Base Chemical Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: We discuss Chinese polyolefin capacity additions and the potential for Western turnarounds to spur new capacity and keep high-cost units online in 1H25 that may create a harsh 2H25 global profit setting.

- Polyethylene (PE): US spot PE prices were weak in late 2024 but are currently priced below spot levels in Europe and Asia, and its production costs are advantaged and poised to remain that way in 2025. Europe is most at risk.

- Polypropylene (PP): US spot PP prices were weak in 4Q24 but are currently priced at a premium to spot levels in Europe, with both markets priced above Asia. Non-integrated US PP producer margin risk is high in 2025.

- Polyvinyl Chloride (PVC): We discuss weakness in China spot PVC, support in US spot PVC, and the generally weak near-term global PVC market setting – we prefer those with low-cost integrated production positions.

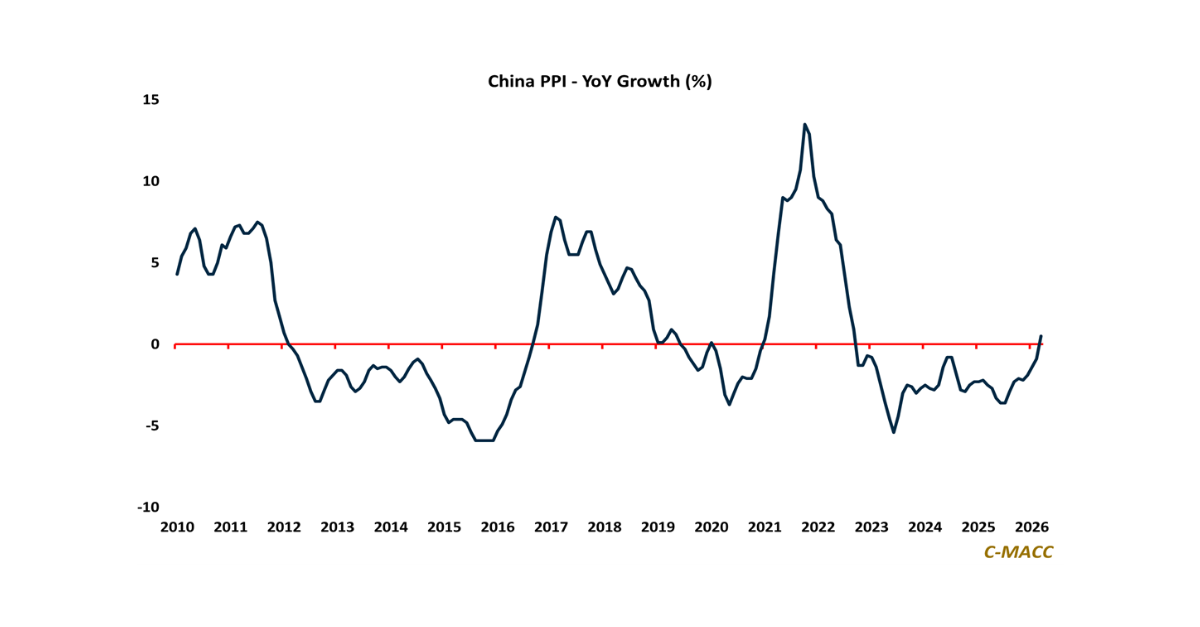

- Other Sector Developments: We discuss the futures market for Brent crude oil and US natural gas that paints a bearish feedstock-level view for chemicals in 2025, but it is not bad enough to force needed global capacity cuts.

