Daily Chemical Reaction

Sittin’ Sidewayz (& That’s Not a Good Thing) – China Prices Still Undercut the West, Currency Devaluation Risks Emerge

Key Findings

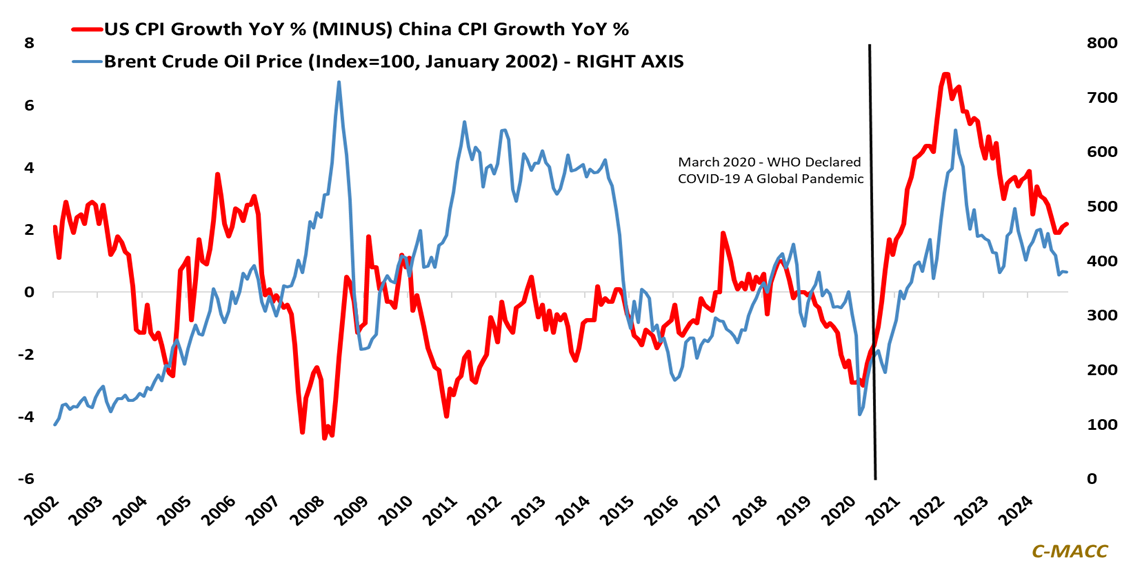

- General Thoughts: Western consumer price inflation has moderated in 2024 but remains high relative to China – North American chemical producer cost advantages provide an offset; most of Asia and Europe lack this benefit.

- Supply Chain/Commodities: The backward integration of auto- and battery-makers into critical mineral markets keeps many high-cost producers operational despite low prices pinching global profits. Lithium is a prime example.

- Energy/Upstream: We flag an announced crude oil supply deal between Reliance and Rosneft, the crude oil flows from Russia to India, China, and Turkey YTD, and why this trend is unfavorable for tighter petrochemical markets.

- Sustainability/Energy Transition: We discuss the multi-year decline of lithium-ion battery pack prices, with some estimating a ~20% YoY drop in 2024, continuing to challenge the build-out of battery supply chains in the West.

- Downstream/Other Chemicals: China’s potential to devalue its currency to offset Western tariffs is high, despite the Yuan already being at multi-year lows relative to the USD, and we discuss global real estate market trends.

Exhibit 1: China’s CPI growth remains significantly below US levels – a negative trend for US industry, in our view.

Source: Bloomberg, C-MACC Analysis, December 2024

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!