Weather We Should Hold More Inventory – Seems So!

Key Findings

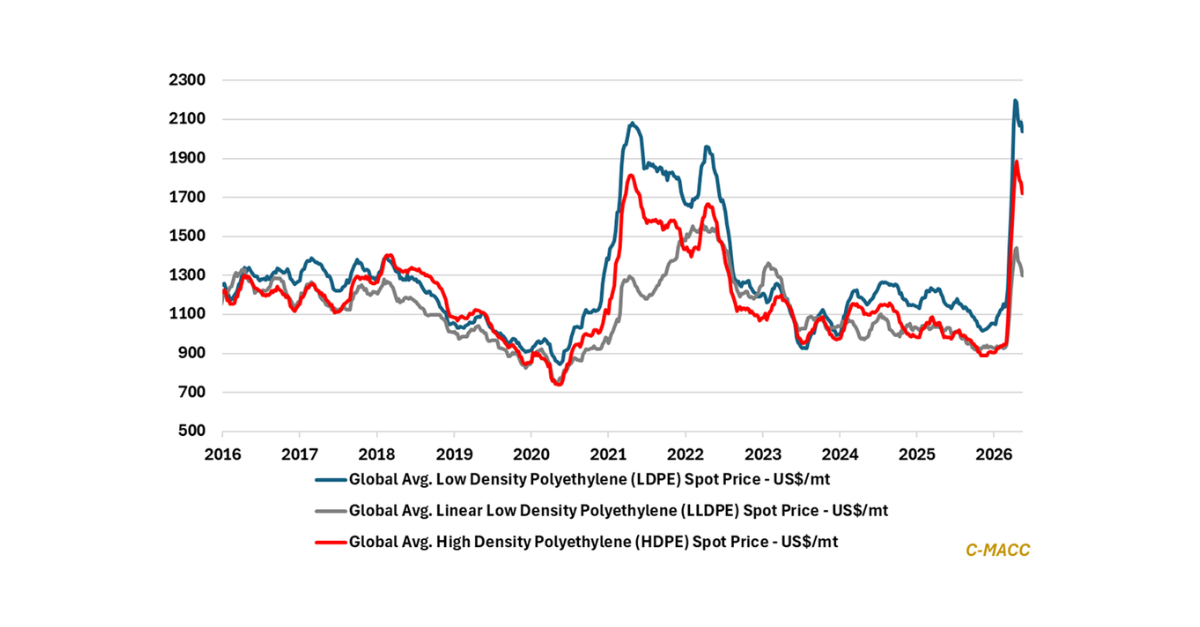

- General Thoughts: US spot polymer prices, on average, have increased from mid-2Q24 lows amid a mixture of production and logistic issues and efforts to stock inventory as some anticipate a record US hurricane season.

