C-MACC Sunday Thematic and Weekly Recap

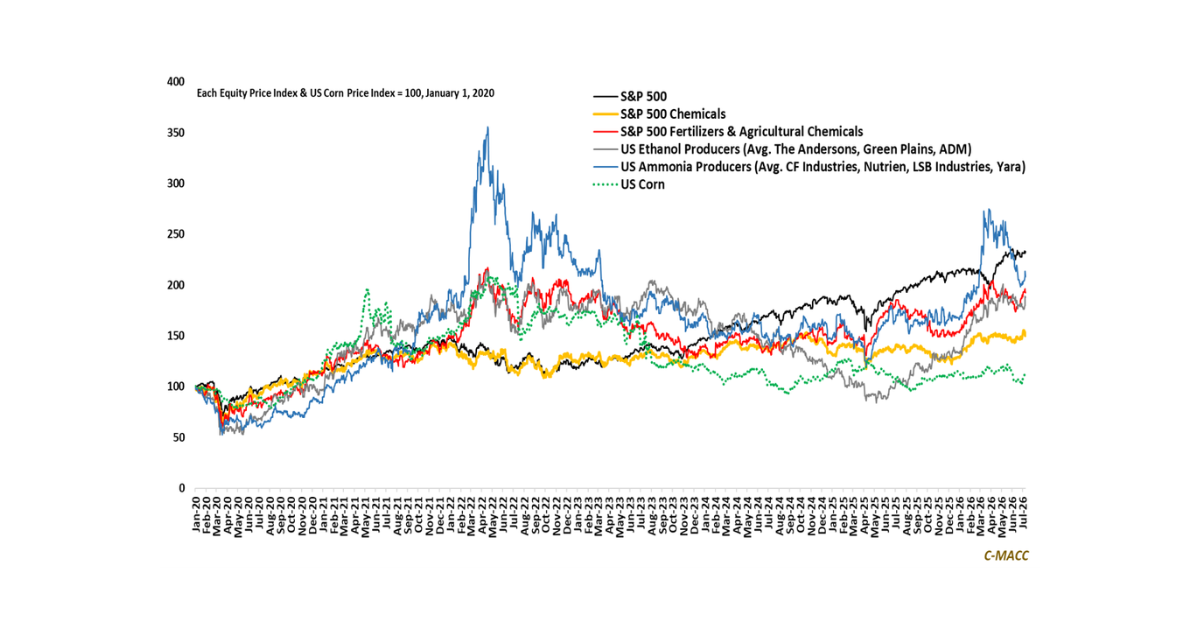

A Food Inflation Upside Surprise In 2025 – We Would Not Bet Against It

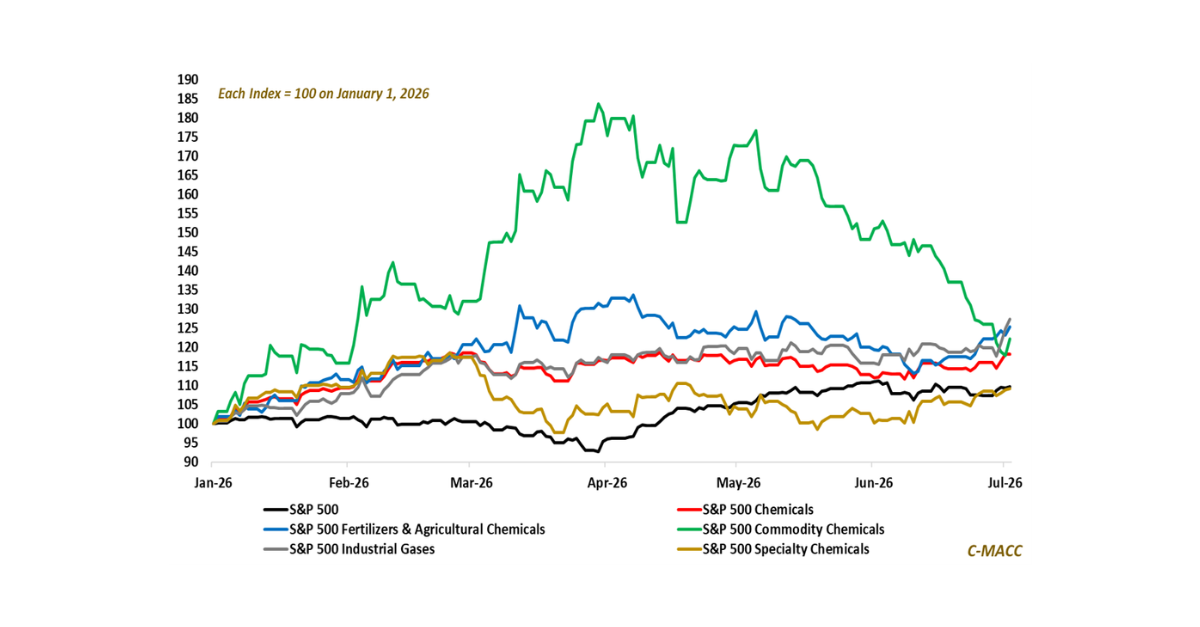

- We struggle to find a compelling case for anything to buy in chemicals this quarter, except the agriculture space – weather surprises will affect crop production negatively and global tension could raise demand (hoarding).

- But what is good for the agricultural chemicals sector is often bad for the consumer as it means higher food input price and