C-MACC Sunday Theme and Weekly Recap

Covestro: A Unique Situation or the Start of Something Bigger

- The likelihood of a wave of M&A following ADNOC/Covestro is not high, as valuations are not aligned for deals that would make sense, and few have the deep pockets to pay the cash that most sellers would want.

- Some mergers of equals deals look interesting, but as chemical earnings fall, multiples today suggest that big oil buying chemicals look dilutive, even for the highly valued oil majors in the US. Europe could see mergers.

- The ADNOC logic beyond expanding downstream into chemicals through JVs and the selective pick up of assets is still not clear (yet). The endgame may involve consolidating Borealis, Borouge, and possibly OMV and Nova!

- The key will be derisking deals for valuations that could be quite volatile in a World where global trade is under threat, and climate-related costs are uncertain, as are regulatory backdrops around climate.

- Otherwise, we look at North America’s very profitable polyethylene business (especially Canada) versus the weakness elsewhere. We question the solvency of Plug Power and discuss the confused US ESG backdrop.

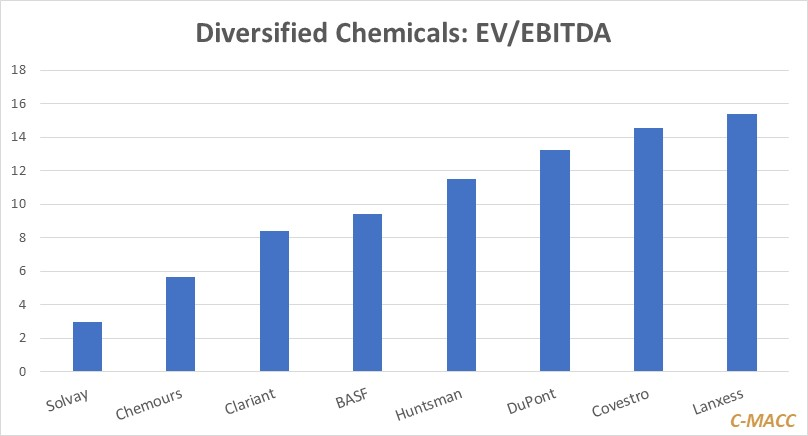

Exhibit 1: Lanxess valuation is a function of very low EBITDA and plenty of debt. The Covestro bid is key.

Source: Bloomberg, C-MACC Analysis, August 2024

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!

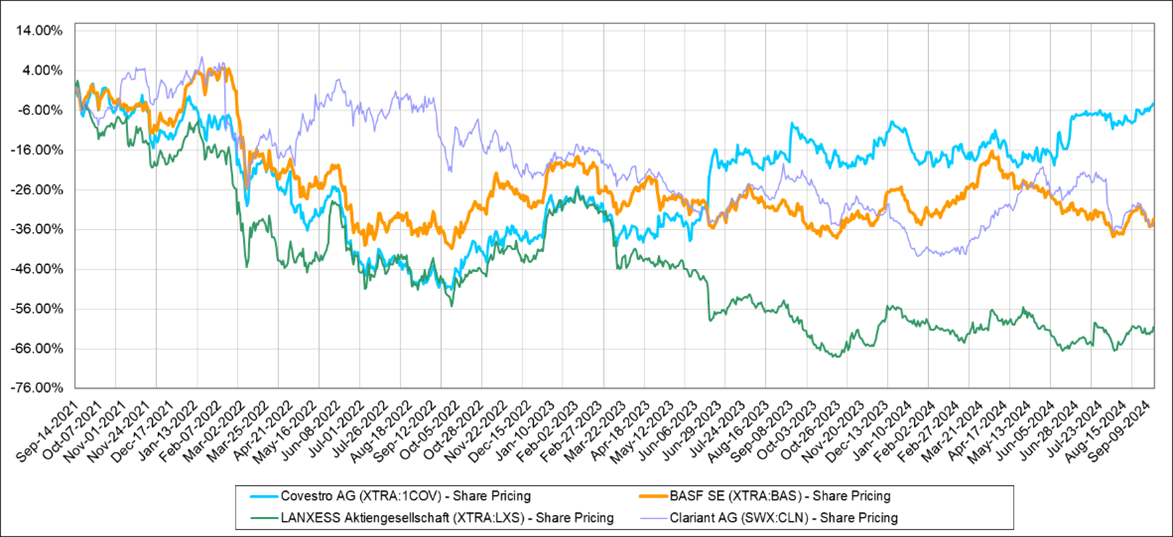

With the latest offer from ADNOC to buy Covestro, we may be seeing a marriage at the end of a courtship that has taken a long time. But it raises two questions: What is ADNOC’s endgame, and is this the start of a larger M&A trend? As we have noted in prior work, at this point it would be career suicide for the management and board at Covestro to turn down the deal as, without another bid, the share price has significant downside to reach levels that reflect the rest of the European market for intermediate and diversified chemicals, as implied in the chart below.

Exhibit 2: The general weakness in Europe is reflected in most stock values – the ADNOC bid is supporting Covestro

Source: Capital IQ, C-MACC Analysis, September 2024

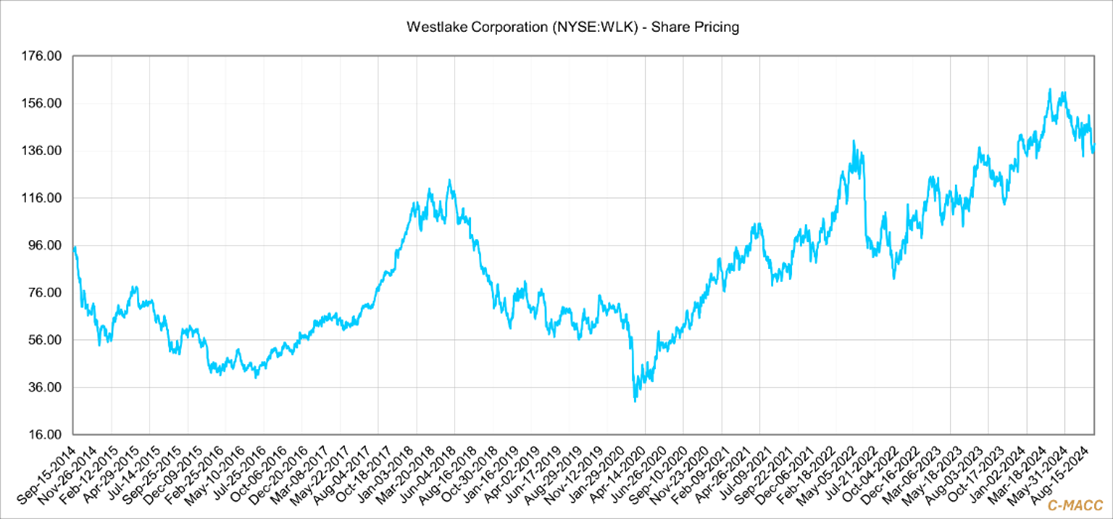

Expecting more deals like this is probably a long shot, even if the markets need significant restructuring, especially in Europe. ADNOC is paying a lot and paying in cash, and as such is taking a lot of market risk, especially with the very large part of the Covestro portfolio that is in Europe and especially in Germany. Cash deals are challenging in markets like these as the buyer needs to be able to fund the acquisition without taking on too much capital structure risk – the Dow/Rohm and Haas deal in 2008/2009 is the best example of how market fundamentals can turn what looks like a good deal very sour very quickly. The way to risk-adjust valuation challenges is to trade for stock rather than cash, but sellers always want to give their shareholders certainty, and the Dow experience is still a recent industry lesson. Note that when Westlake bid to buy Axiall, the first offer was stock or cash or a combination of both. Axiall insisted on cash, but with hindsight, the stock deal would have been meaningfully better for Axiall shareholders. The benefit is understated in the chart below as a stock deal would have meaningfully increased the liquidity of Westlake’s stock at the time and this would have likely added more momentum. Axiall understood this, but the “bird in the hand” view of cash was compelling and risk free.

Exhibit 3: Westlake’s share price doubled in the two years from the June 10th, 2016, Axiall deal announcement

Source: Capital IQ, C-MACC Analysis, September 2024

There is inevitably more M&A to come but it will be challenging. Companies looking at strategic options against the current chemical, polymer, and energy transition backdrop, will all be looking at M&A as part of that strategy review, but the potential variables in forecasting today drive some quite large ranges of outcomes, that it is highly unlikely that many companies have similar views. They may all have scenarios that overlap, but as a seller you are not going to agree to a deal that reflects your worst fears and as a buyer you should not pay up in the face of heightened risk – although this is what ADNOC appears to be doing. Some will see M&A as part of a growth strategy, and others will be looking at survival, contrasting different agendas that exist within diverse groups of companies with different end market and geographic exposure. As we look at the Dow earnings revision last week, we see one of the complicating factors, which is the movement in valuation, and some of valuation divergence that exists today. Covestro’s shareholders are getting cash, and others in the sector that might be acquisition targets are also likely to want cash, while chemical companies looking at consolidation will want to pay in equity because of some of the significant risks in the business today. The oil industry has done a lot of stock-based M&A recently, which reflects some of the valuation discounts in the market compared to reserve values – Pioneer shareholders, for example, were attracted by getting ExxonMobil’s reserves at a discount.

