Daily Chemical Reaction

Staying Selective – Risk-Adjusted Return Strategies in Focus, As Positive Demand Surprises Appear Limited

Key Findings

- General Thoughts: We discuss US chemical sector equity performance, including its sub-sectors and a few of their components, as defensive return-generative positions stay favored amid lingering global demand uncertainties.

- Supply Chain/Commodities: We flag depressed farm income views weighing more on parts of the fertilizer and agricultural chemical sector than others and differing US commodity and specialty chemical fundamental trends.

- Energy/Upstream: Surging global electricity demand expectations are accompanied by concerns with supply ahead of CERA and the need for new solutions, such as those at Issaquena Green Power, to fill the likely void.

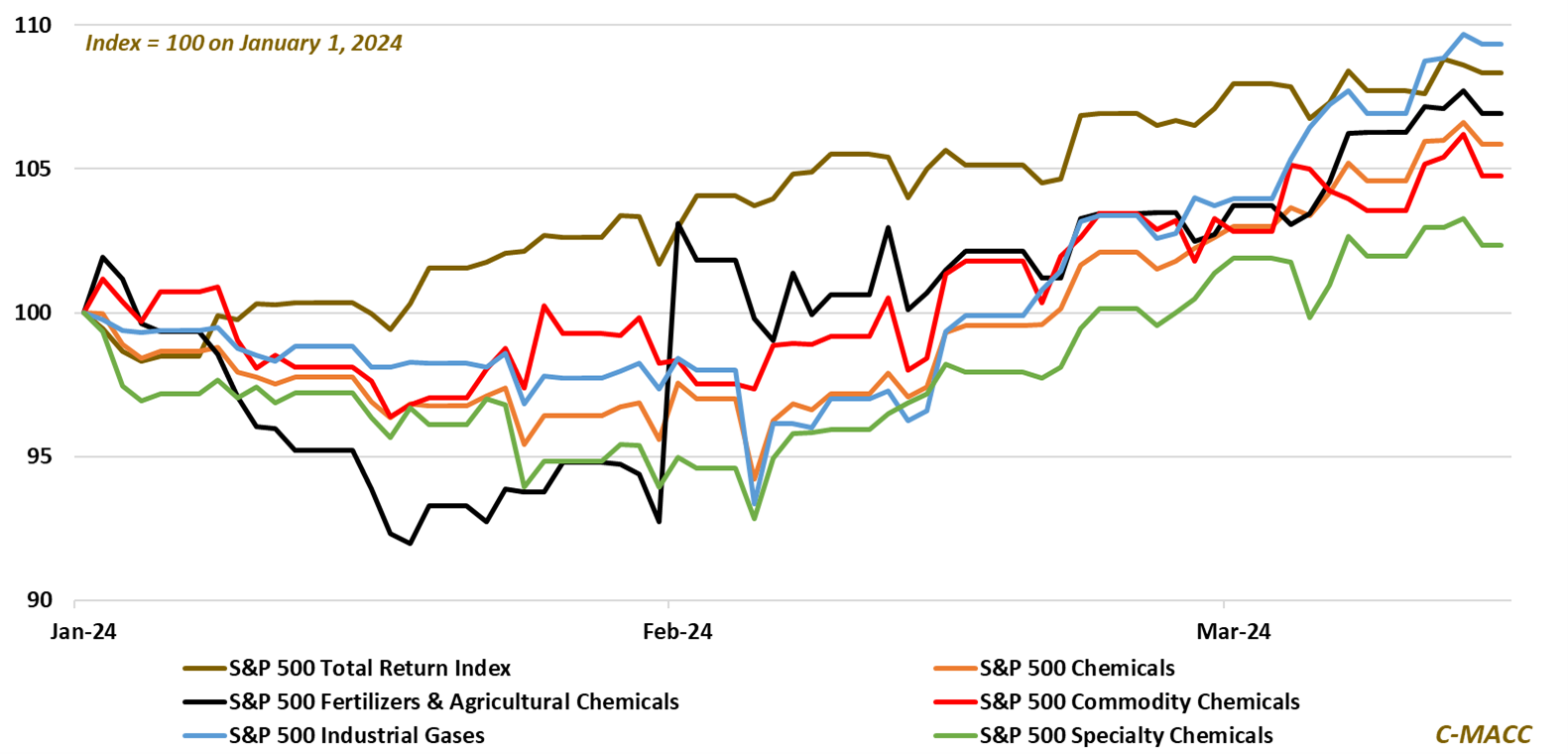

- Sustainability/Energy Transition: US industrial gas equities have outperformed the chemical industry overall and the broader market YTD; however, most of the strength results from Linde’s significant outperformance.

- Downstream/Other Chemicals: We discuss an array of 1H24 economic indicators, implying continued weakness in Europe and China and moderating US economic health – 2Q24 chemical demand appears unlikely to surge.

Exhibit 1: US industrial gas equities have outperformed the S&P Total Return Index and the equities of other US chemical industry sub-sectors YTD, with the equities of specialty chemical companies being the worst performers.

Source: Bloomberg, C-MACC Analysis, March 2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!