Daily Chemical Reaction

Location, Location, & Integration – Cost Position & Relative Integration Keys To Outperformance

Key Findings

- General Thoughts: Cost position and relative integration will likely remain primary determinants of commodity chemical and refining outperformance in 2024 amid oversupplied markets. We discuss Shell’s poor positioning.

- Supply Chain/Commodities: We highlight a few points from our global olefins webcast today, the announced development and operational plans of a few chemical sites to start 2024, and Shell’s 4Q23 business update.

- Energy/Upstream: We discuss US refinery profitability to start 2024, flag recent strength in Brent Crude and US natural gas relative to Asia and European natural gas, and US natural gas strength relative to USGC ethane.

- Sustainability/Energy Transition: We discuss Celanese’s unique position, enabling the start of carbon capture and utilization (CCU) based methanol production, the announced layoffs at NuScale, and other sector news.

- Downstream/Other Chemicals: Our downstream discussion and exhibits mostly target global freight rates, showing a rate surge between China and Europe and the US East Coast, a net plus for US and Europe trade.

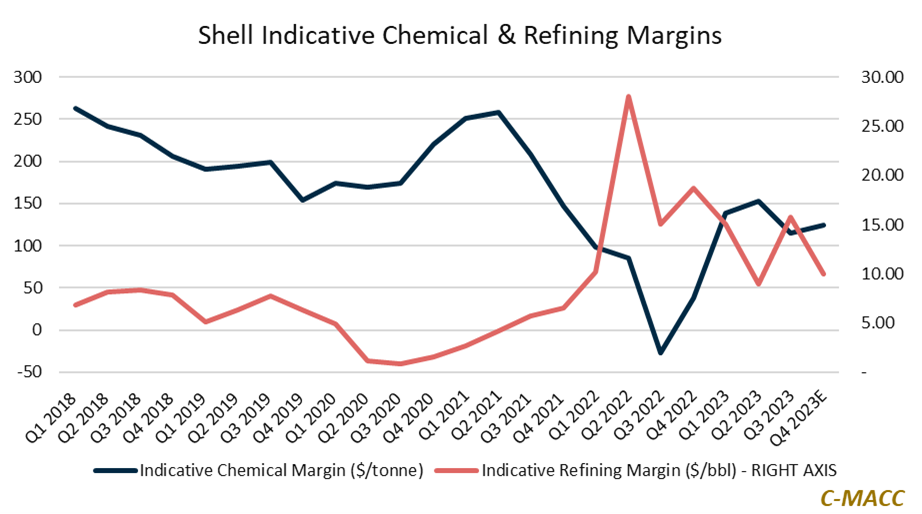

Exhibit 1: Shell estimates indicative chemical margins rose QoQ in 4Q23 while capacity utilization declined (see Ex. 2)

Source: Shell – January 2024 Business Update

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!