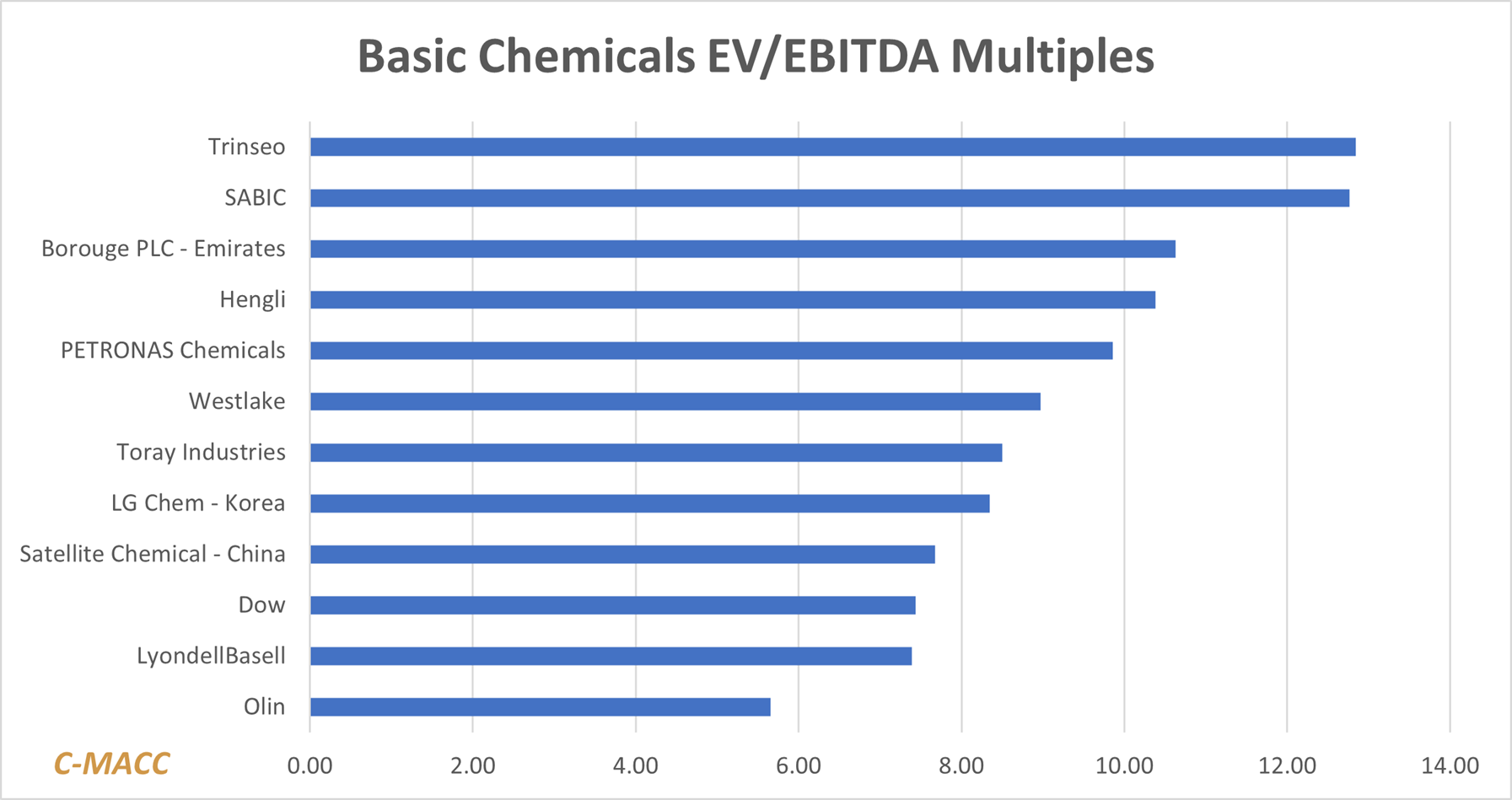

Exhibit 4: Some of these valuations reflect very low EBITDA – Trinseo for example. SABIC and Borouge are majority owned by others, while the Chinese producers are seeing earnings shrink

Source: Capital IQ, C-MACC Analysis, September 2024

We have discussed at length that one of the challenges for the chemical industry going forward will be the desire of oil companies to integrate downstream, with most highlighting chemicals as the most interesting demand growth sector for hydrocarbons from here. As the chemical sector has seen earnings fall, some stock prices have held up better than in past cycles, in part because of the strong base level of earnings in North America – see below – and in part because of the overall strength of the US stock market. As such, it is becoming less attractive for oil and gas companies to buy chemical assets, despite the ADNOC move. Only Olin has a value that might create an accretive deal for the higher valued oil companies, and none of them would want Olin as it does not drive an integration story – US and chlorine.

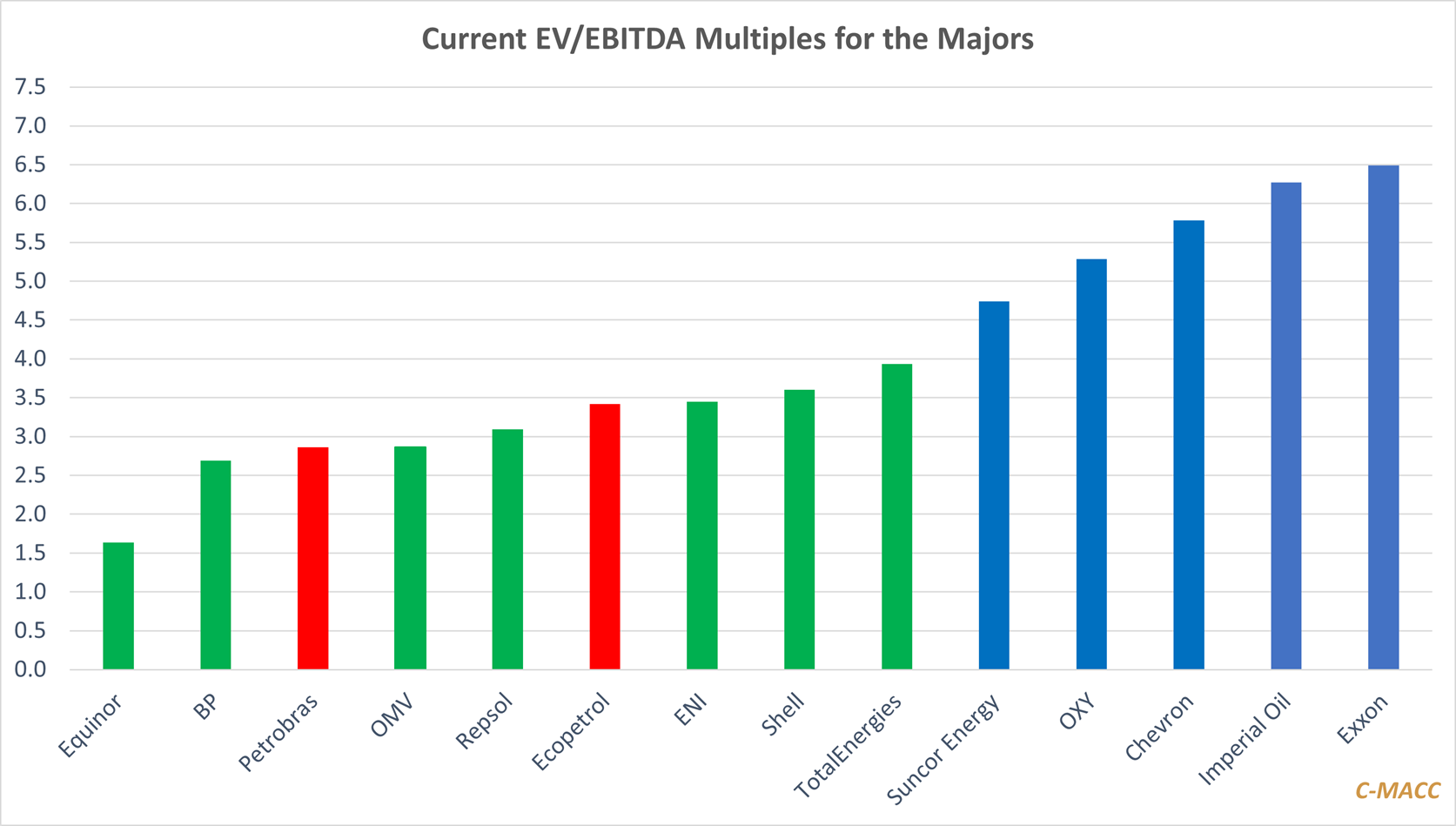

Exhibit 5: Oil valuations are lower than chemical valuations for the most part and most chemicals company shareholders would not want oil company equity.

