Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: Plastics are shifting from commodity resins to integrated solutions—packagers now prioritize cost-advantaged, customer-aligned suppliers delivering performance, flexibility, and resilience amid raw material volatility.

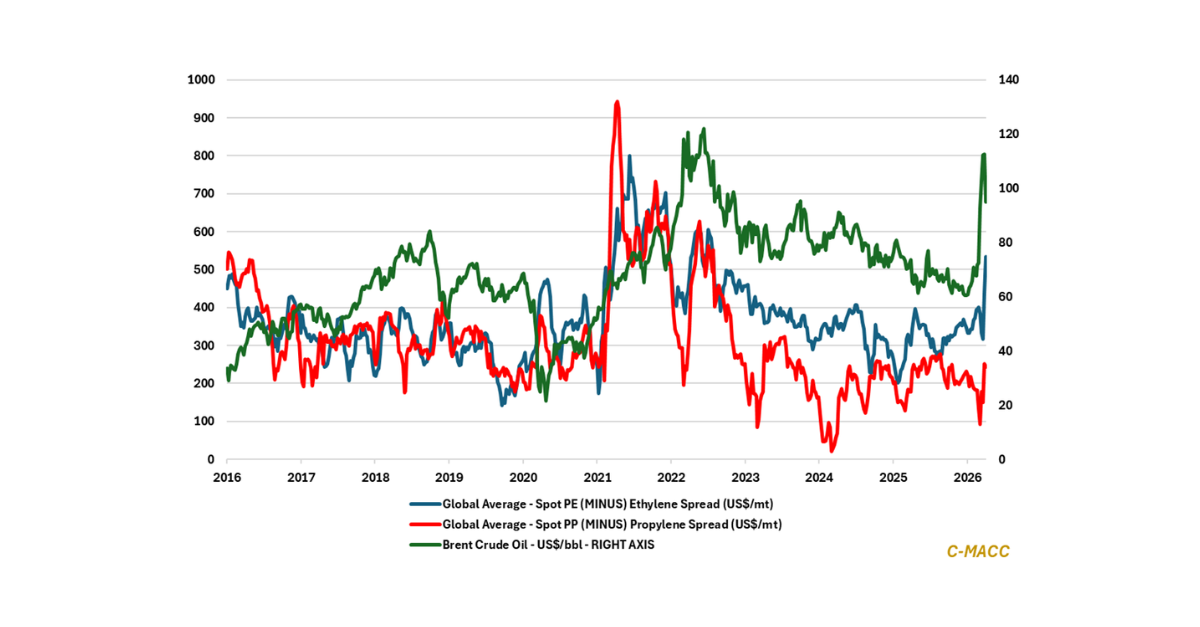

- Polyethylene (PE): In a turbulent PE market, winners combine feedstock advantage, export agility, and scale—while high-cost, inflexible players face falling margins and low market access, threatening their current survival.

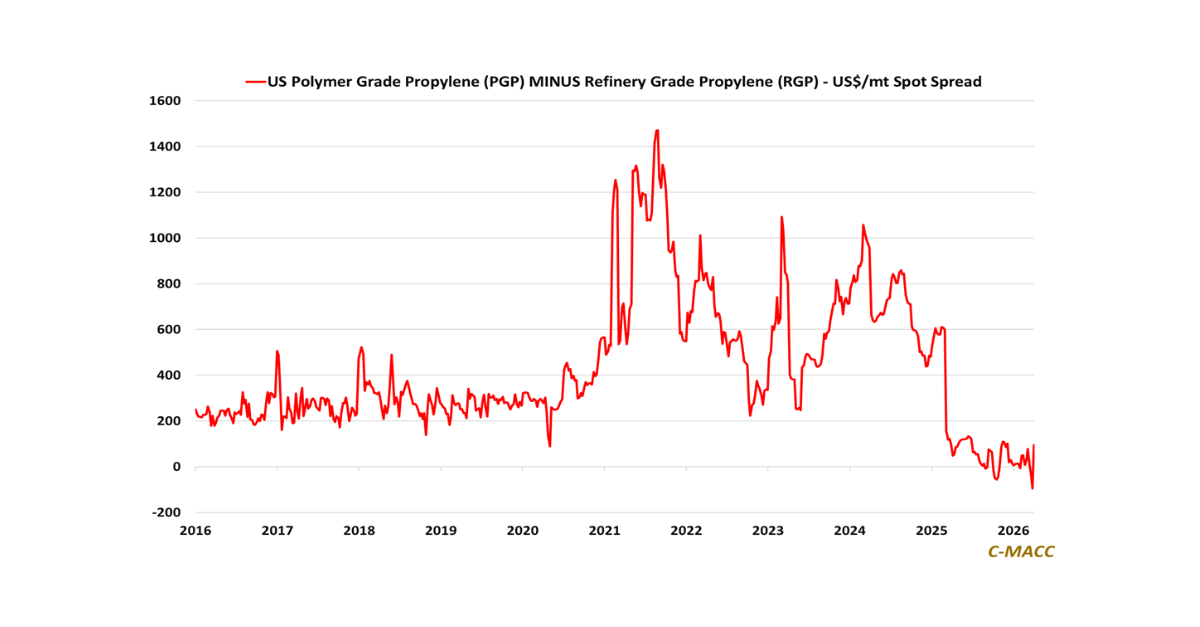

- Polypropylene (PP): Integrated producers with captive low-cost propylene are among the best positioned as PP markets face oversupply, weak demand, and rising capacity—amplifying margin risk for non-integrated players.

- Polyvinyl Chloride (PVC): As global PVC margins erode, integration, feedstock control, and downstream leverage define resilience—while trade actions, weak demand, and oversupply pressure vulnerable players to restructure.

