Daily Chemical Reaction

Global Chemical Sector Restructuring & Strategic Activity to Stay High, Europe & Asia Remain in Focus

Key Findings

- General Thoughts: We provide thoughts following our meetings at CERA and AFPM, as global chemical producers continue to stress the benefits of integration, consolidation, and needed Europe and Asia Ex-China restructurings.

- Supply Chain/Commodities: We discuss chemical producer 2H24 return concerns in Europe and Asia Ex-China, despite some recently seeing feedstock relief, and highlight the March US propylene contract price settlement.

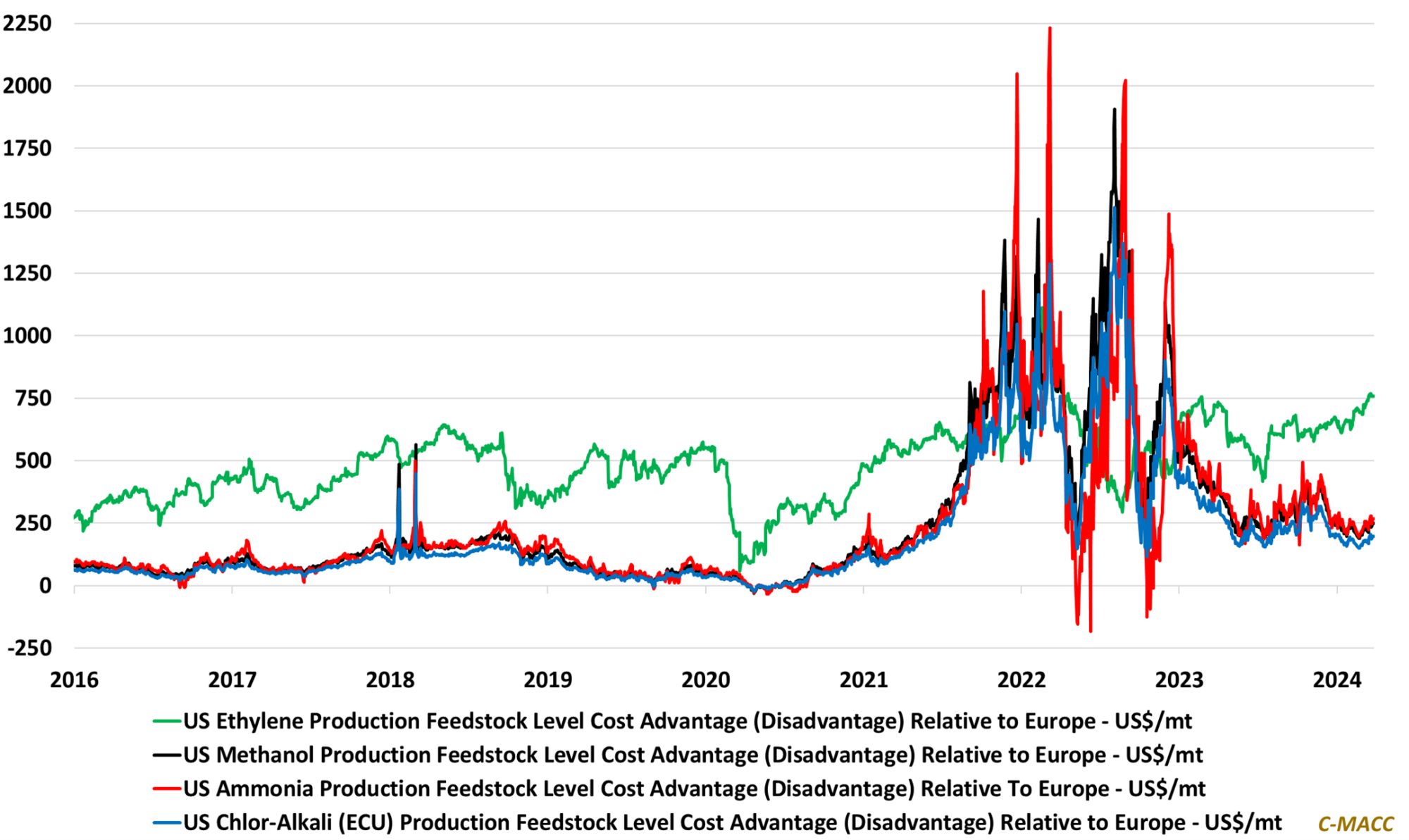

- Energy/Upstream: We display and discuss Brent crude oil and US, Europe, and Asia natural gas price movements in 1Q24, which support our findings in Ex. 1, and we highlight substantial strength in US refinery margins YTD.

- Sustainability/Energy Transition: The ability to source cheap, consistent green power remains at the heart of most green product ambitions, however, the prospect of obtaining it is proving increasingly challenging for most.

- Downstream/Other Chemicals: We highlight a modest uptick in European export sentiment though it remains much lower than 2017-2019 levels, and the recent drop-in freight rates between China and the US and Europe.

Exhibit 1: The US ethylene production cost advantage relative to Europe has risen YTD and YoY, while its feedstock-level cost advantage in methanol, ammonia, and chlor-alkali is mostly unchanged YTD but notably lower than 1H23.

Source: Bloomberg, C-MACC Analysis, March 2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!