Source: Capital IQ, C-MACC Analysis, September 2024

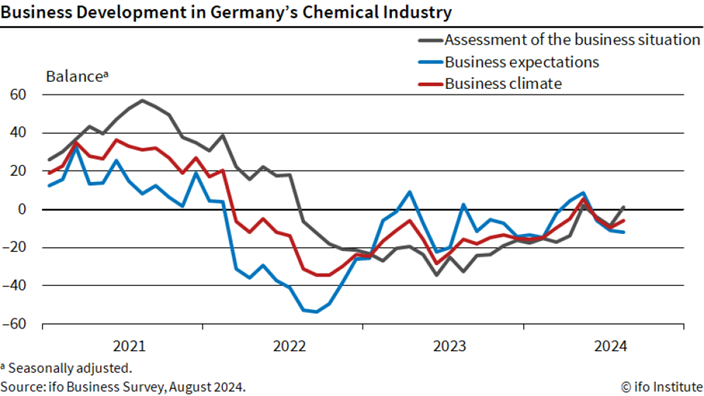

Coming back to ADNOC’s motivation, it is worth noting that the more ADNOC pays the more determined the company should be to drive synergies from the deal. The challenge that ADNOC faces is that it does not own enough of any of its other major chemicals’ assets, Borealis, Borouge, and OMV, to consolidate – so you have four different companies with assets that could be run well as an integrated portfolio, all operating independent businesses with potentially redundant overheads within business management, head office expenses and other common SG&A. Add to this a number of local JVs in the UAE and the moves in fertilizer. This may be more important than any synergies that can be gained by optimizing hydrocarbon flows through the businesses. ADNOC is offering to buy a company that has 12% of its revenue in Germany and as much as another 35% in Europe (not broken out that way in Covestro’s financial reports – so this is an estimate). All our work and all the macro signals suggest that many segments of the European industry are in trouble, and we have noted a couple of recent headlines about pullbacks in Germany in general and in the auto sector specifically. The Auto market is critical for Covestro. The second chart below shows another negative sentiment chart for Germany – one of a series that have been progressively more bearish since the Ukraine war began and energy prices spiked. It is not just energy that is a challenge in Germany – other costs are also high and as the region and country is aggressively focused energy transition, support for the industrial based in general and chemicals specifically is hard to find.

As noted above, this offer looks like a very good deal for Covestro shareholders, and they would be foolhardy not to take it, in our view. ADNOC may be playing a long game here, but lots of other pieces need to fall into place for the company to get real value.

- Adnoc makes formal offer for chemical company Covestro for $16bn

- Dow Shares Retreat on Weak Forecast for 3Q

- Saudi Arabia fosters closer ties with China; Aramco, Chinese firms sign fresh deals

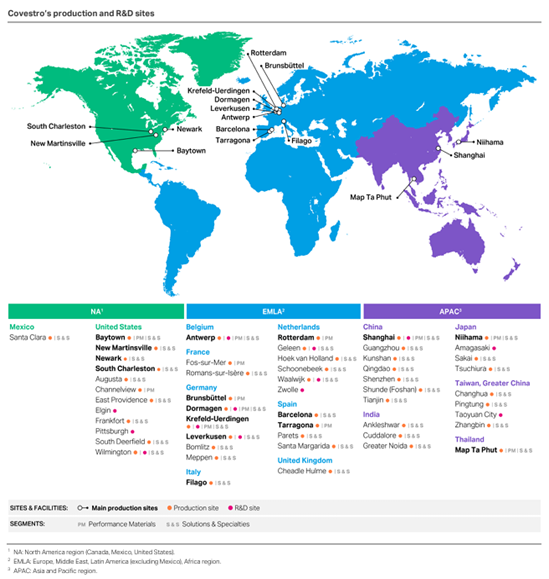

Exhibit 6: We highlight Covestro production & R&D site locations.

Source: Covestro – 2023 Annual Report, September 2024

- European companies cut jobs as economy sputters

- VW’s job cuts highlight challenges facing Europe’s auto industry

Exhibit 7: Business Climate in the German Chemical Industry Improves | Facts | ifo Institute

Source: ifo Institute, September 2024

Otherwise, Last Week – Diverging Polymer Markets – But Risk Everywhere

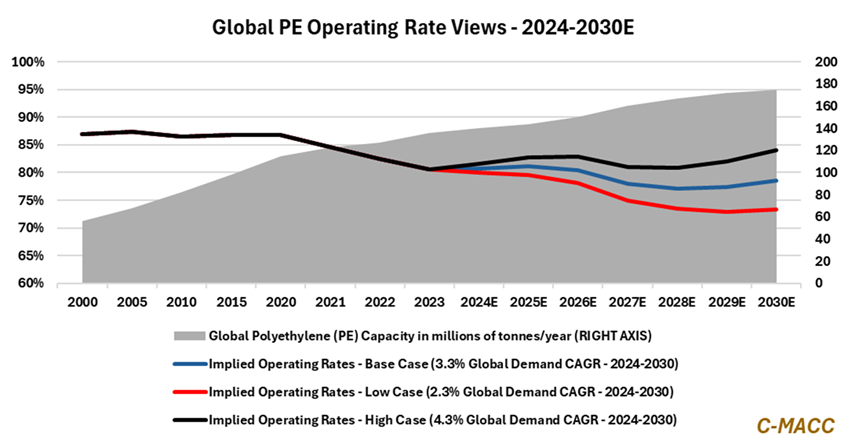

Fear of oversupply may be driving lots of behavior in polyethylene. While we are sitting on a huge production surplus in the US for polyethylene, all of which is easily making its way into export markets, outside the US, the oversupply of polyolefins is rising. New capacity keeps hitting a market that is not growing at rates seen in the past and at rates well short of what is needed to absorb the capacity. While North America is insulated for polymers because of its lower costs and because the logistics in the US – mostly rail car – make it expensive for importers, the sheer volumes of US exports mean that international competition is a critical influence on export pricing and profitability, and as US export netbacks shrink, all producers must question whether they could make more money by trying to gain domestic market share. The reality is that while oil prices are high, the difference between export netbacks and “net” domestic prices – i.e. what we show below versus what the pricing services are showing – is not that large. All are discouraged from upsetting the domestic status quo for what may be very little, or possibly negative net income outcomes. However, as crude oil prices weaken, the negative pressure on international polymer prices increases, and the gap between the export netback and the domestic netback increases, especially for polyethylene and polypropylene. Polypropylene is much more vulnerable to opportunistic imports into the US than polyethylene. While we saw a hurricane moving through Louisiana last week and watch others possibly forming in September, once the storm season is over, we are quite bearish on US supply/demand for polyolefins and expect a weaker 4Q. As noted in the chart below – global operating rates look very poor and they do not look like they will improve any time soon.

Exhibit 8: Global virgin polyethylene (PE) operating rates will struggle to reach 80% by 2030, much less the 2000-2015 average of between 85-90%, without substantial help from restructuring actions/closures to cut supply, per our view.

Source: Bloomberg, C-MACC Analysis, September 2024

Exhibit 9: We highlight the Dow global PE outlook from earlier this year which estimated a total PE demand growth CAGR of 4% between 2023 and 2030, slowing to 3% between 2030 and 2050.

Source: Dow, September 2024

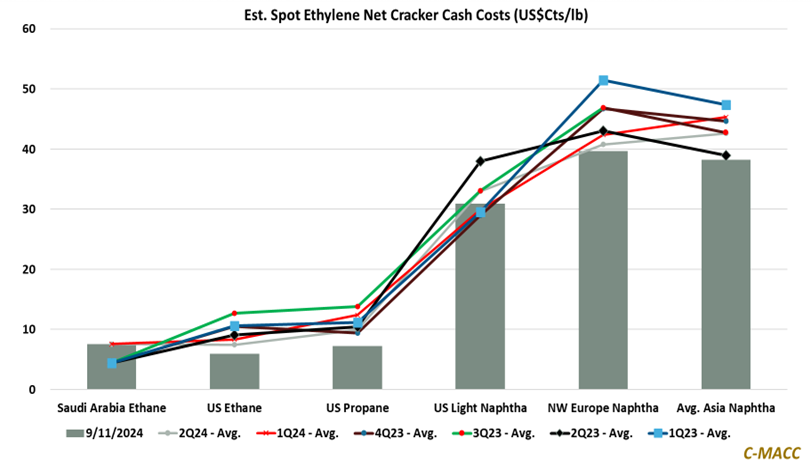

Even as oil weakens – the US edge remains strong. The chart below shows the continued major cost advantage in the US versus the rest of the world for ethylene, based on the abundance of ethane and, more recently propane. The propane market has some seasonality to it, because of heating demand in the winter, but the NGL surplus in the US is growing, and we see no end to this as new natural gas demand emerges to feed new LNG capacity. While the surpluses will likely remain, and we have written extensively about the likely consequences, the risk to US producers of ethylene is that natural gas prices rise to encourage more production to feed the LNG facilities and that ethane and propane prices track natural gas, although perhaps with larger discounts to fuel values. If we continue to see weakness in oil prices through the balance of this year, we will see the curve flatten. While it may impact international polymer prices and lower export netbacks for the US – as noted above – it is unlikely that prices would fall far enough that the US NGL and chemical/polymer export arbitrages would disappear.

Exhibit 10: The US and Middle East’s cost advantage is sizable relative to Europe and most of Asia.