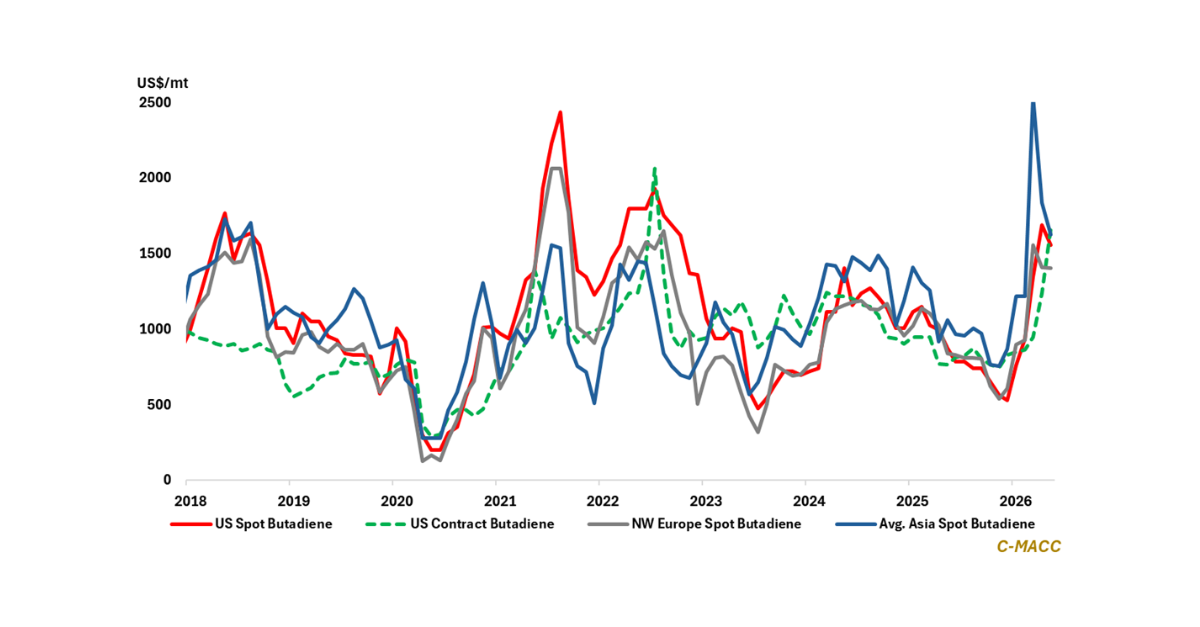

- Supply Chain/Commodities: We discuss US spot PGP price strength in June as production issues persist, US polymer export market support, and why we see US polymer price weakness ahead absent sizable outages.

