Base Chemical Global Analysis

Global Weekly Catalyst No. 264

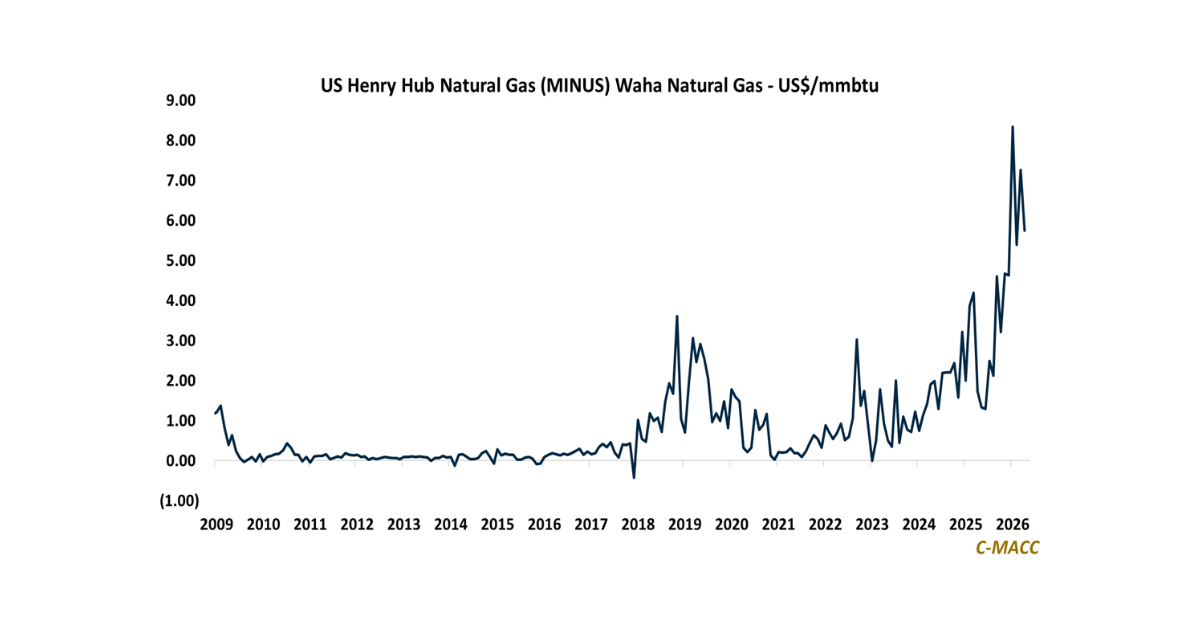

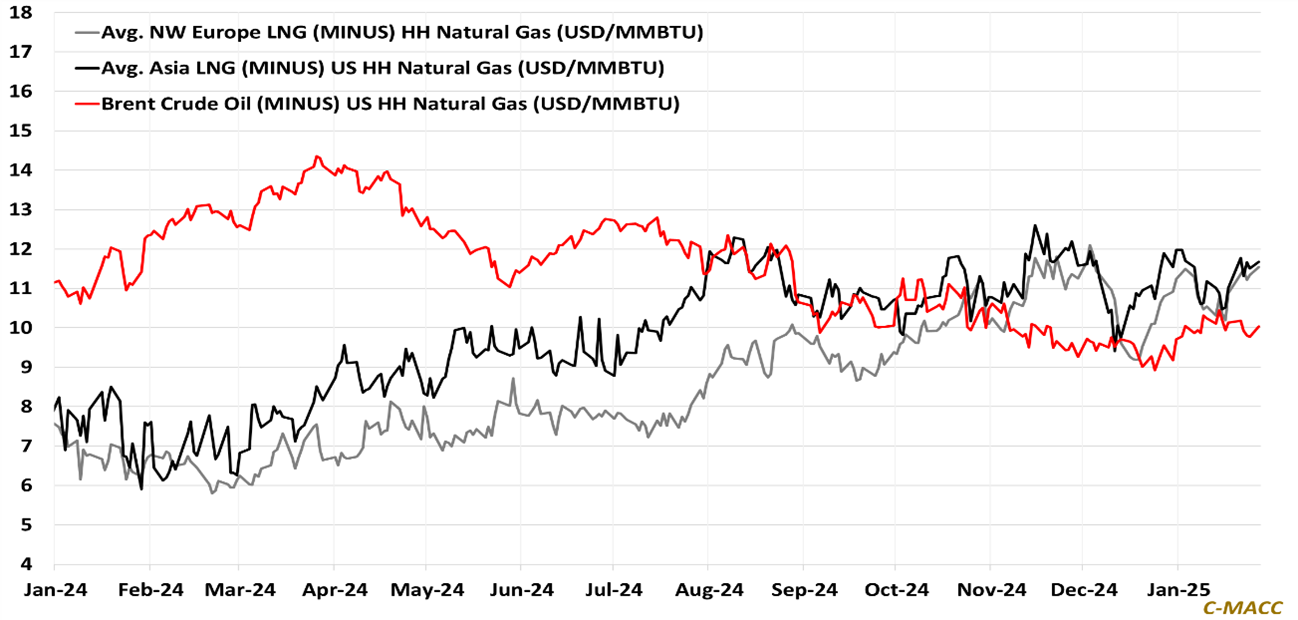

- General Thoughts: The global petrochemical feedstock setting in 1Q25 differs from 1Q24, as Brent crude oil prices are lower, but Ex-US natural gas prices are higher than US natural gas – we frame the global setting.

- Feedstocks & Energy: Global chemical feedstock movements were mixed WoW, with crude oil prices trending lower. Still, global natural gas prices are holding up, though US NGL values, mostly notably propane, fell WoW.

- Olefins: US spot ethylene and propylene prices rose WoW, but the recent positive momentum looks to be subsiding, and we discuss this spot price strength relative to 30 days ago, also considering Europe and Asia.

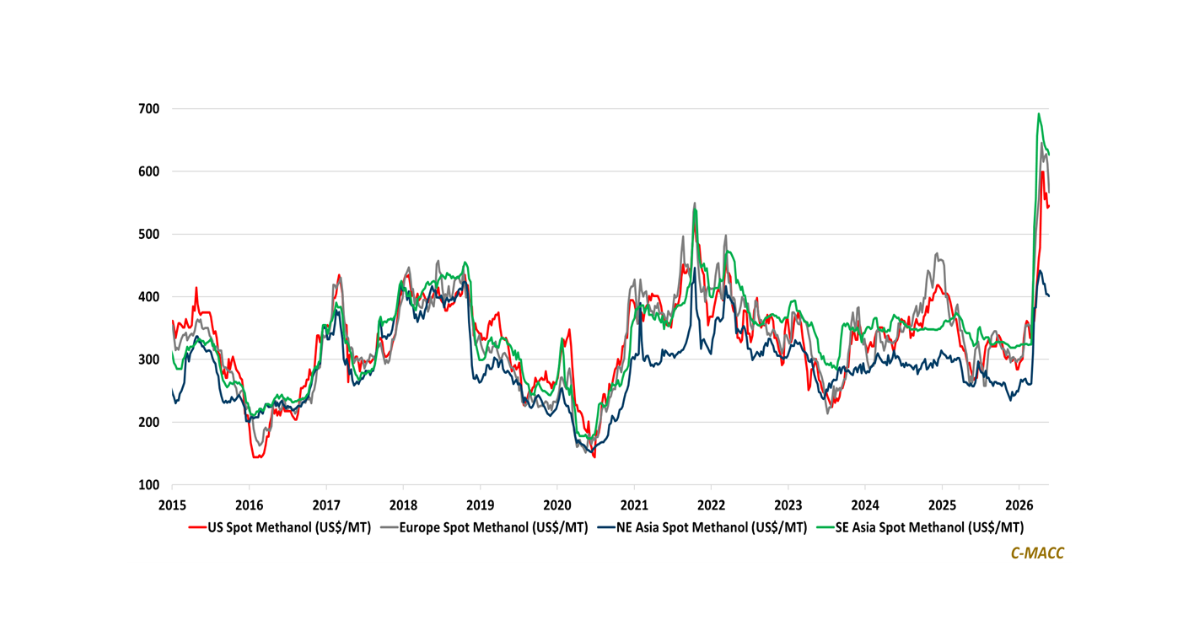

- Other Base Chemicals: Western methanol prices reflect little change WoW, holding still substantial premiums relative to Asia – we expect Western methanol values to trend lower, but not aggressively, toward Asia in 1Q25.

- Agriculture: Global ammonia spot prices weakened WoW despite global natural gas price support and corn price strength that favors on-farm demand support, which we think curbs downside risk amid supply growth.

- Refining & Biofuels: US crude oil refinery margins held up, but US ethanol production margins turned negative last week – we remain broadly more cautious about US ethanol margins than US crude refiner margins in 1H25.

Exhibit 1 – Chart of the Day: Ex-US natural gas has strengthened relative to US natural gas YoY; Crude oil has not.

Source: Bloomberg, C-MACC Analysis, January 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!