Source: Bloomberg, C-MACC Analysis, September 2024

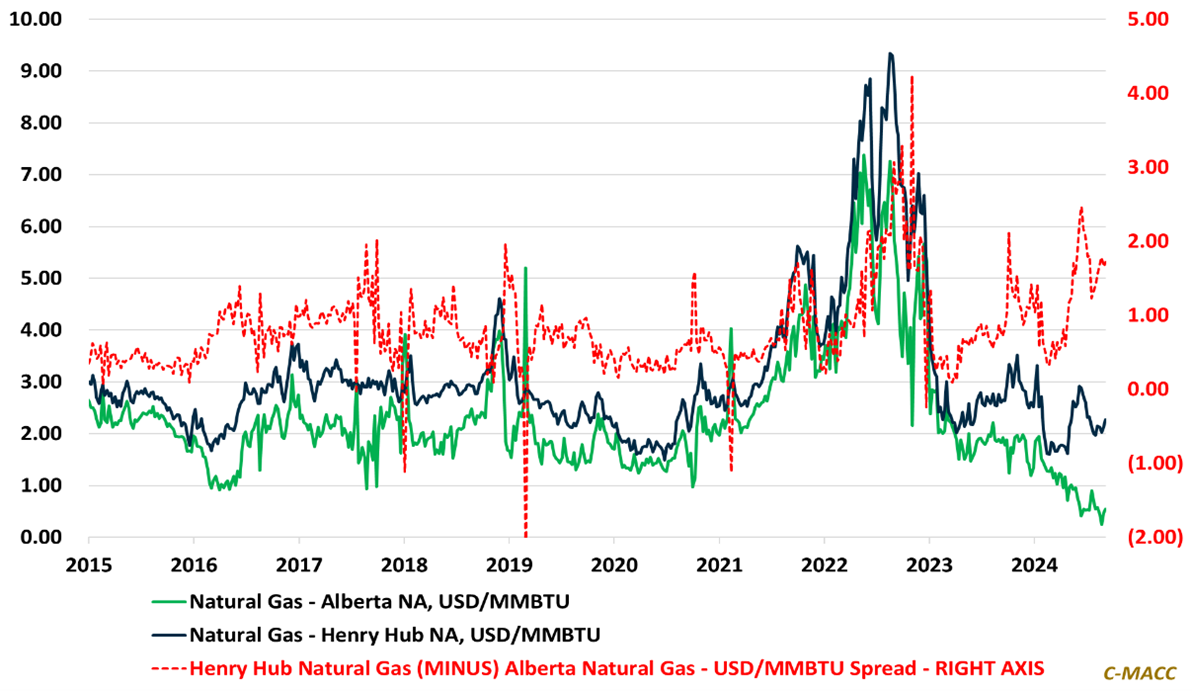

Canada gas – a gift that will keep giving or one that will end: In Exhibit 11, we show a growing natural gas advantage in Canada, but it is just as interesting to look at the absolute levels of natural gas prices in Canada, which have collapsed. Local production is likely rising in anticipation of the Shell Canada LNG start-up, but for now, the competitive edge this gives to Alberta based companies is significant. Note that this edge comes when US natural gas is also very cheap, and Canada prices look almost free compared to Europe and Asia. Dow talks about the strength of margins in its North American polyethylene business in the release today. The capacity in Canada is looking significantly better than the capacity in the US today, which is still very good. Based on today’s numbers, Dow’s new project in Canada will be a home run, as the blue hydrogen coming from the natural gas will be very low costs and Dow may well be able to produce low carbon polyethylene in Canada for less than regular polyethylene in the US, and much less than anywhere else in the world. But is the gas advantage sustainable? Canada has LNG ambitions beyond the Shell Canada project and low natural gas prices will only serve as an added incentive to build more. Step changes in demand due to new very large LNG projects could change the gas dynamic in Canada and take away this advantage and it will be interesting to see what happens when Shell Canada starts up.

Exhibit 11: Alberta natural gas reflects a discount to Henry Hub, which has risen YTD and is at the high end of the 2015-2021 range. Cheap Alberta natural gas prices support regional chemical growth projects, such as at Dow.

Source: Bloomberg, C-MACC Analysis, September 2024

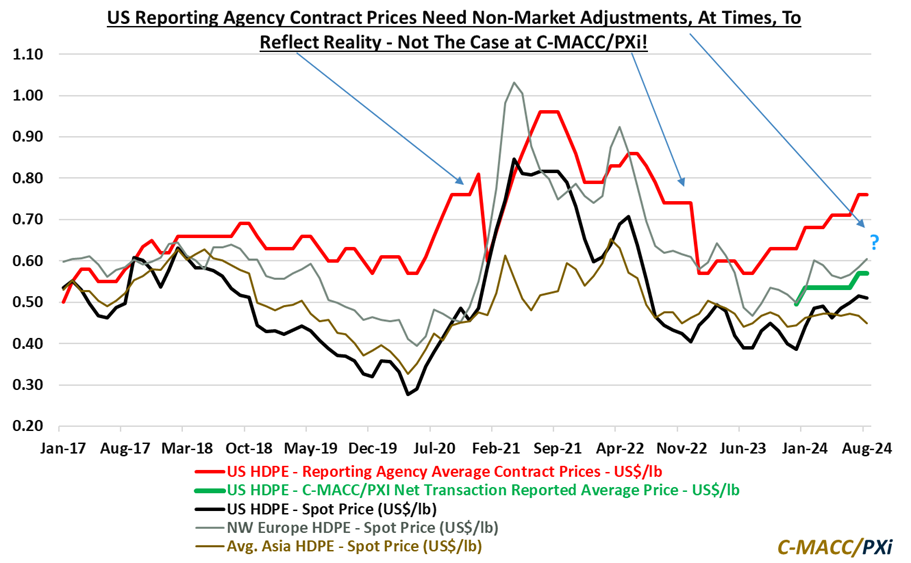

The lack of market transparency – good or bad for US polyethylene? In our journey to develop the C-MACC/PXi polymer price expectations service, one of the more obvious standouts to us is the severe lack of transaction transparency in US polyethylene and the surprising fact that many on both sides of the table are happy with that. We see a market where price reporters should more accurately be called price setters, and this drives a very different relationship between the price reporters and those buying and selling the polymer, with an emphasis on influencing what is reported rather than reporting transactions that have been settled. This makes polyethylene very different in the US than in other markets and very different from reporting for other chemical and polymer pricing in the US. We have a partisan market – companies supporting reporters’ views that they believe better represent the buyers and others supporting the views that better represent the sellers. The reason why this has been allowed to develop is that some buyers believe that they can negotiate large discounts off higher reported prices, while using those reported prices to drive their own sales prices, while at the same time, the producers generally do not provide color or price confirmation to the reporting services, they just publish price increase announcement. Those reporting the increases without factoring in any of the discounts that might accompany some of the increases report prices that drift away from the “real” market over time, leading to periodic “non-market” price adjustments. We understand that one of the new entrants has suggested that they make a non-market adjustment each year in the same month, effectively accepting that they expect their price reporting to drift away from the real market over a year – how is this helpful?

- US-China relations may have a big impact on polyethylene

Exhibit 12: We highlight our net transaction price methodology from our polymer pricing service relative to the major reporting agency reference price average, and this Exhibit factors in an unchanged MoM level in August.

Source: Bloomberg, C-MACC Analysis, September 2024

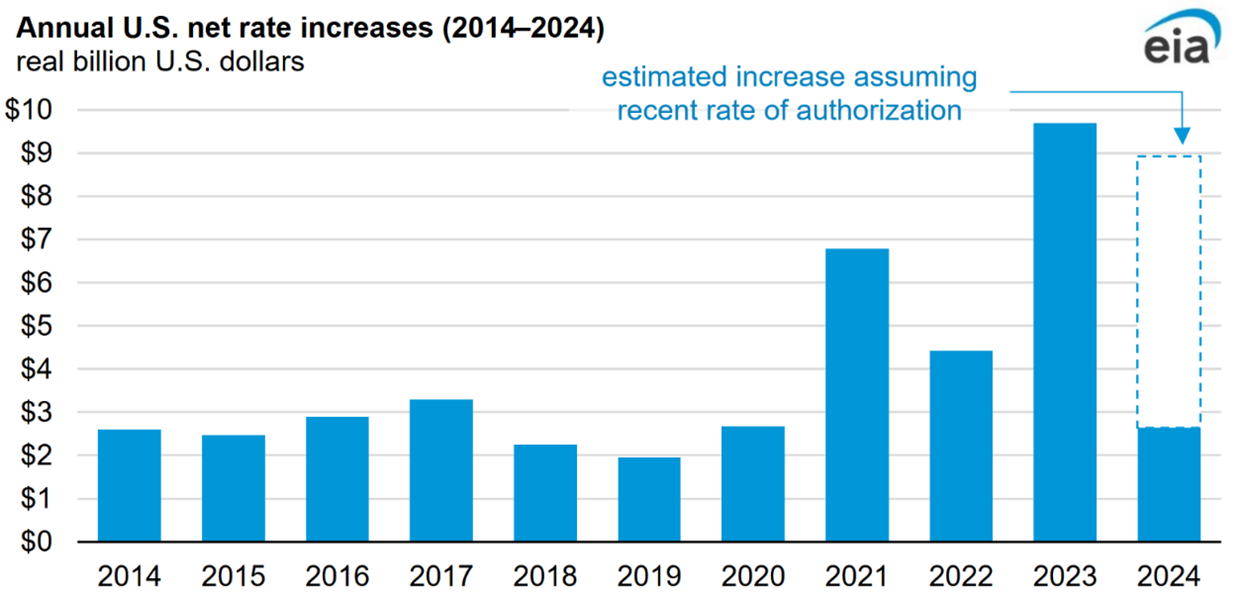

Supply/Demand works in power as well – especially in regulated states: US regulated utilities are allowed to make a reasonable return on investment and can price new capital projects into rate bases and directly onto consumers. Years of power efficiency gains and lower cost technologies have allowed power prices to decline in most US states, more aggressively in unregulated states. In the unregulated states, there is no guarantee of a return on capital, and consequently, you see more IPPs emerging, while the majors cut back on capex in exchange for higher dividends – one of the criticisms that has been thrown at CenterPoint for the poor infrastructure in Houston after hurricane Beryl. Recently, power demand growth, coupled with investment inflation, has driven spending higher than expected for many utilities, a trend that should continue for years. This is leading to higher rather than lower power prices, as shown in the chart below, and this is not a trend we expect to reverse quickly. This is part of the challenge facing data center development and many energy transition initiatives as these need not only more power, but lower cost and clean power. The trends are moving the wrong way.