more food inflation. The farmer sees better prices but must spend more on inputs.

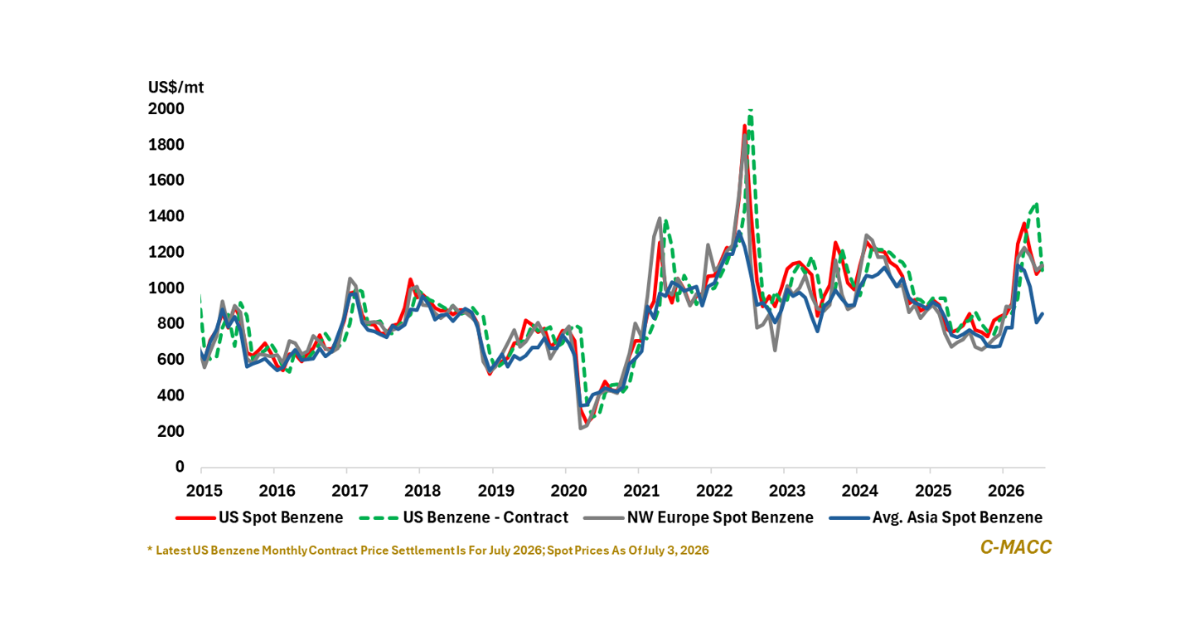

- Nitrogen fertilizer makers in the US have a significant cost advantage, both because of the low natural gas price but also from cheaper power, and ammonia demand could get a boost from some early fuel trials.

- The other wild card for ammonia would be the signing of any longer term take or pay agreement for blue hydrogen, as this could put a floor under ammonia pricing which may limit some of the cyclical downside.

