Daily Chemical Reaction

Global Sustainability Efforts See Pull-Backs, While Other Corporate Strategies Pause Amid Shifting Terrain

Key Findings

- General Thoughts: We discuss global chemical and associated market 2Q24 reports, with many 2H24 outlooks expecting global demand improvement to help counter their disadvantaged positions likely to be proven wrong.

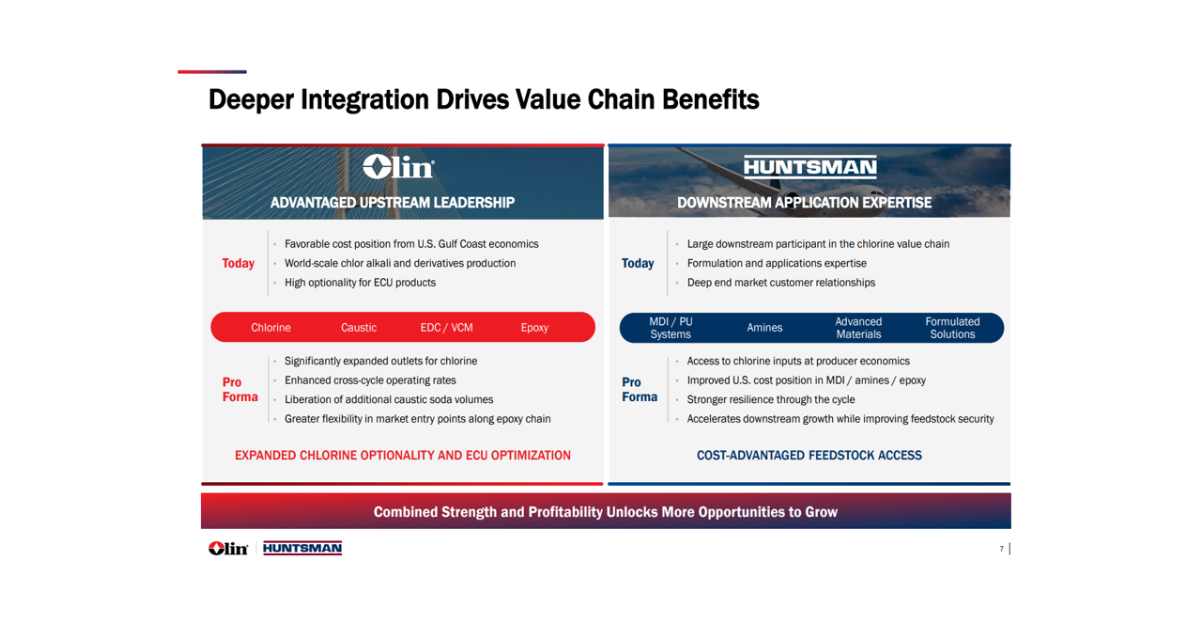

- Supply Chain/Commodities: We favor low-cost global production positions amid oversupplied product markets with access to the global export market, and we discuss Olin Chlor-alkali and BASF battery material ambitions.

- Energy/Upstream: Asia natural gas prices have ticked higher relative to European and US levels and Brent Crude oil. The drop-off in Asia LNG import contracts is tactically sound but risks a scramble to lock in supply later.

- Sustainability/Energy Transition: We agree with TotalEnergies CEO’s view that firm power sources are needed to balance those from intermittent sources, and we also flag Neste and Eastman sustainable business updates.

- Downstream/Other Chemicals: We highlight the Eastman 2H24 views of its end markets, the decline in European manufacturer export expectations in July, and mixed global stimulus initiatives to spur consumer demand.