- Appalachian Power lowers rate hike request as customers criticize increases

- Reregulation? How utilities and states are responding to PJM’s record capacity prices

- TVA Raises Rates without Public Scrutiny to continue Fossil Fuel Bonanza – SACE

- US electric utilities push for more rate hikes after record year of increases

Exhibit 13: Trend toward electric utility rate increases in regulated markets continues in 2024

Source: EIA – Today In Energy, September 2024

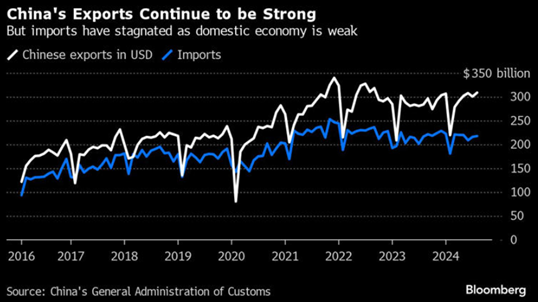

Why a trade war with China could be disastrous: If we look at the Chinese trade data it is very evident how important the export market is to the domestic economy, and while some of the lower import blame in the headline below is placed on lower domestic demand growth, some is also greater self-sufficiency as local capacity increases – China no longer has to look outside China for luxury or any other autos, for example. The Chinese economy is not robust, a lot of which is due to much slower than expected domestic demand growth, and many factories are running well below capacity, despite the rise in exports. The chart below understates the volume of exports, as there has been price deflation for the last three years and consequently the growth rate in exports in terms of units sold is higher. While China has been growing the volumes of exports to places other than the US and Europe, any major import restrictions from either country would present problems – Chinese export-driven revenues would fall and factory output in China would drop even lower. This would inevitably have a further destabilizing impact on the government, which is in no-one’s interest. See – Global Trade – The Greatest Risk for the Next Two Years?

Exhibit 14: China’s Exports Jump to Two-Year High, Imports Remain Under Pressure

Source: Bloomberg, China’s General Administration of Customs, September 2024

- China’s exports top forecasts, but imports disappoint amid depressed domestic demand

- Wholesale Used-Vehicle Prices Increased in August

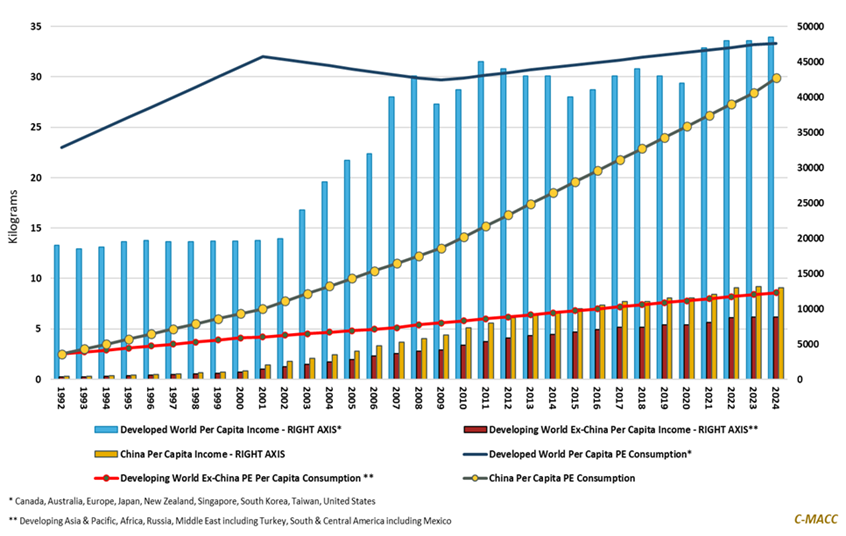

Plastic trade – more than just polymers: The consumption per capital chart for Chinese polyethylene does not suggest that the average Chinese citizen is using polyethylene at a rate greater than he or she can afford. It is a reflection of the volume of polyethylene that is produced in China and imported which is subsequently exported and finished consumable goods – like plastic bags – or durables, or as packaging for anything exported. As such, the health of the Chinese export market is at the heart of the future for polyethylene and while global producers are concerned about the level of polymer construction in China and its likely impact on global markets, any trade slowdown with China could have more severe repercussions. You could argue that buying less from China means buying more from elsewhere, and this might not impact overall polymer demand, just move the demand around, but forcing more Chinese polyethylene into export markets because of lower domestic demand would not be good.

Exhibit 15: Can we count on China for similar polyethylene (PE) demand growth going forward?

Source: World Bank, OECD, ICIS, Bloomberg, C-MACC Analysis, September 2024

Hydrogen Economy – Desperate Times – Plug Power Throws a Series of “Hail Maries”

- Plug Power issues equity quarterly to meet its cash burn, and as the stock falls, dilution worsens. Eventually, the option of issuing equity could disappear – absent a rapid turnaround in revenue/earnings, Plug is in trouble.

- As traditional capital markets for Plug close, borrowing further against fixed asset values might be another option. Danimer Scientific has gone down this path but is now out of options and in more trouble than Plug.

- Plug’s conditional DOE loan is unlikely to help the company, as it is intended for the construction of hydrogen projects and cannot be used for general expense coverage. Plug has limited options and may need a bail-out.

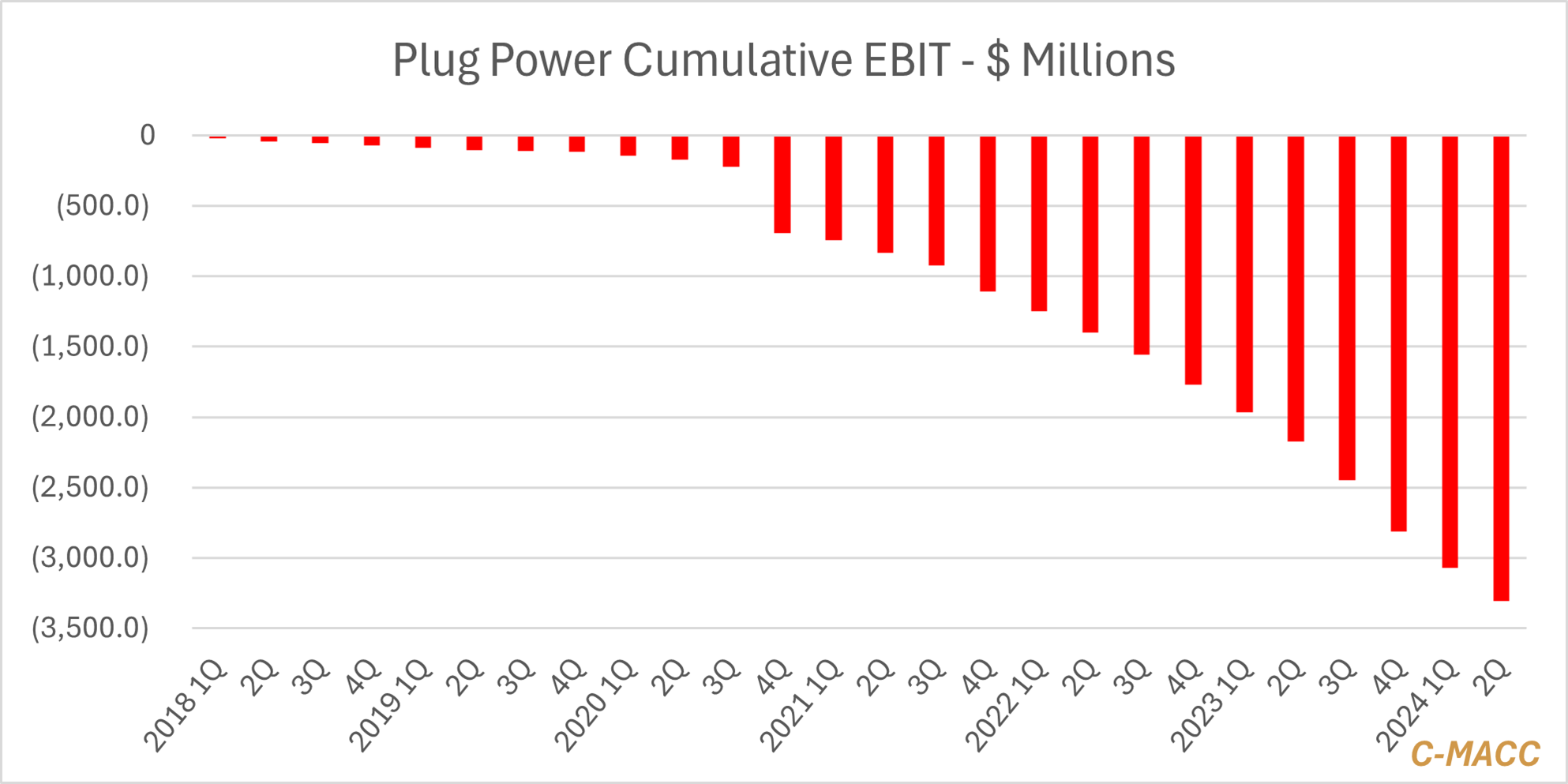

Plug Power has little choice but to look between the cracks in the pavement for any cash it can find to stay operational, but it may all still be for nothing. The company has spent the last three quarters diluting shareholders meaningfully as it issued stock through both an ATM (starting in 1Q) and a secondary offering in July, with the cash raised being used to offset the cash burn in the business, not for additional investment, so the company is selling shares to stay solvent. The opportunity to rethink the business, rebase costs, and think about the austerity that is now needed was more than a year ago, but at that time, Plug and many others were looking at the optimism in the hydrogen market and the indication of interest around equipment demand and decided to plow forward in the hope that it would all come together. Instead, the stock issuance has only contributed to investor fear and driven the stock lower – so much so that meeting cash flow needs in 4Q would require a lot more dilution than we have seen in the first three quarters – note in the chart below that we are basing 3Q 2024 on only the secondary offering – Plug still has the ATM in place. It could have raised more cash through this program but with more dilution. (note: an ATM is an “at the market” share sale, where a broker is authorized to sell treasury shares from the company on a daily basis, and it is limited in both how much can be done each day and how much can be done in aggregate, by an agreement filed with the SEC- Plug Power has such a high daily trading volume, that the company has been able to raise a lot of cash this way).

