The Hydrogen Economy #38

45V – The Red State Rush!

Key Points

- Some of those concerned that a Trump administration would repeal the 45V tax credit for hydrogen are pushing forward with projects in Republican states in the hope that their support will keep 45V in place.

- With so much of the infrastructure and IRA funding targeting Republican-biased states, the only real (non-vindictive) reason to roll back some of the incentives would be anticipated affordability – jobs are being created.

- With the many investment challenges we have outlined for hydrogen, costs, incentive risk, & power availability, it is unlikely, in our view, that we will get much through FID by November – but we may see more plans.

- Texas has momentum, in part because of the significant renewable power investments in the state, but also because of the unregulated utility that covers most of the state and because of possible low-cost CCS.

- Otherwise, we are excited about almost 60 hydrogen-related presentations or forums at CERA, with some of our initial thoughts discussed below – no projects this week – we will double up next week if there are any.

Even before the CERA conference started today, we had a couple of conversations over the weekend about energy transition in general and hydrogen specifically. The first conversation was with an engineer – in the oil sector – and amateur economist, whose view was very simple – how can anyone expect to transition away from fossil fuels without it costing more, and who can afford it? Very straightforward and arguably spot on. The second was around a specific green hydrogen project, which has a lot going for it regarding power availability and price, but the project is still struggling to get off-take agreements supporting funding. The most recent ammonia auction in Europe is encouraging given the high price achieved, but project financers need some sort of fixed return generating offtake agreement to lend the money. A single high auction marker is not enough. The other slowdown on the money front is that none of the green projects work in the US without 45V, and we doubt that anyone will lend until they are sure it will remain. They may be willing to lend without that reassurance, but the terms and covenants would be too expensive for any project to accept. Owning the hydrogen equipment in lieu of debt repayment may leave you with something that no one wants to buy.

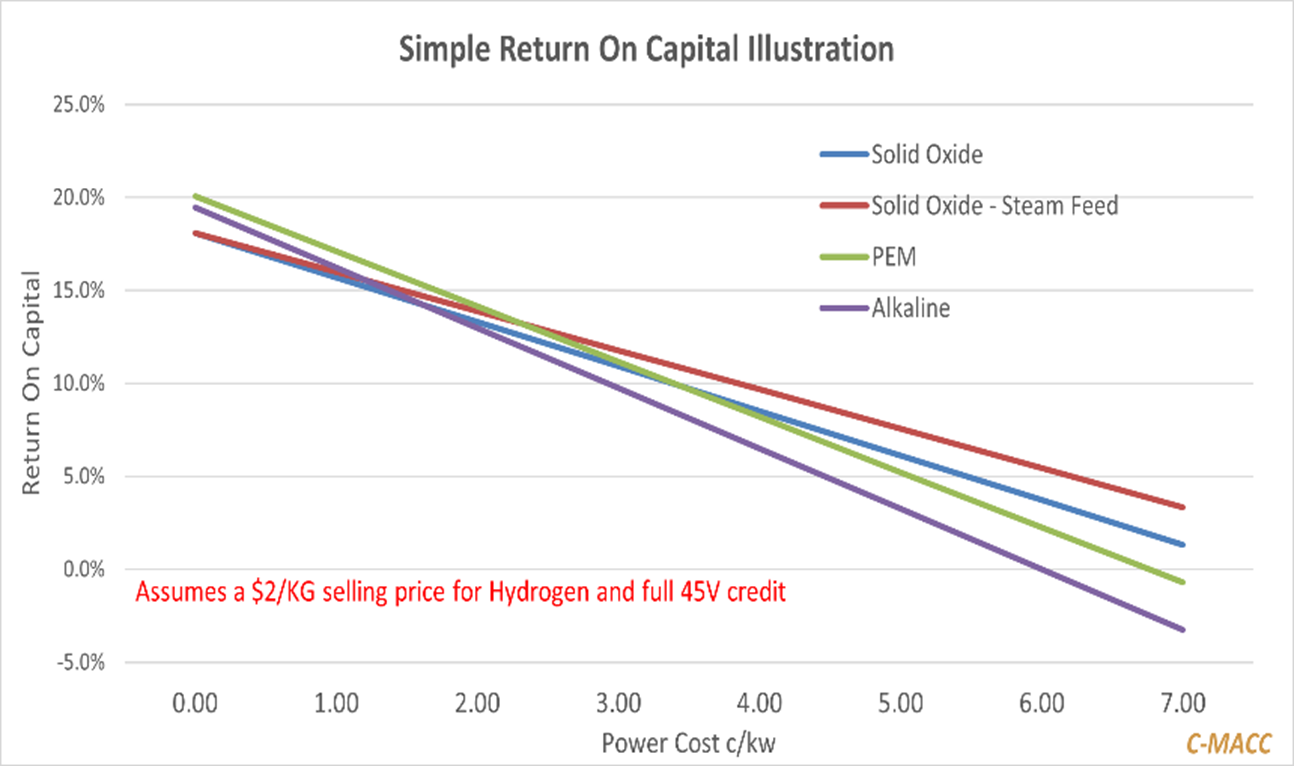

We also got into another discussion about what electrolyzer technology to buy and then from whom. Our advice always starts with the same question – what is your power price? If power is free, buy the cheapest equipment you can get. Free power covers a lot of inefficiencies. However, power is not free in all but a few locations where other significant inefficiencies exist. As long as you pay for power, the efficiency of the electrolyzer matters. We introduced Exhibit 2 when we started this service, and it sits in the appendix of each report. The more expensive the power, the more attractive Solid Oxide technology looks, but if you have free power then Solid Oxide is a waste of money. If we were running a solid oxide electrolyzer manufacturer today, we would be exploring every option to get capital costs as low as the other technologies – at least as low as PEM- because there would not be much of an argument at that point. Offshoring some or all of the manufacture looks like an obvious option. Solid Oxide has another advantage over PEM, which would be a deal closer if capital costs were more aligned, in that it does not have the rare earth dependence that PEM has in its design, and this may matter to those who are concerned about general relations with China. Note that as part of the due diligence that C-MACC has done concerning opportunities for IGP (see release HERE), we have examined waterpower to ammonia opportunities for the Mississippi, and consequently, we have got into the weeds around which electrolyzer technologies make the most sense in certain situations. Even with the very low power prices we think we can generate at IGP, we would still choose Solid Oxide for ammonia because of the heat synergies. If you were generating hydrogen for a process that did not generate excess heat, you might choose a cheaper and less efficient electrolyzer. Just to show the importance of capital costs, in Exhibit 2 we remind clients of how much returns improve with lower capital costs. The real opportunity here is for Solid Oxide to close the capital cost gap.

Exhibit 1: The winners and losers switch positions as power prices move.

Source: Corporate reports, client discussions, C-MACC

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!