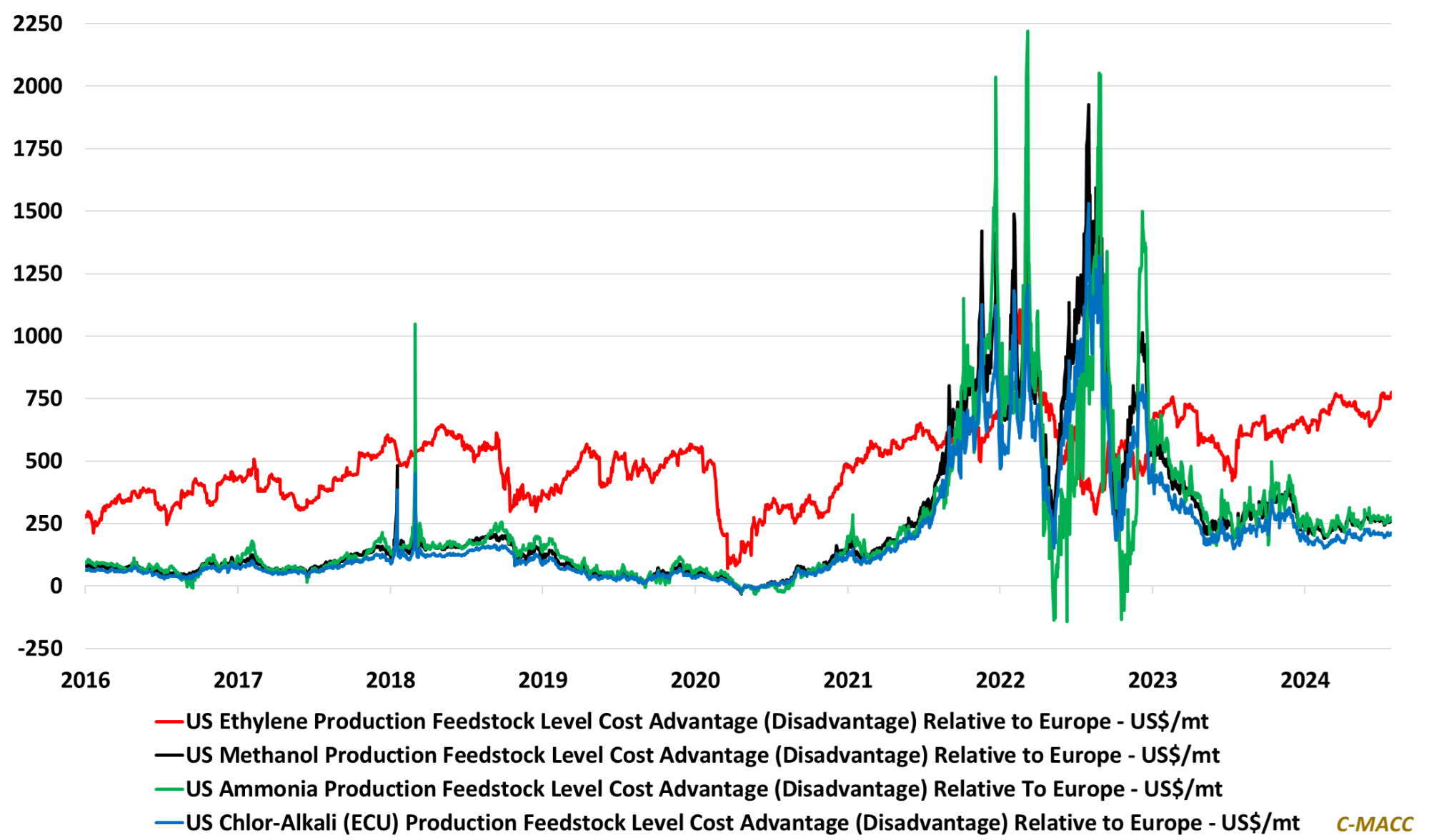

Exhibit 1: The US ethylene production cost advantage relative to Europe has risen since the start of 2024, while its cost advantage in chlor-alkali, methanol, and ammonia is mostly unchanged YTD at the feedstock level.

Source: Bloomberg, C-MACC Analysis, July 2024

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!