Daily Chemical Reaction

How Do You Want It – Chemical Supply Is Not A 2024 Issue Unless You Want It Blue or Green

Key Findings

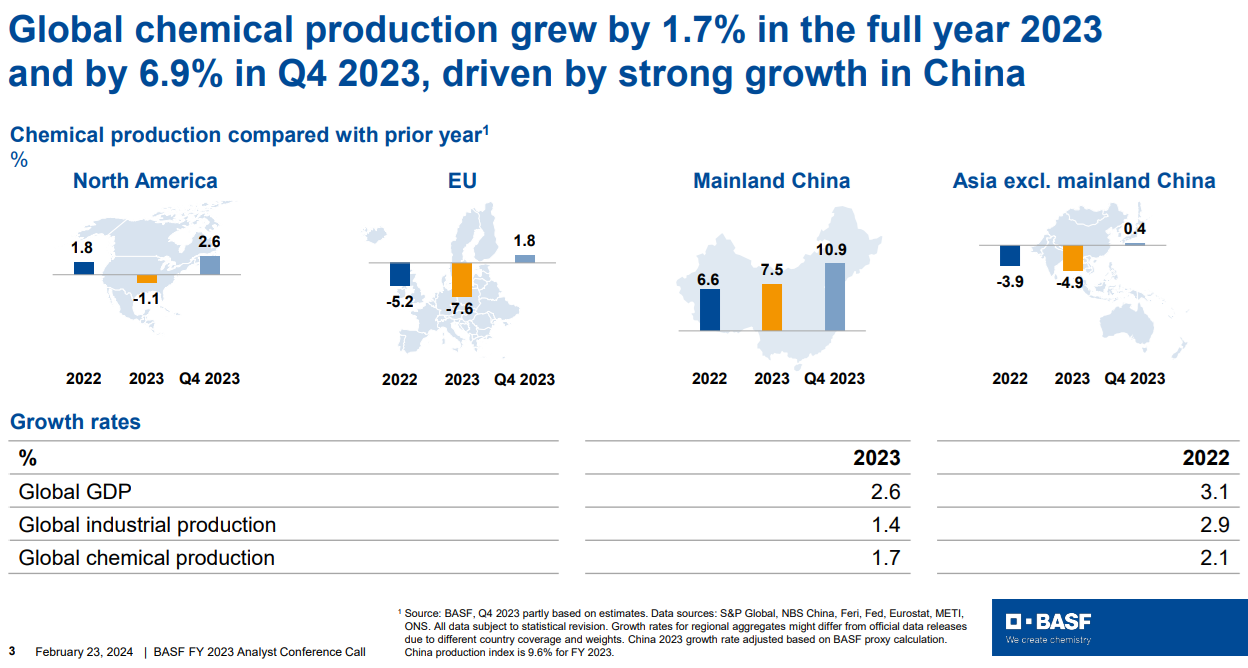

- General Thoughts: Global chemical production significantly grew YoY in 4Q23, and this momentum continued into 2024 in the West and China: this suggests oversupply if demand does not meet early-year 2H24 expectations.

- Supply Chain/Commodities: ADNOC and OMV have a chemicals problem to solve. It may be complex, but the benefit of getting it right is compelling – there may also be some low carbon opportunities from the combination.

- Energy/Upstream: European natural gas prices are lower relative to the weak US, and the European naphtha premium is pulling as much LPG to Europe for ethylene production as can be consumed.

- Sustainability/Energy Transition: We highlight the collapse in Europe carbon prices, nearing 1Q21 levels and ~40% off 2022/23 highs, and comment on global challenges with obtaining enough renewable and low-carbon power.

- Downstream/Other Chemicals: We highlight European manufacturing sector weakness but recent improvement in US manufacturing, though from low levels, and discuss North American rail traffic movements by sector YTD.

Exhibit 1: Asia Ex-China producers are among those being hurt from the recent rise in Western & China output.

Source: BASF – 4Q23 Earnings Presentation, February 2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!