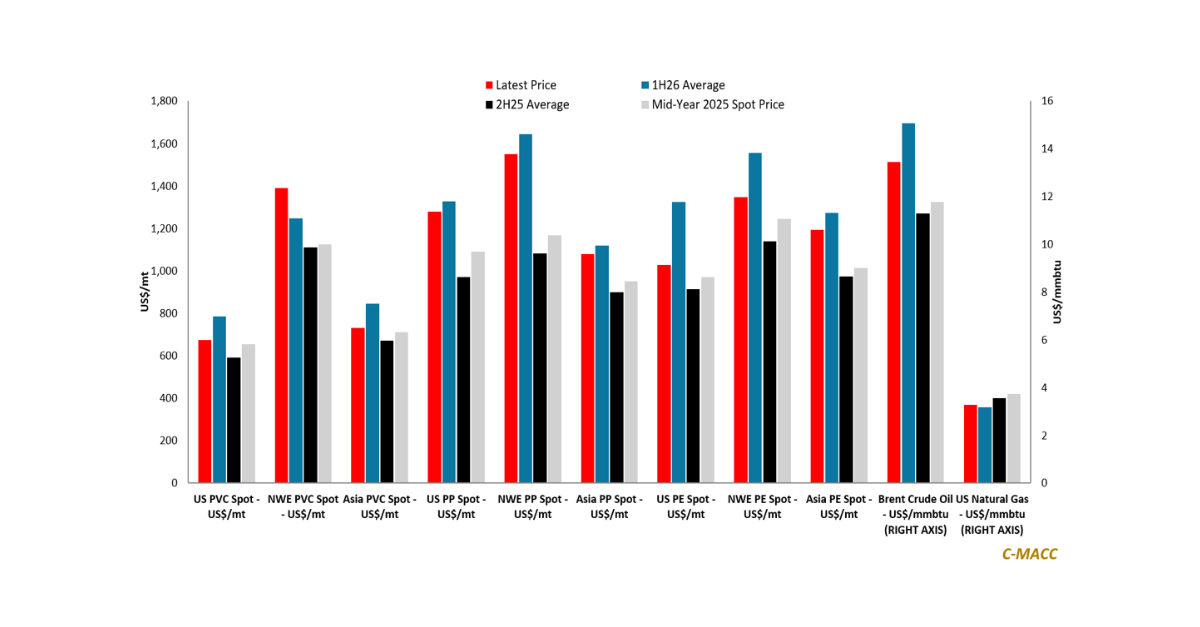

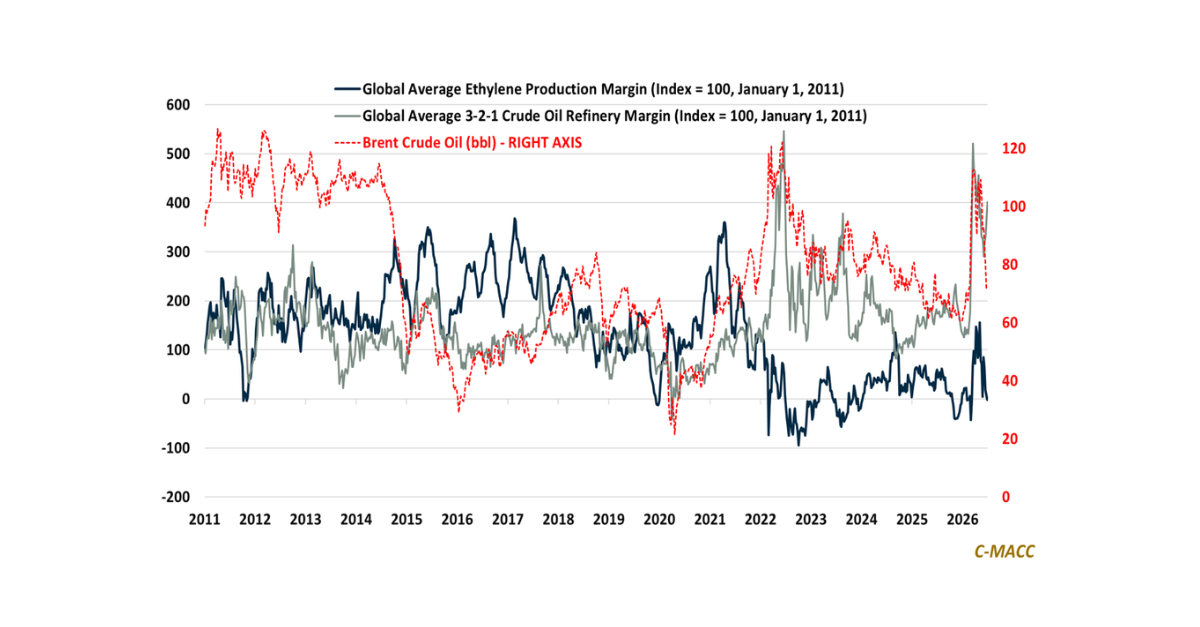

- Otherwise, we look at the expected mood of those reporting earnings in the coming weeks, the compelling cases to invest in new ethylene capacity, despite oversupply, Chinese deflation, and hydrogen economics.