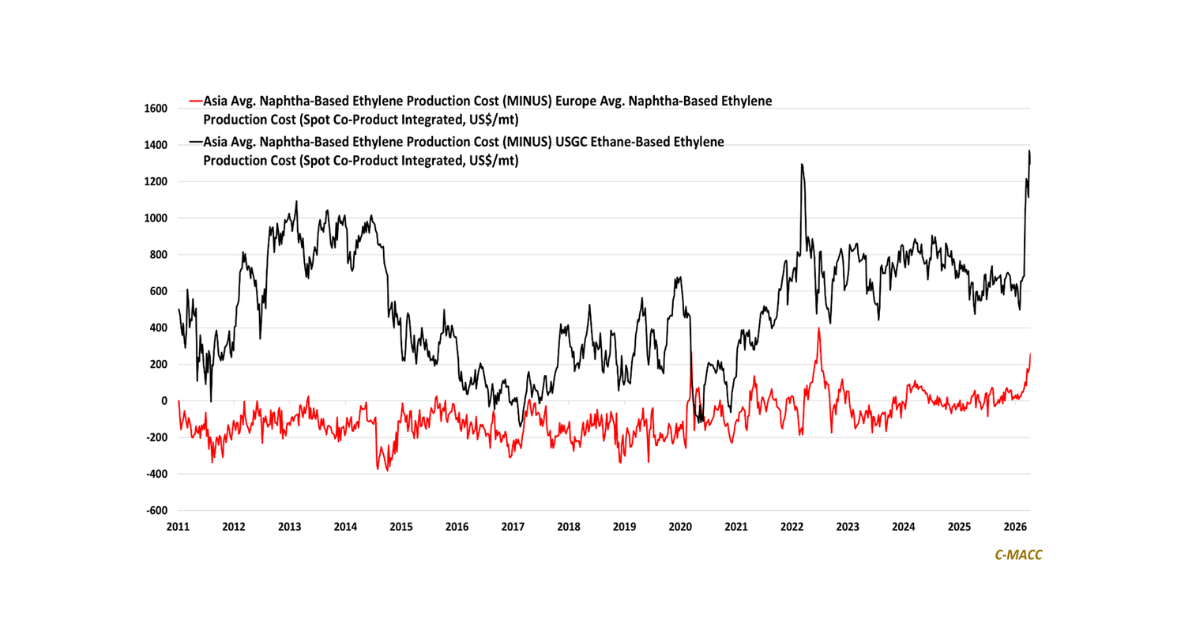

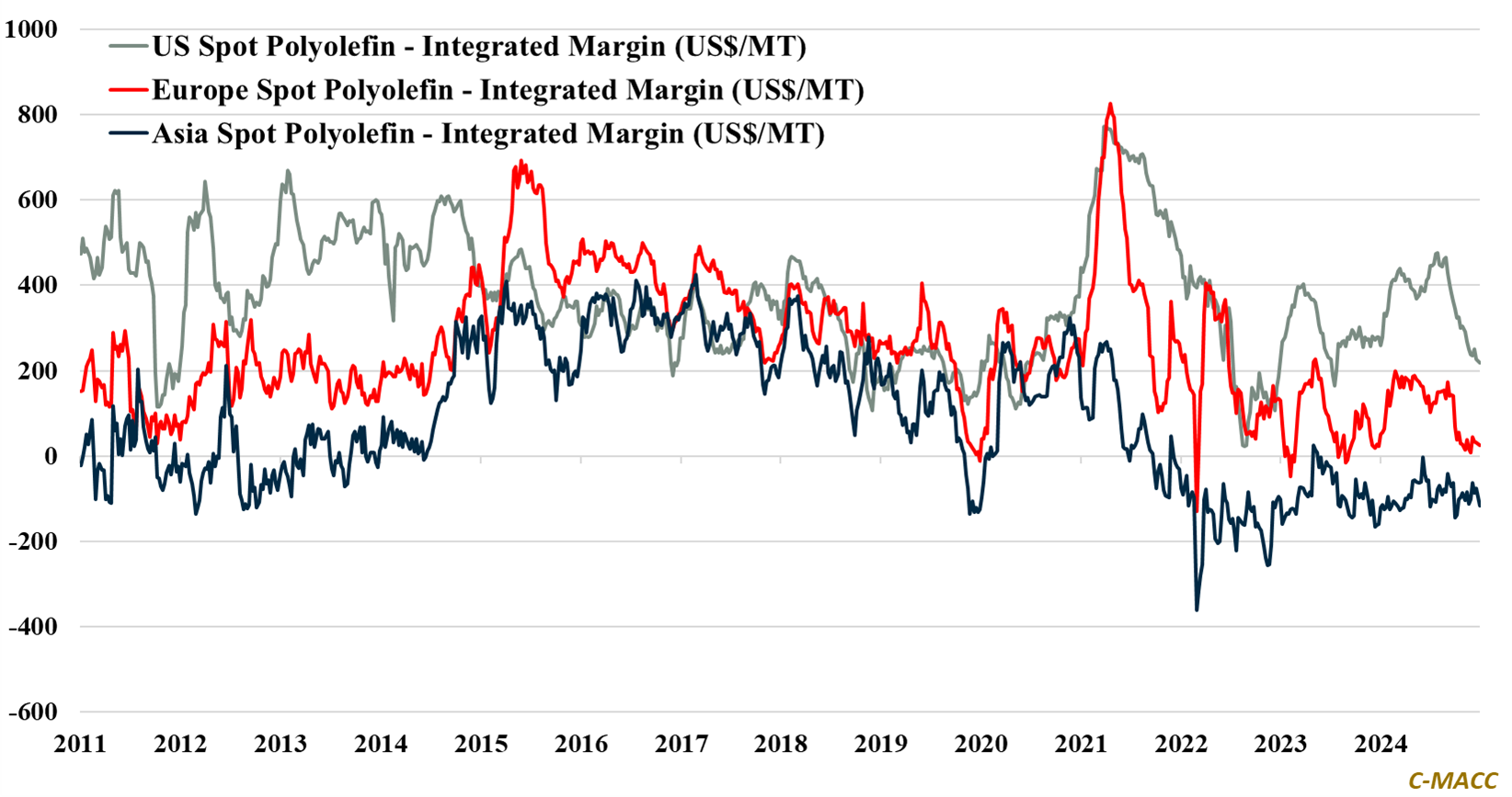

Exhibit 1 – Chart of the Day: Western average polyolefin margins fell from their 2H24 highs relative to Asia in 4Q24.

Source: Bloomberg, C-MACC Analysis, January 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!