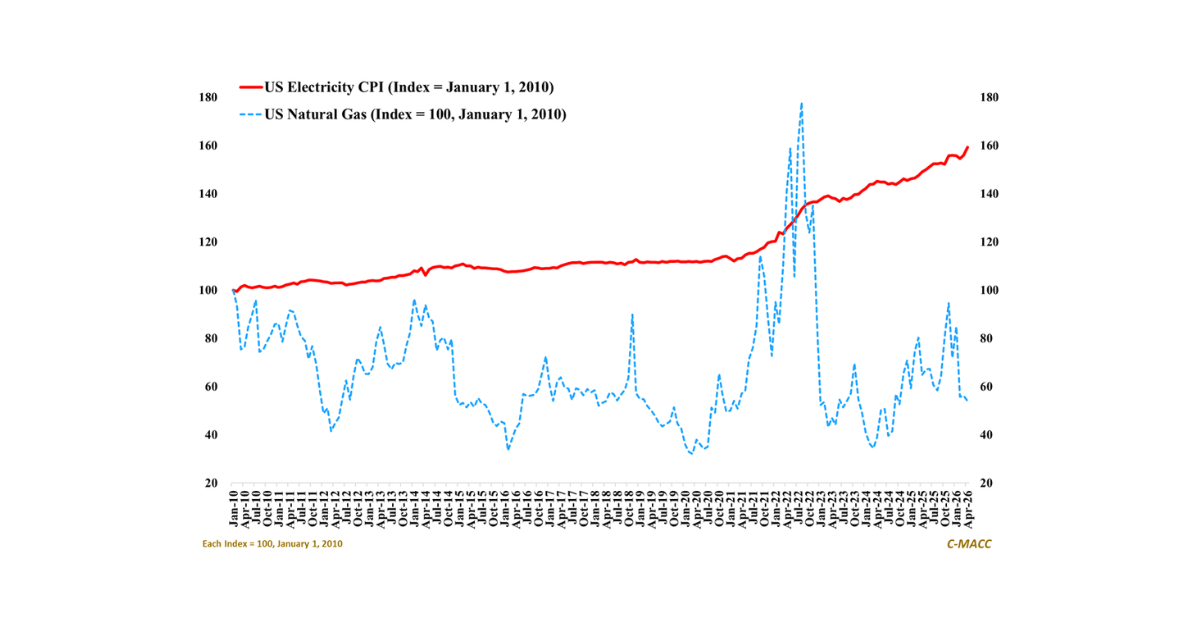

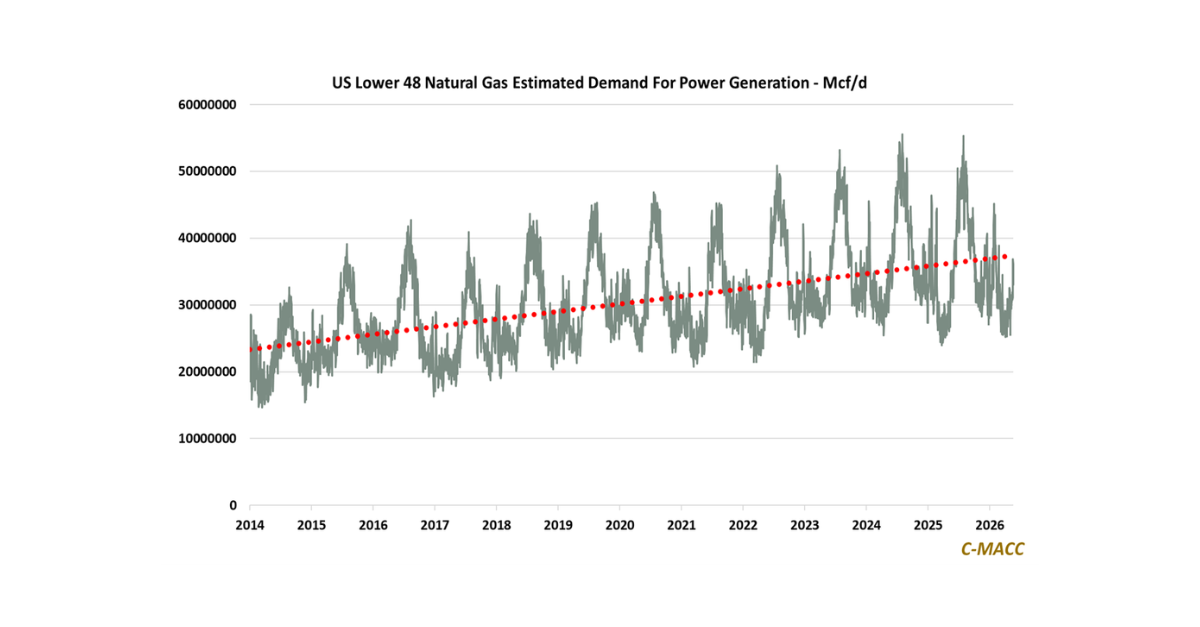

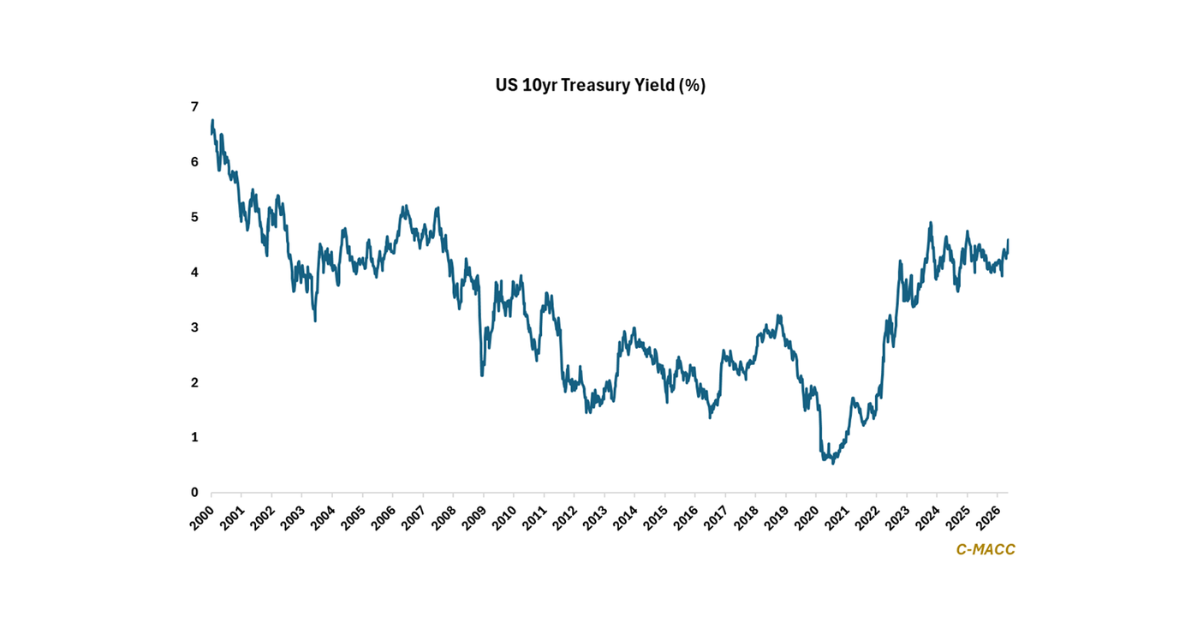

- Energy/Upstream: We highlight YTD price support and less volatility in Ex-US naphtha prices relative to crude oil and falling US ethane values relative to US natural gas, which benefits North American ethylene producers.

- Recycled/Renewable Polymers: We discuss circular product initiatives at several plastic producers, each with initiatives underway in advanced recycling, and highlight the different chemical recycling technologies.

