Say It Will!

Key Points

- We characterized 2022 as the year in which the world woke up to the extraordinary need for renewable power – as the enabling step in almost all decarbonizing efforts – this focus is unchanged.

- In 2023, we believe that the market got ahead of itself with hydrogen, not because of anything intrinsically wrong with the idea and need for clean hydrogen but because the power is not there yet.

- The IRS tax guidance has confirmed the main challenge with its additionality power rules and strict low-carbon definitions – if 45V stays in place, qualifying will be challenging and, at scale, is years away.

- 2024 is likely to see less physical green hydrogen investment than most expect, which may create financial challenges for some start-ups, especially in the equipment sector, e.g., Plug Power.

- Blue hydrogen remains far more interesting from a cost perspective. Where CCS opportunities exist in the US, the cost should be lowest, but we need permitting, and capital costs are rising.

Below, we include some of the more interesting things we have written on the subject of hydrogen over the last year – we began our dedicated hydrogen service mid-year. Many of the comments are recent, simply because the landscape has become less cloudy recently. Let’s start with the conclusion – blue is the answer:

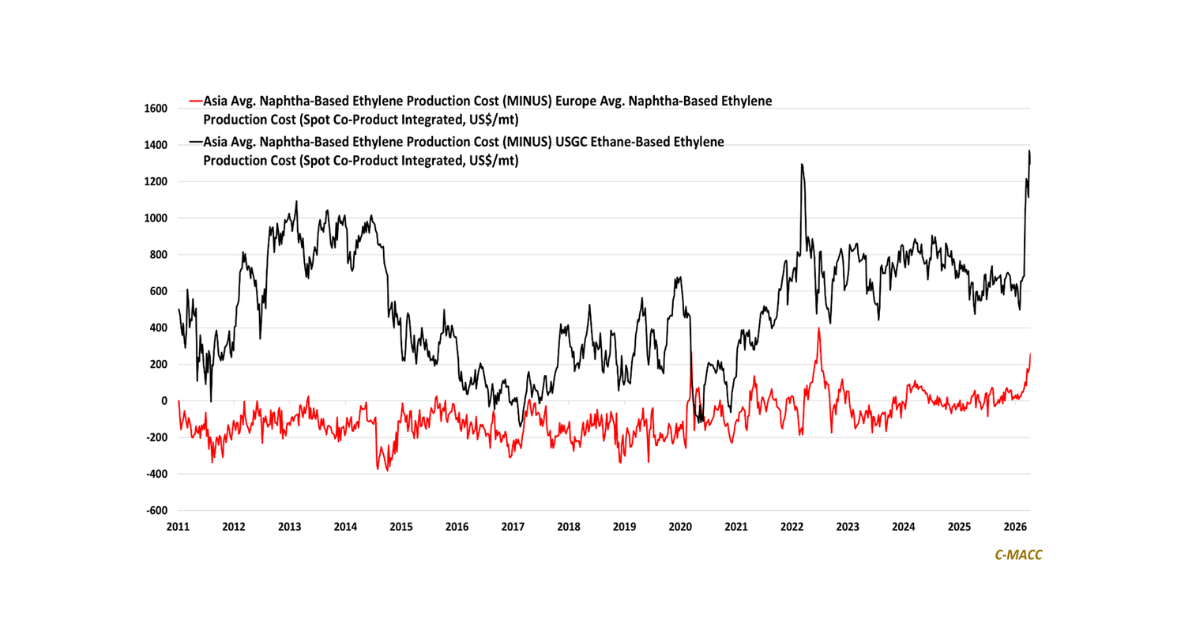

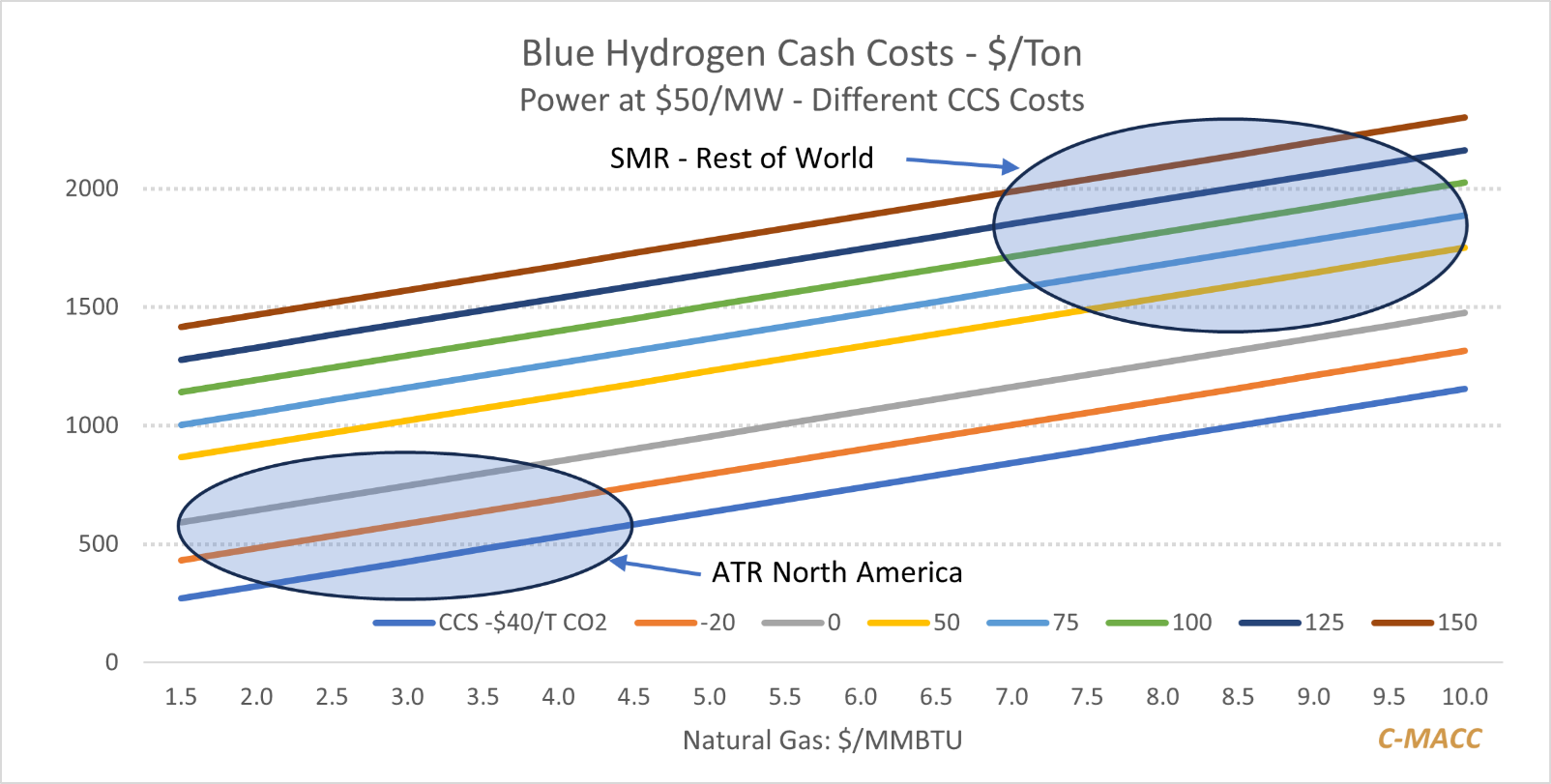

The chart below shows what looks like an insurmountable difference between the economics of making blue hydrogen in North America compared to the rest of the world. This results from two factors – a credit for CCS in the US, and what that credit allows you to do with technology. The 45Q credit in the US is based on the CO2 you sequester rather than the product you make, and consequently, a technology that allows you to capture the CO2 more easily but produces much more of it can be a positive if you can keep capture and sequestration costs down. The lines in the chart below represent different carbon capture costs, from as low as a $40 per ton credit in the US to as high as $150 per ton in some of the higher-cost European locations.

Exhibit 1: While the US advantage looks unassailable, we are comparing blue with blue, not blue with green.

Source: Capital IQ and C-MACC Analysis

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!