Exhibit 16: Plug Power is pouring out money – is it going down a drain?

Source: Capital IQ and C-MACC Analysis

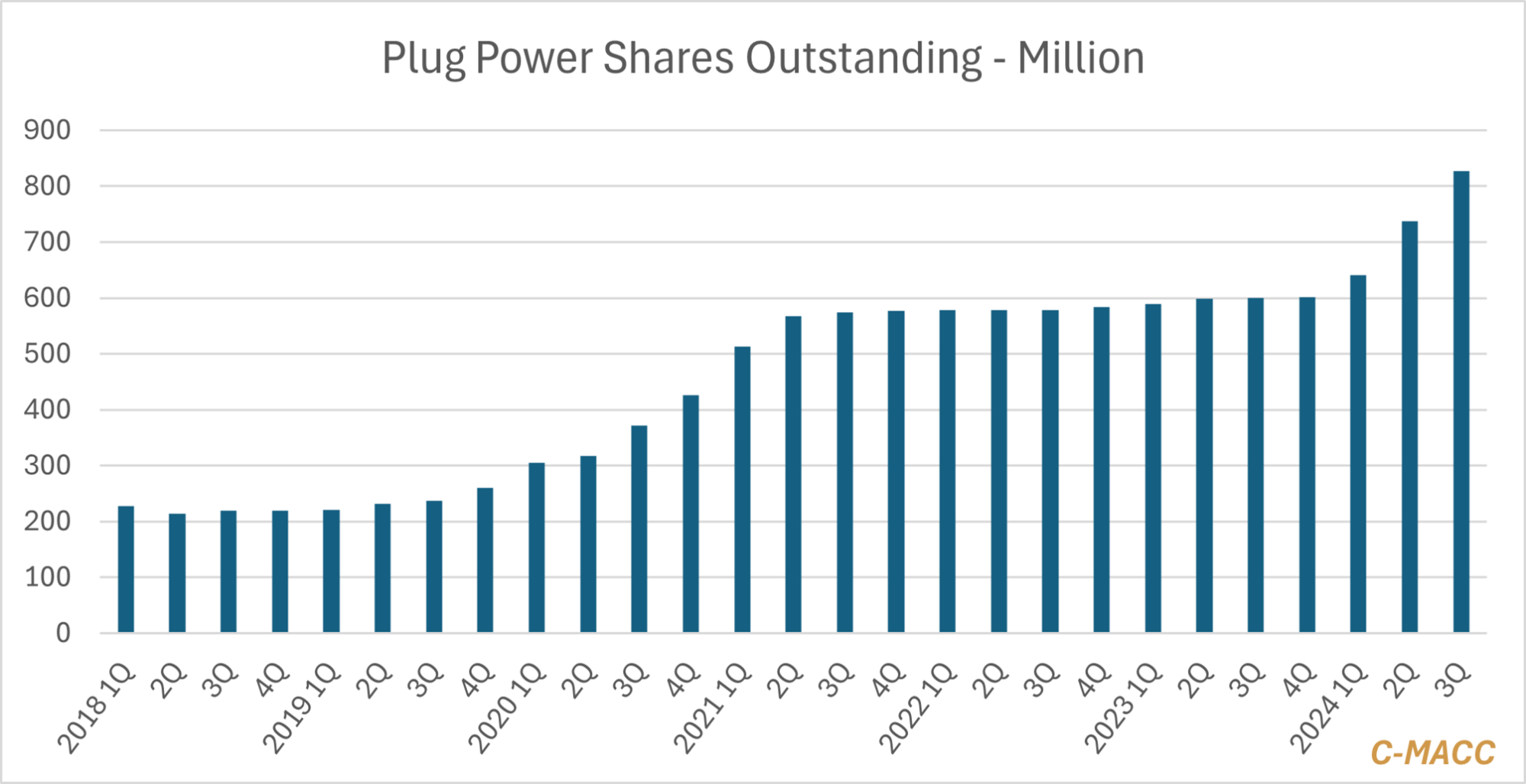

Exhibit 17: Shareholders have been diluted this year by more than 35% while all the cash raised is gone.

Source: Capital IQ and C-MACC Analysis

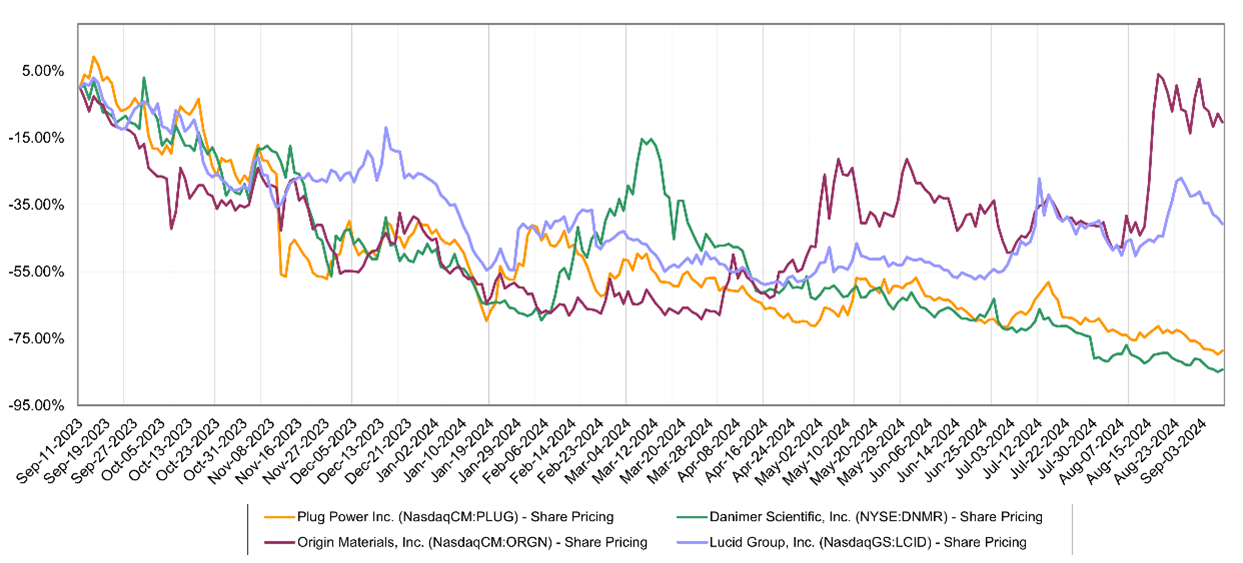

At the current share price, Plug would need to sell close to 145 million shares to raise $250 million, which may be what is needed to get from here to the end of the year without running out of money. But another equity raise of that nature will likely drive the share price even lower, assuming there are buyers – the secondary in July may have been seen as less destructive than trying to raise the same amount of money daily through the ATM. The constant selling pressure caused by an ATM, especially when there is no other positive company news, can drive the share price down incrementally each day. In the share price chart below, we show a few companies that are struggling with cash flows and running short of options to raise more money. However, some have found self-help and others have investors who are keeping the faith. The rebound in Origin Materials stock, while not that significant, reflects a change in corporate strategy to exploit a possible shorter-term opportunity, away from the original plan, but targeting a fast path to cash flow positive (note that C-MACC owns Origin Material in its corporate brokerage account). This is a fortuitous discovery that Origin had on the back burner, but given the reality of the current financing market, Origin has been able to adapt, assuming the PET caps business takes off. Lucid still has a funder in the Saudi Arabian sovereign wealth fund but continues to bleed cash and is effectively doing the same as Plug, issuing equity to cover losses. Plug Power and Danimer Scientific are likely past the point of no return, although Plug has yet to mortgage the assets, while Danimer has now borrowed against everything.