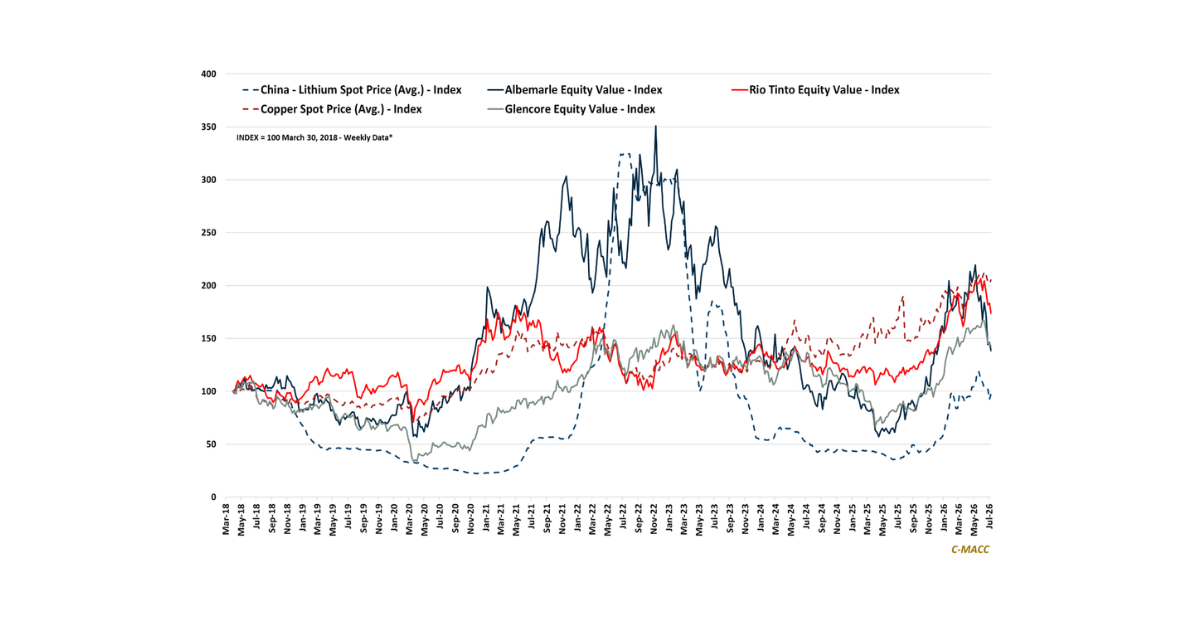

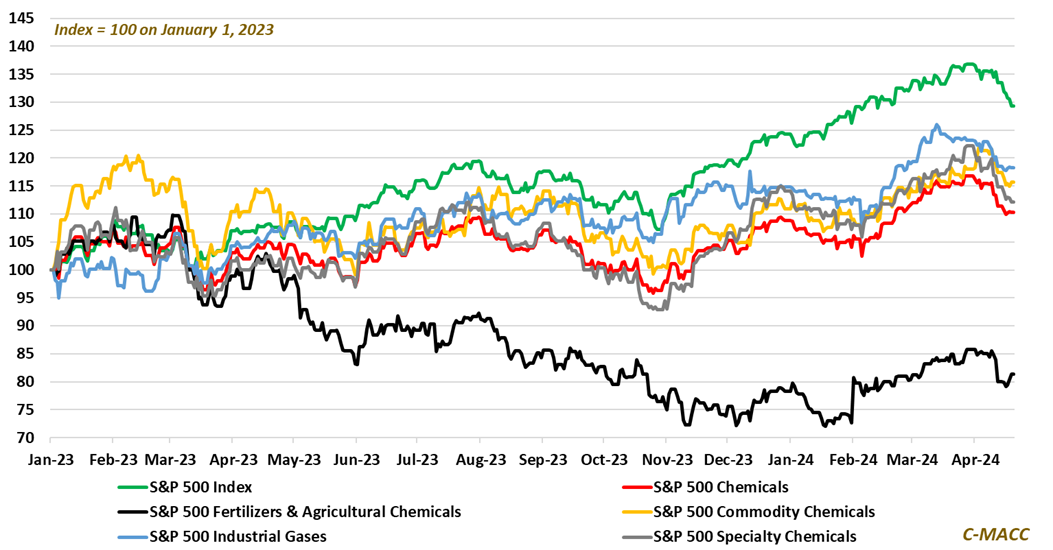

Exhibit 1: The Ag underperformance came after a year of strong outperformance in 2022.

Source: Bloomberg, C-MACC Analysis, April 2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!