Here is the anecdote, that the global market should not forget:

In the late 80s a client called all excited to tell us that they were going to build a new world scale styrene plant – the market was strong, and margins were good. One of the reasons they gave for the build was that one of the large styrene buyers – a company that no longer exists – had agreed to buy 50% of the output. But the agreement was not at a price that justified the investment, it was at prevailing market prices. At the time, we told the client that the buyer was not really interested in the purchase contract, they were much more interested in what sort of disruptive effect the new capacity would have on overall pricing, which was more important to them. The supply contract cost the buyer nothing as they needed a lot more than what they had agreed to buy from this one facility.

This is happening in a much more magnified way today with lithium, in our view, and companies like Albemarle are falling into the trap. The automakers and battery makers are very conscious of the need for more lithium, and they are encouraging everyone to invest, in part with the goal of ensuring enough supply but equally because they want the oversupply. With consuming industries looking for lower prices over time, anything these companies can do to encourage lithium supply makes sense – that is anything except give the lithium producers guaranteed pricing. We see lithium projects pressing ahead despite the recent collapse in prices and we still see lenders willing to commit capital to the industry.

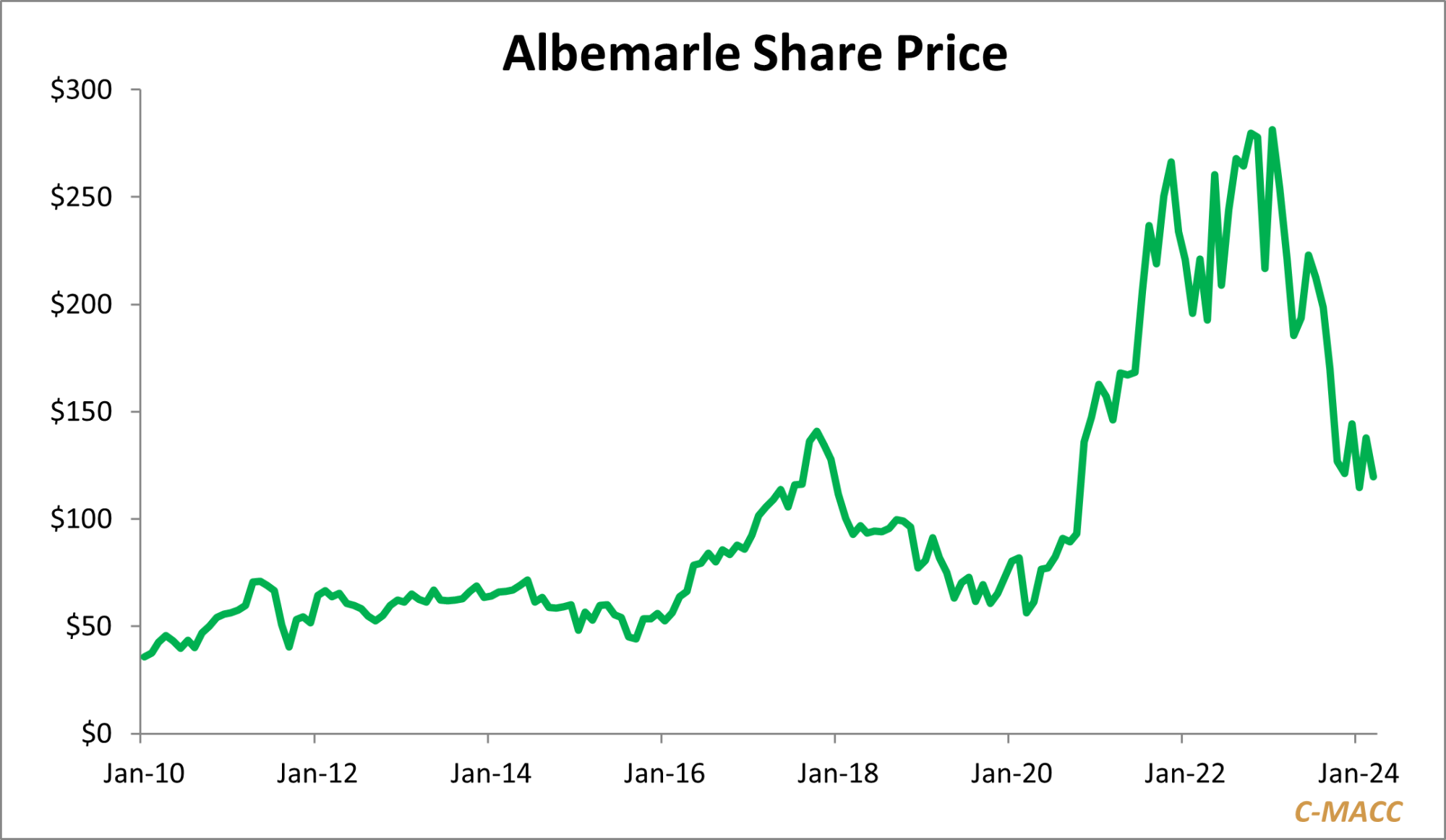

The stock could have further to go if lithium prices do not recover and the company keeps spending.

Source: Capital IQ and C-MACC Analysis, March 2024

Lithium is a special case today as despite similar supply warning signs for copper and nickel, money is not flowing in these directions, as current pricing is a much larger driver of decisions than customer projections of demand. We are also seeing a pullback of investments in other critical minerals and metals because of a decline in pricing – and in the case of critical minerals, this will play into the hands of Chinese producers. With the capital still flowing