Exhibit 18: Plug is not the only one in trouble

Source: Capital IQ and C-MACC Analysis

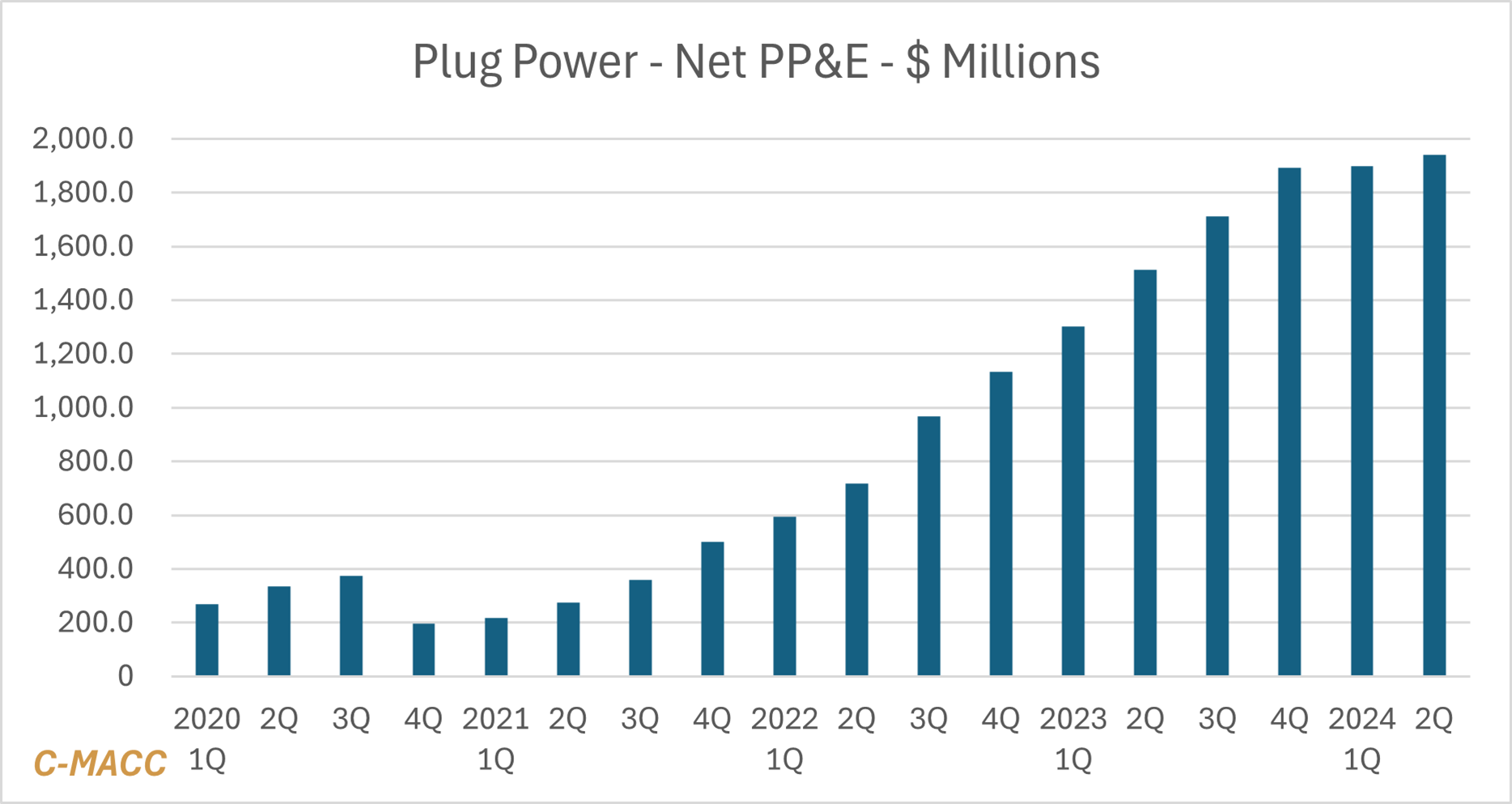

Borrowing against the assets is still an option for Plug Power, but it is a last resort. The assets to be considered would include the net plant and equipment – see the exhibit – and any IP, where the value is hard to quantify. The more PEM electrolyzer manufacturers that hit the market the lower the potential value of any IP any of them might have. Also, if the plant and equipment is manufacturing capacity that is incomplete or unproven, the perceived value will fall and the amount anyone is willing to lend against it will also fall. In the chart below, note that the net PP&E has not grown since the company started raising more equity. It would be very coincidental if the capital program ended at the same time – more likely, Plug does not have the cash.

Exhibit 19: Spending stopped as cash ran low, and the equity issuance started

Source: Capital IQ and C-MACC Analysis

So, what are Plug’s options? Severely limited in our view and unlikely to include the DOE loan suggested below. DOE loans are very specific, in this case to build hydrogen facilities that would employ plug electrolyzers – i.e. building demand to support the existing investment in electrolyzer capacity. These would be discrete projects, and the DOE would expect some level equity to support each project, and it is unlikely that Plug can come up with the equity without involving co-investors and this may be counter to the conditions of the loan. The other possibility for Plug, but perhaps not for its shareholders is that a new Democratic Administration, should it happen, deems the company “too important to fail”. This might involve some sort of bailout, but it is unlikely that any remaining equity holders would do well.

Sustainability and Energy Transition: Transition Getting More Expensive and Less Popular – By Association

Are we heading for an ESG showdown in the US? The “anti-woke” lobby in the US is making a lot of noise, enough to scare some companies into backing away from targets, especially for diversity and inclusion. There are also plenty of groups pushing back on environmental targets, and most of this is focused on the right-wing “Trumpian” view, which has more to do with pushing back on anything “liberal” versus considering ideas on their own merit. Interestingly, there is very little to suggest that a DIE program negatively impacts financial returns, which is what investors should be looking for, while some of the proposed environmental targets are very negative for financials, which is why we are seeing so many challenges with investments to drive emissions lower. The trouble with pushing back on any of these agendas is that companies get caught between activists who are pushing both sides of the argument but also customers who fall into both camps, and by bowing to the “anti-woke” activist pressure or customer groups that say they will not buy your products, you will inevitably alienate yourselves from another customer group. Should this get worse you could envisage a world where we have republican companies making products for republican buyers and democratic companies making products for democrats!! All very silly, but a major challenge for large corporations selling consumables or durables. It is very unclear how this will turn out, but on the environmental side it is another roadblock on a road that already looked too challenging.

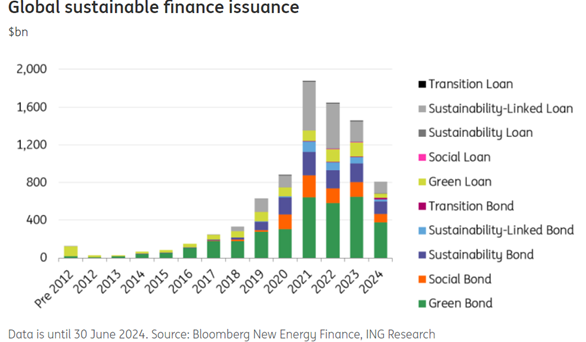

Exhibit 20: While the 2024 numbers look better, the peak came in 2021.

Source: Global sustainable finance market: changing for the better, August 2024

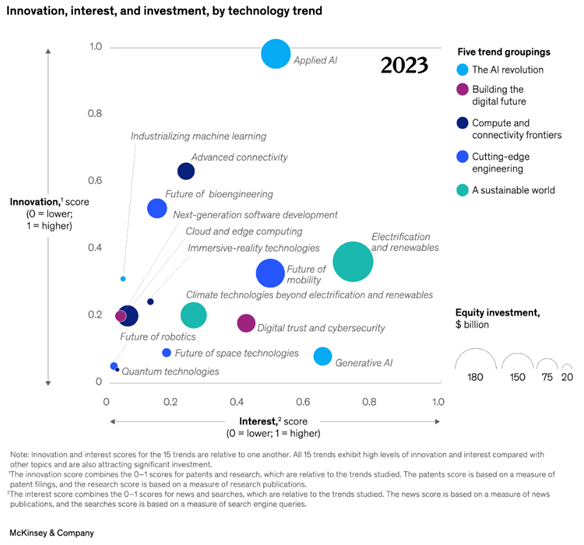

The McKinsey chart below, which looks at both interest in a topic and the level of innovation needed shows energy transition as high interest and relatively low innovation, which sounds like it should be a good thing – i.e. manageable. The challenge is the investment needed – which is very high, and the fact that in almost every case we are looking to replace something that is very cheap today. Added to this is the necessary job transitions from old energy to new energy, which causes some of the fear reactions. The sheer level of spending needed should convince most that this will be a good thing for economic growth, but the underlying fear of change overwhelms the overall opportunity for many. These are very easy emotions to play on from those who are trying to limit environmental moves and some of the broader ESG objectives. In the chart, the “interest” level measured is global – the US level would be lower.

Exhibit 21: In this chart McKinsey places environment and sustainability among other World trends.

Source: McKinsey

The shape of the US government and legal system makes it very difficult to move fast. Even if you had a congress stacked in the favor of a sitting president in the US – allowing for relatively fast policy changes, industrial and environmental progress can get hung up in the courts and with regulators, such that progress is constrained. For every well supported good idea, there is a well-funded minority who think it’s a bad idea and are willing to fight it. In Exhibit 20, some of the early funding was for easy projects, where regulations were not much of a challenge, and neither were any local objections. For energy transition to work, the bar in the chart above should be getting higher every year, but as the mix moves from lots of small projects to fewer much larger projects, the hurdles start rising.