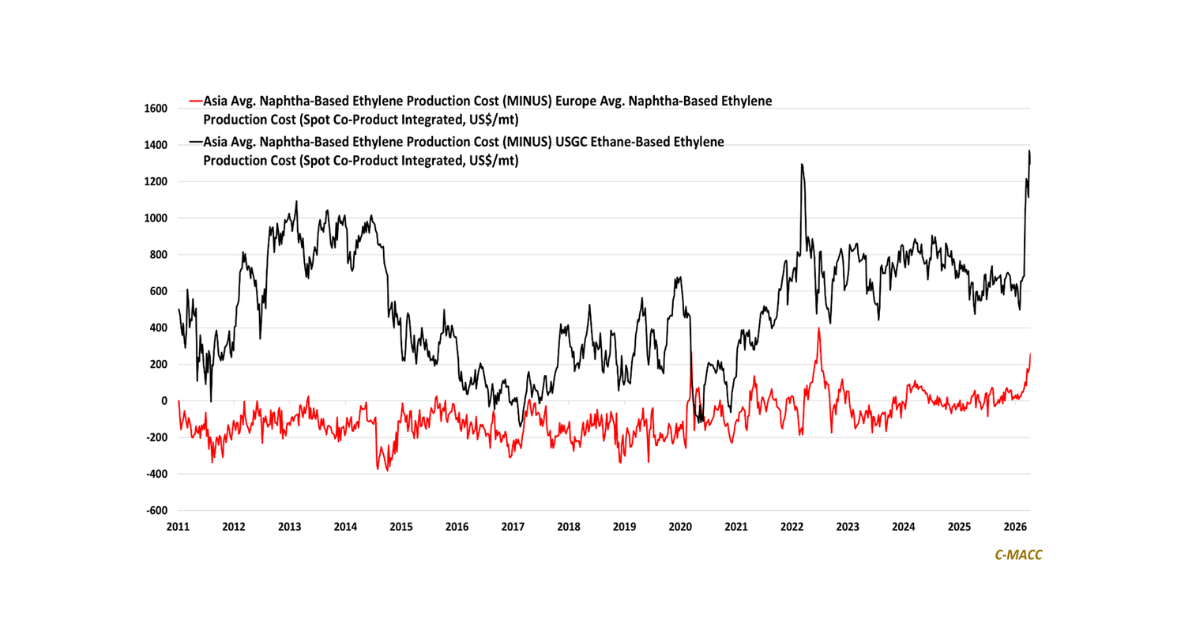

- Other Sector Developments: Ex-US feedstocks are broadly falling following the downward trend in crude oil prices, suggesting broader olefin-chain price pressure ahead, shrinking the North American cost advantage.

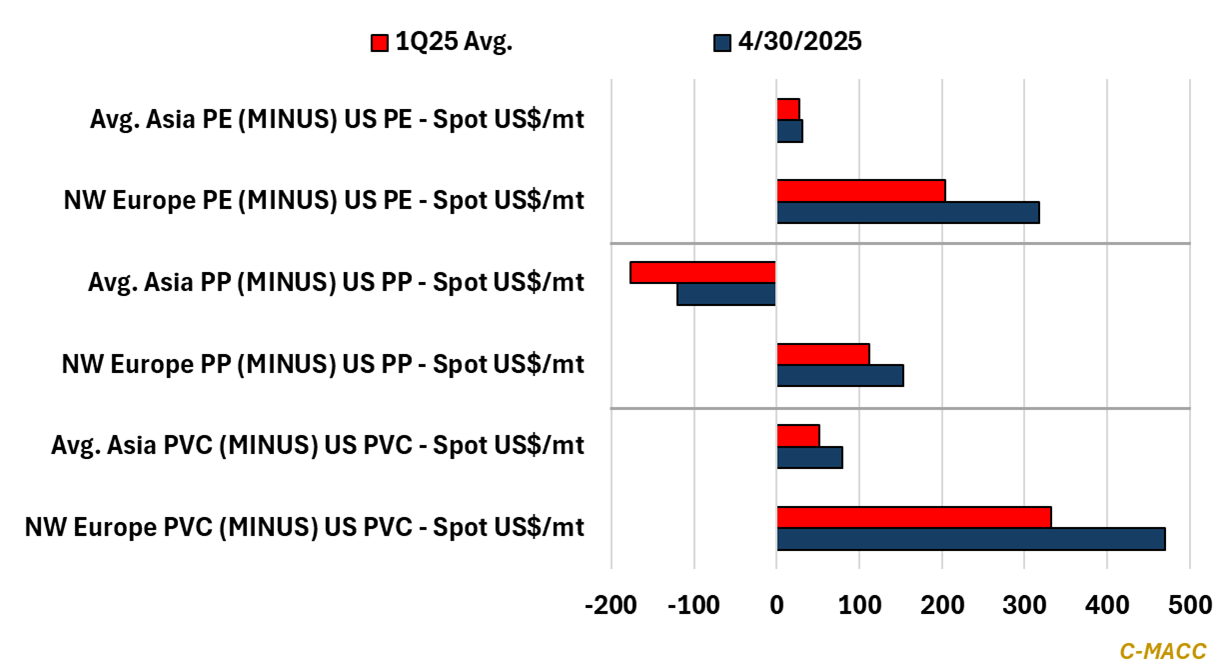

Exhibit 1 – Chart of the Day: US spot PE, PVC, and PP have fallen from their 1Q25 average relative to Europe and Asia.

Source: Bloomberg, Company Reports, C-MACC Analysis, April 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!