Base Chemical Global Analysis

Global Weekly Catalyst No. 334

- General Thoughts: Chemical value chains should treat late 2Q26 price relief as a positioning window to secure supply routes, liquidity, contract terms, and pass-through before 2H26 tests weaker commercial systems.

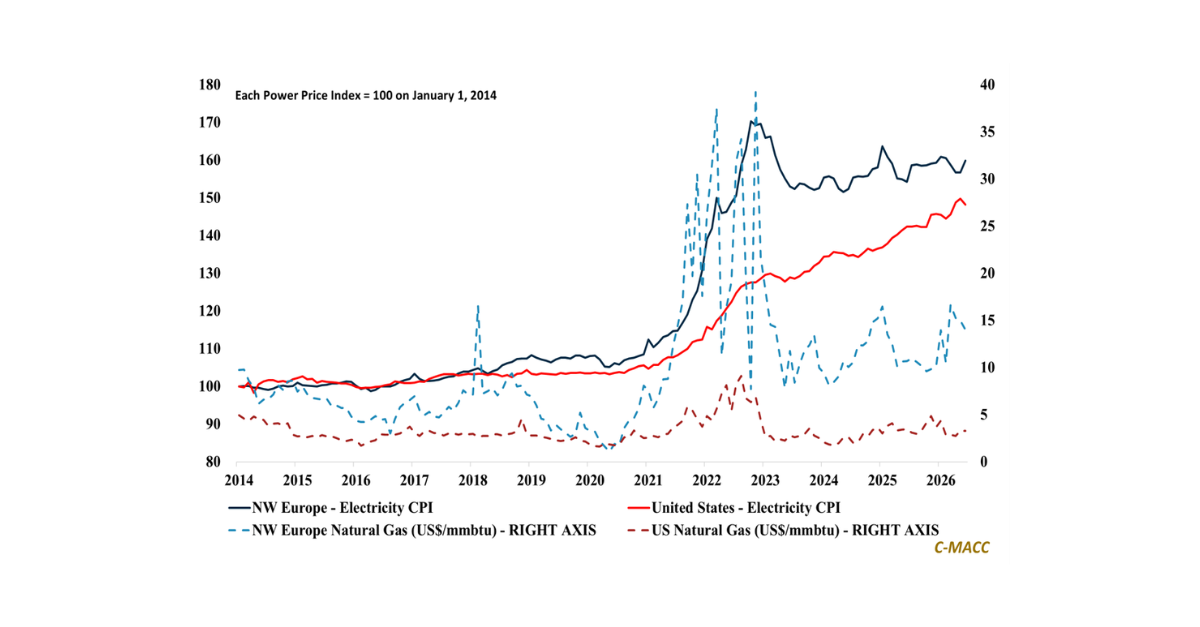

- Feedstocks & Energy: Falling global naphtha and rising USGC ethane values have flattened the global olefins cost curve, making contract control, physical access, and export optionality the sharper near-term feedstock advantage.

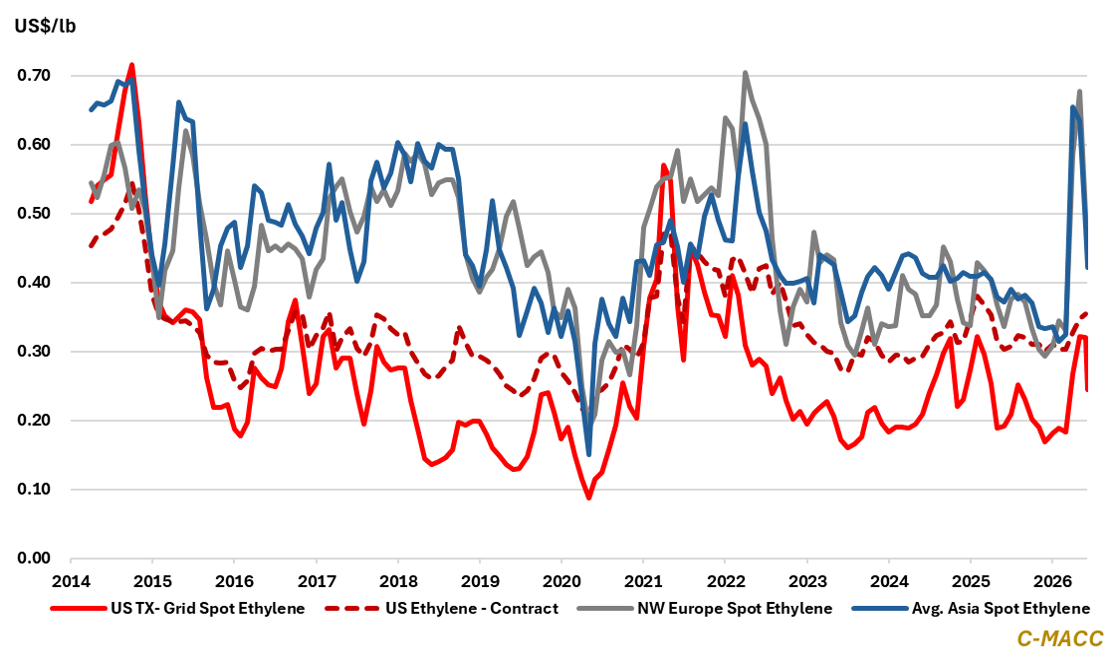

- Olefins: Global olefin prices have retreated from their 1H26 highs, but near-term relief still favors NGL-linked systems as Asia ex-China and Europe net capacity pruning defines the longer-term earnings divide.

- Other Base Chemicals: Global base chemical relief remains selective, with benzene split by region, methanol weakening broadly, and chlor-alkali rewarding those controlling feedstock, logistics, and derivative export flows.

- Agriculture: Global nitrogen prices are holding at elevated levels, leaving secure US producers advantaged as farmer affordability, policy scrutiny, logistics repair, and import timing position to challenge global demand.

- Refining & Biofuels: Global refining strength remains concentrated in flexible coastal systems, with distillate recovery, export access, crude optionality, and biofuel credits outweighing modest softness as product balances stay tight.

Exhibit 1 – Chart of the Day: Global Spot Ethylene Prices Fall as Supply Relief and Softer Demand Weigh Globally.

Source: C-MACC Estimates, June 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!