into lithium and the wave of new entrants, some with possible disruptive technology, there is the added risk that should electrification investments stall in a few years because of nickel or copper shortages, a lithium oversupply could look even more pronounced. With companies like ExxonMobil and Oxy investing in lithium and focused on direct extraction (DLE) from brine, we also see the risk of serious disruption, as these are subsurface and process expert companies, and we would not expect either to be entering the business unless they believe that they can produce very economically – scale economies in DLE could drive much lower costs over time.

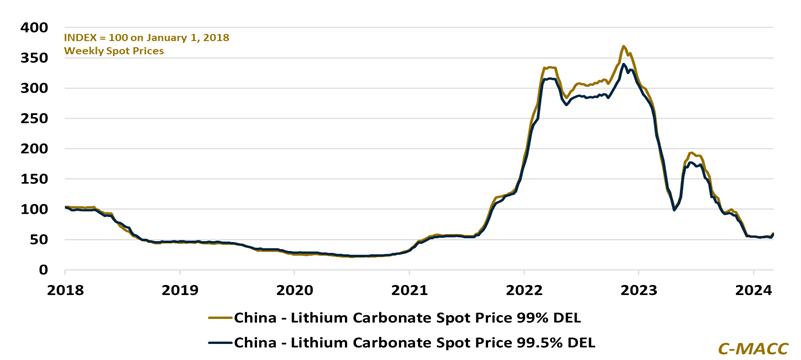

China lithium carbonate prices bounced modestly higher at the start of March 2024, while global lithium prices, at the average, began to rise a bit sooner in February as shown in the Exhibit above.

Source: Bloomberg, C-MACC Analysis, March 2024

Even More Lithium! The Aramco/ADNOC story below is another example of the risks to the lithium space and why we believe that the incumbents should be scaling back investment meaningfully. This is a little different from the ExxonMobil and Oxy DLE initiatives, as the focus is on produced water, which based on our experience in this space can be quite dirty and will require a lot of cleanup, which could be expensive. Still, like ExxonMobil and Oxy, Aramco and ADNOC have deep pockets and can afford to put some capital at risk for this.

Exclusive: Gulf oil giants Saudi Aramco, Adnoc set sights on lithium

Trying to protect market share or minimize lost market share in any commodity market has proven to be a folly for all that have pursued such strategies, and anyone who does not yet believe that lithium is commoditizing should exit the business. This will be a business that, while potentially volatile from time to time with pricing, will see success driven by position on the cost curve, and unless Albemarle has compelling cost opportunities the company should be scaling back its growth plans even further.

Read the complete version of our Sustainability Report below to know more about the implications of the investment decisions of Albemarle and others who might follow suit: