Daily Chemical Reaction

Less Constructive on Agriculture Sector Equities Than Global Crop Markets After A Weak 2024 – Corn Looks Interesting!

Key Findings

- General Thoughts: We discuss the US agriculture sector ahead of 2Q24 business updates, considering US corn prices is near a YTD low – we are more constructive on crop price support than agriculture sector equities overall.

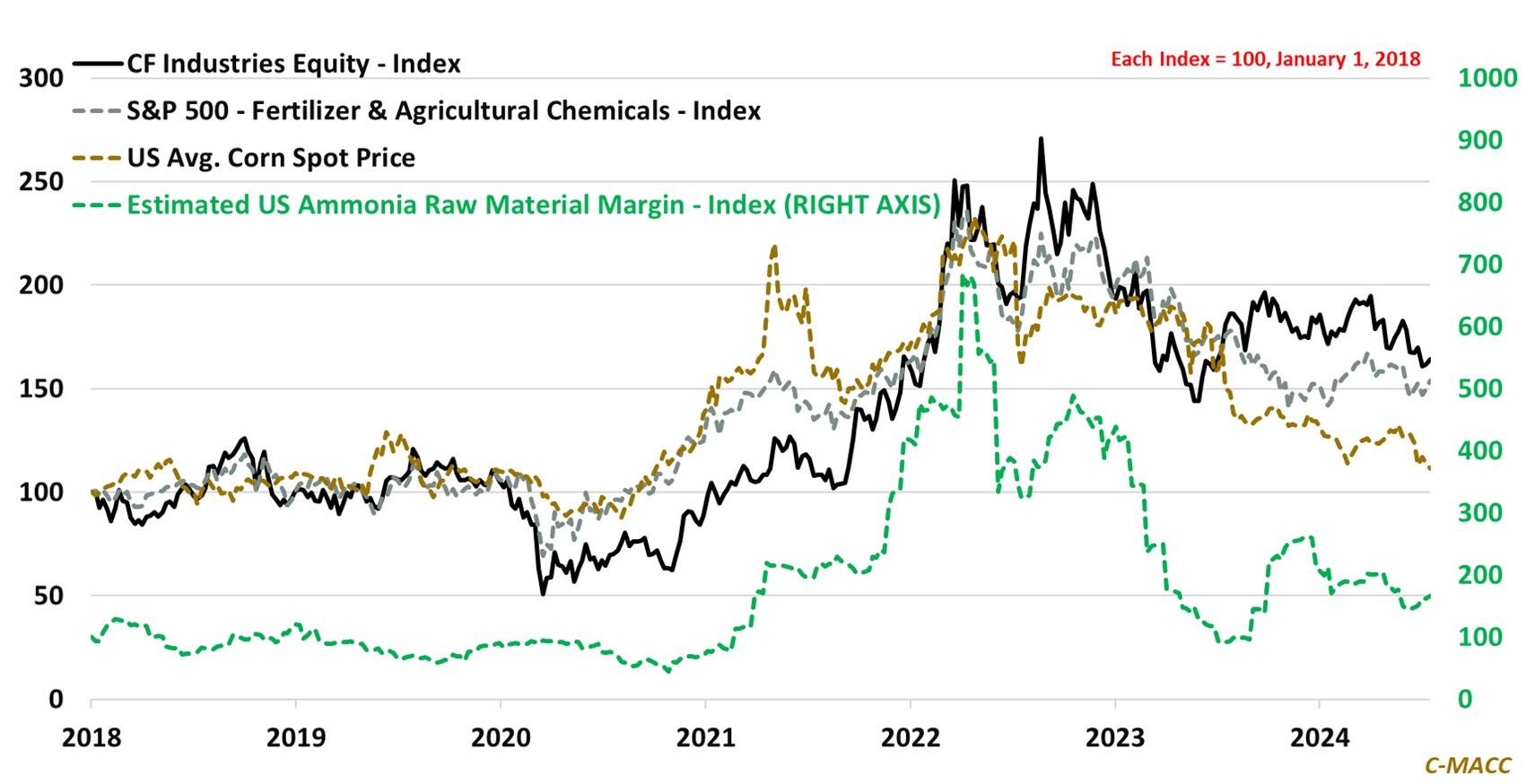

- Supply Chain/Commodities: We comment on apparent distortions being seen in agriculture and chemical sector equities relative to their historic relationships, and generally comment on an uptick in copper growth investments.

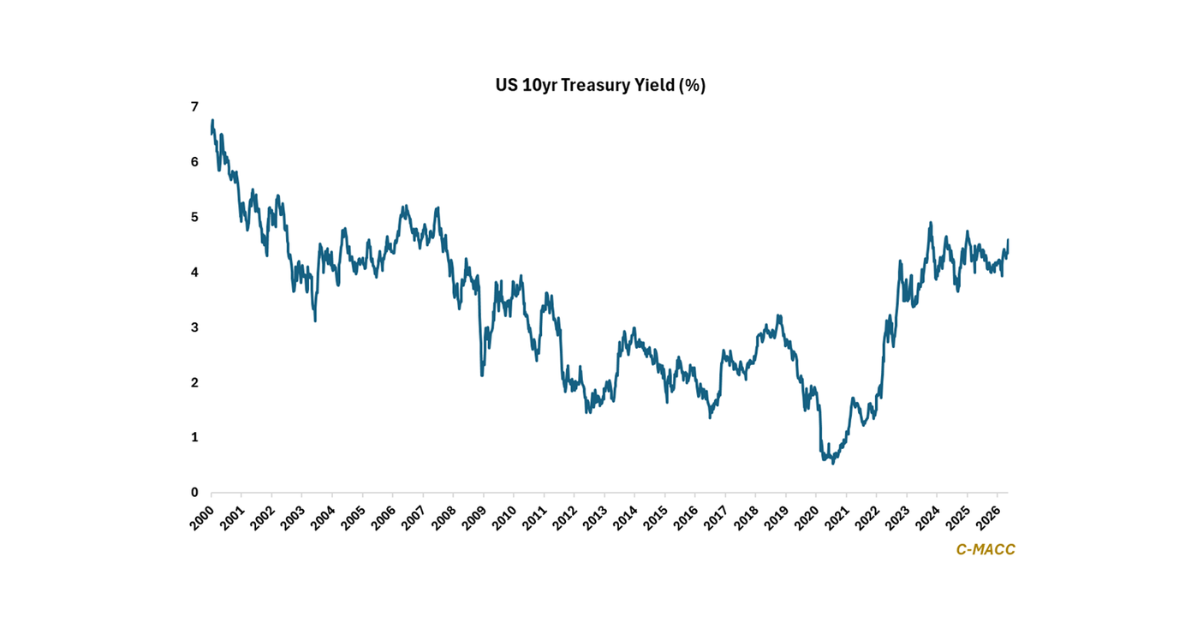

- Energy/Upstream: We highlight the build-out of US LNG capacity, the still widespread between Ex-US natural gas and US natural gas relative to pre-COVID levels, which is benefiting US chemical producers, including ammonia.

- Sustainability/Energy Transition: We continue our focus on carbon credits, noting that many industries will struggle to meet low carbon goals without a robust credit market. We note a turn in SAF activity – bullish for corn.

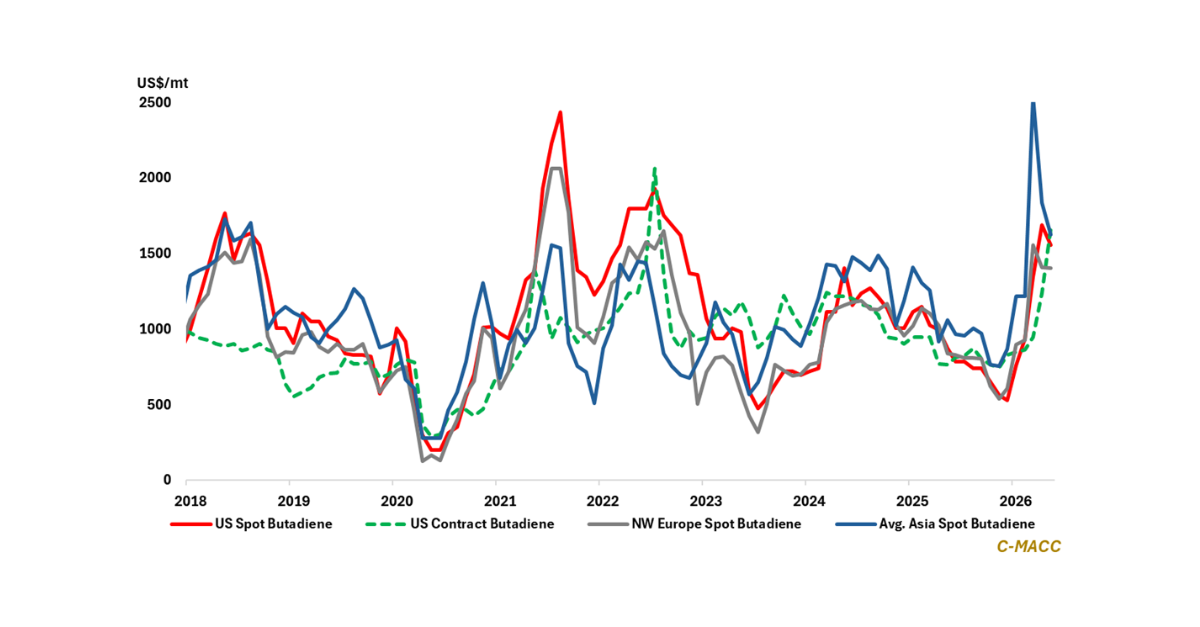

- Downstream/Other Chemicals: We highlight US crop prices, showing the underperformance in corn relative to soybeans, as compared to 2019 levels, and comment on chemical end market trends worth notice this week.

Exhibit 1: US agriculture sector equities have held up better than US corn, near a 3-yr low, and ammonia margins.

Source: Bloomberg, C-MACC Analysis, July 2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!