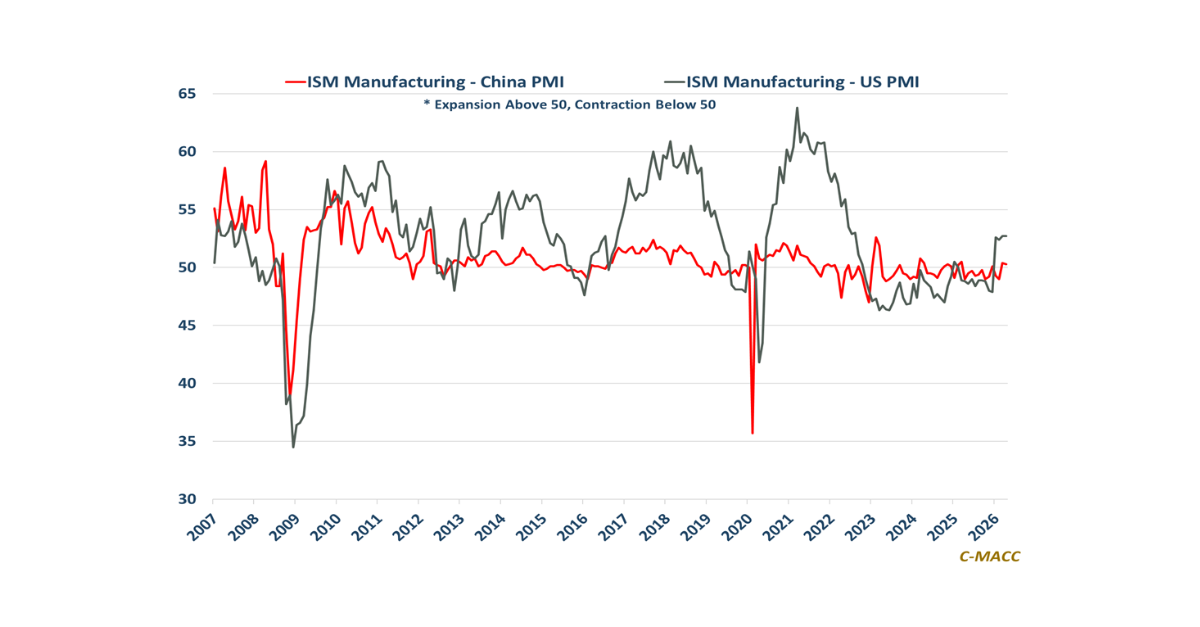

- Downstream/Other Chemicals: We discuss the May CPI postings for the US and China, following our research from yesterday, and discuss the greater packaging market drivers of global PE demand relative to PP and PVC.

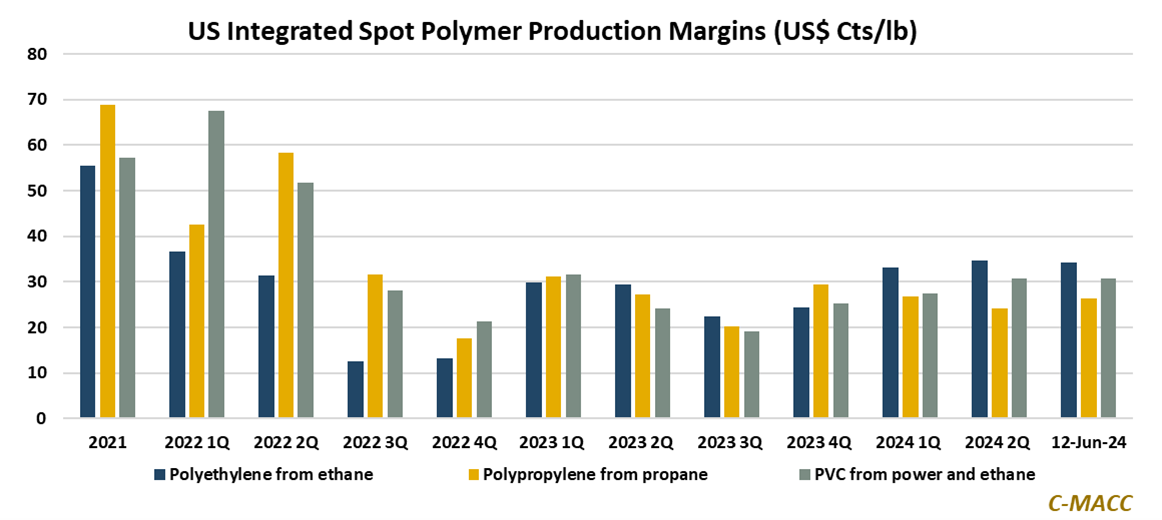

Exhibit 1: US integrated polymer margins, on average, have generally held up or improved upon levels seen in 1Q24.

Source: Bloomberg, C-MACC Analysis, June2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!