C-MACC Sunday Thematic and Weekly Recap

All Eyes Back On China Again – 2024 Growth Is The Focus

- If the most recent, post New Year, Chinese demand data for polymers is more than just a one-off, we may face another year where confidence vanishes in the global market, driving losses again in Europe and Asia ex-China.

- With China still building, demand growth below expectations means more local surplus and more pricing that exposes high-cost producers in Japan, S. Korea, and Taiwan, but the ripple effects will flow through to Europe.

- The risk for North America is that export demand weakens without more aggressive pricing aimed at driving more immediate shutdowns, and it will be challenging to do this without negatively impacting US prices.

- The broader consequence of weaker-than-expected Chinese growth in 2024 will be more export surpluses and the deflationary pressure that brings. Calls for China to export fewer “clean” products will fall on deaf ears.

- Otherwise, we see more evidence of European pessimism, look again at some of the emerging power availability challenges, make some investment choices for 2Q, and discuss costly hydrogen and climate change.

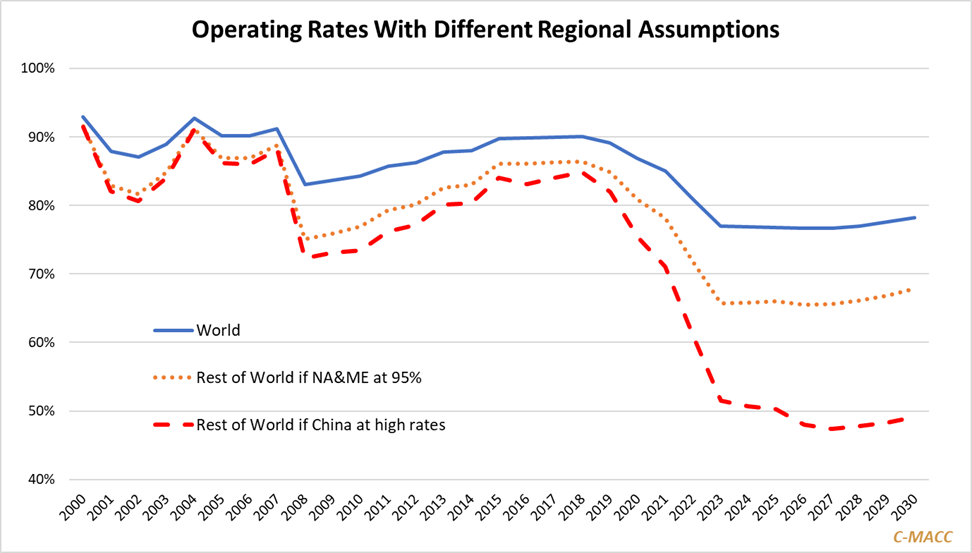

Exhibit 1: Average global ethylene operating rates disguise the challenges in regions not feedstock advantaged – especially, if that group includes a feedstock-subsidized China.

Source: Bloomberg, C-MACC Analysis, March 2024

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!