Public Education – Is it Possible? In our sustainability report last week, we painted a relatively bleak picture of how climate change action might unfold – too little progress, much worse weather issues, and panic-based very expensive eventual action. One of the articles below suggests that public education might help as consumers could do a lot to reduce their carbon footprint if they believed in the consequences of doing so and were properly motivated. We also discussed plastic recycling last week and again below, and this is another area where there are significant misconceptions and where a better educated public could drive significant change. In both cases you struggle in many countries, but especially in the US with an overwhelming load of misinformation, some generated maliciously, and often politically motivated, and some generated by those who simply do not understand the science, the economics of what they are asking, or both. Getting a consensus view on emissions and plastic use and reuse will only come if there is evidence of significant personal risk through non-consensus behavior. The weather is not impacting enough people, nor is it conclusively linked to consumer behavior and preferences (yet) such that it would be possible to get a consensus, and the only way to get a consensus on recycling is through financial incentives – rebates if you recycle and fines if you do not. Even where they are in place today, The Netherlands and Germany, for example, we do not see thriving recycling businesses and recycling rates remain low. It is highly unlikely that we can rely on changing consumer behavior voluntarily to combat emissions. These issues are related because wider bans on the use of plastics will result in the use of alternatives for packaging that will almost certainly drive higher emissions.

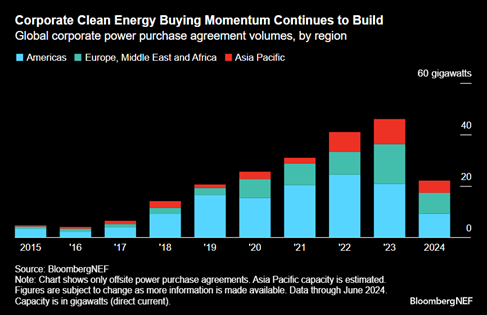

The difference between activity and targets: In the headline below the spin could be quite positive, but while we see progress at many companies – more spending on environmentally biased projects, the overall rate of aggregate spend is well below some of the very tight climate targets. Part of the challenge is broader infrastructure and power-related, as we have noted in lots of work, but only a subset of projects meets the criteria of being better from an environmental and sustainability perspective AND making sense commercially. These are the easy moves and possibly moves that companies might have made without the promise of incentives, and simply as part of a health and safety drive within their operational plans. It would be interesting to see the same survey below conducted 10 years ago, because the answers may not have been much different in terms of the percentage of companies, although the focus and accounting are more targeted today. Note the growth in PPAs in the chart below – this is good growth, but not enough to meet climate targets.

Exhibit 22: There were 211 corporate clean PPAs in 1H24: more than 22GW, up more than 30% YoY.

Source: Energypost, September 2024

The week of September 9th – click on the day or the report title for a link to the full report on our website.

Monday – Weekly Margin and Pricing Analysis

Francine Concerns Put US Polymer & Chemical Markets on Edge, As Prices Likely To Decline Absent A Disruptive Production Event!

- Polymer Market Trends: Global polymer prices, on average, reflected weakness WoW, and while fundamental trends suggest further price weakness ahead, a storm development in the USGC could favor price support.

- Chemical Market Trends: We highlight the announced Methanex acquisition of OCI Global methanol assets, US methanol prices at a premium to Asia, and flag strength WoW in US spot ethylene relative to propylene.

- Feedstock Market Trends: US natural gas and USGC ethane values rose WoW relative to Brent crude oil, Ex-US naphtha, and Ex-US natural gas prices, lessening US chemical producer cost benefits and favoring lower prices.

- Agriculture Market Trends: Ex-US ammonia prices fell relative to US levels WoW, following a run-up in global ammonia prices, and global input cost trends suggest greater production and lower global prices into yearend.

US PVC Producers Among the Most in Francine’s Path, Methanol & Ammonia Markets Could Also See Impacts

- General Thoughts: We focus on USGC storm Francine and those most notably impacted if it makes a direct hit on Louisiana, as it favors tighter US polyvinyl chloride (PVC) markets and keeping some other markets relatively tight.

- Supply Chain/Commodities: While some markets could tighten from Francine’s impact, the potential shutdown of ethylene derivative units, including PVC, could loosen USGC ethylene markets – Louisiana is net short ethylene.

- Energy/Upstream: We discuss electricity price inflation in regulated utility markets as higher growth capital costs are spurring efforts to raise prices to ensure adequate returns – this trend is unlikely to reverse anytime soon.

- Sustainability/Energy Transition: We highlight and discuss the power grid development backlogs facing many US states and Europe striving to meet demand, and flag falling lease rates for EVs as dealers seek to clear inventory.

- Downstream/Other Chemicals: The growth in Chinese exports relative to imports remains an ongoing trend, and it not only signals a weak Chinese economy but also the exporting deflation/low-cost goods to other markets.

Global PE Operating Rates Unlikely To Exceed 85% By 2030 – Substantial Restructuring Needed, Higher Oil Prices Would Help!

- General Thoughts: The global polyethylene (PE) market reflects oversupply, and this setting appears more likely to worsen between now and year-end 2030 than improve as more capacity arrives and demand growth slows.

- Supply Chain/Commodities: We discuss the C-MACC polymer pricing service and regional PE spot price trends and provide a global capacity growth view to show the significant capacity set to arrive in NE Asia later this decade.

- Energy/Upstream: The North American and Middle Eastern cost advantages in producing ethylene (& PE) are significant relative to Asia and Europe, providing a margin buffer amid weak global prices – is it as good as it gets?

- Recycled/Renewable Polymers: We provide thoughts on mechanically recycled content growth, the content mix (virgin vs. recycled) debate surrounding compounded solutions, and high chemical recycling carbon footprints.

- Downstream/Other Chemicals: We discuss PE demand per capita in China climbing to reach levels near those in developed economies in 2024 while per capita income in China remains much closer to developing world levels.

O Canada! Cheap Alberta Natural Gas Benefits Its Chemical Producers, Supports Dow’s Regional Growth Ambitions

- General Thoughts: Alberta natural gas prices have fallen substantially relative to US Henry Hub levels YTD, adding to the Canadian cost advantage in an already advantaged North American market relative to Asia and Europe.

- Supply Chain/Commodities: We discuss the Dow 3Q business update that comments on production issues, weak European margins, cost benefits surrounding its Canadian projects, and Adnoc’s downstream ambitions.

- Energy/Upstream: We highlight negative natural gas prices in the Permian in light of upcoming pipeline capacity expansions to bring it to global consumers and compare natural gas prices across major North American markets.

- Sustainability/Energy Transition: The cost of electrolyzer systems is falling, but the cost differences between the West and China remain significant. We also highlight the strength YoY in 1H24 corporate clean energy PPAs.

- Downstream/Other Chemicals: We highlight the global trend underway to cut interest rates amid generally weak conditions, especially in Europe, and flag slightly higher wholesale prices in the US in August than expected.

September In The Rain: Hurricane Francine Fizzles, Ammonia Still Thrives, & Propane Takes A Dive

- General Thoughts: Our observations and discussions suggest Hurricane Francine was not as disruptive as many feared, and our view of most commodity chemical prices is for them to face downward pressure into year-end.

- Supply Chain/Commodities: We discuss the US ammonia market as producer margins remain elevated. We also flag an ammonia project gaining approval in Illinois to serve farmers, possibly pushing more US supply offshore.

- Energy/Upstream: We highlight the ~20% drop in USGC propane prices relative to roughly a month ago, which has moved in the opposite direction of USGC ethane and could spur more near-term US propylene production.

- Sustainability/Energy Transition: We discuss the sustainability-linked bond (SLB) market, highlighting our latest sustainability research report published earlier today and comment on several other relevant industry trends.

- Downstream/Other Chemicals: We discuss the latest USDA report that frames the potential for US soybean and corn yields to set a record this year, though our medium-term view of crop market tightness remains unchanged.

Weekly Climate, Recycling, Renewables Energy Transition and ESG Report (CRETER) No 197

Transition Getting More Expensive and Less Popular – By Association

- 1st Topic of the Week: It is quite easy to play the “anti-woke” card to an audience resistant to and fearful of change, which is a tactic used in the US today. Energy transition spending should drive considerable growth and create millions of jobs, but it is easier to point to the negatives – this will slow progress if the movement continues in the US, but it will also limit spending and may contribute to an economic slowdown.

- 2nd Topic of the Week: Does anyone care if China is green – except China?

- Otherwise: We look at the costs and carbon footprint challenges of chemical recycling, the blue benefit in Alberta, and why lithium’s woes are batteries benefit.

Weekly Hydrogen Economy Update No 63

Pulling the Plug – Dilution Could Make the Spiral Down the Drain Faster

- Plug Power issues equity quarterly to meet its cash burn, and as the stock falls, dilution worsens. Eventually, the option of issuing equity could disappear – absent a rapid turnaround in revenue/earnings, Plug is in trouble.

- As traditional capital markets for Plug close, borrowing further against fixed asset values might be another option. Danimer Scientific has gone down this path but is now out of options and in more trouble than Plug.

- Plug’s conditional DOE loan is unlikely to help the company, as it is intended for the construction of hydrogen projects and cannot be used for general expense coverage. Plug has limited options and may need a bail-out.

- Otherwise, we have only two new projects to discuss this week, both in the EU and both requiring lots of public funding. We examine the still weak crop markets but relatively robust ammonia and discuss Texas power.

Loading…

Loading…

[?restrict]