Base Chemical Global Analysis

Global Weekly Catalyst No. 278

- General Thoughts: The deepening structural crisis in petrochemicals reveals a broader truth: in a fragmented, volatile world, survival hinges less on scale than on strategic clarity, adaptability, and purposeful reinvention.

- Feedstocks & Energy: A flattening global chemical cost curve, amid diverging feedstock shifts, signals deflationary price pressure and intensifies the competitive imperative for efficiency, integration, and regional advantage.

- Olefins: The US olefin cost advantage erodes as weak derivative pricing, tight propylene spreads, and weak ethylene spot values pressure margins, especially for non-integrated buyers navigating the volatile cost setting.

- Other Base Chemicals: European and Asian benzene prices fell sharply versus the US, setting the stage to lift US imports amid US downstream margin pressure. Separately, global methanol prices further weakened last week.

- Agriculture: Global ammonia markets face downward pressure, and those with flexible contracting, channel pull-through, and product upgrade optionality are best poised for resilience during the remainder of 2025.

- Refining & Biofuels: US crude oil refiners regained margin improvement YoY last week. US ethanol producers face mounting pressure from weak prices and relatively high input costs, likely triggering capacity cuts by 2H25.

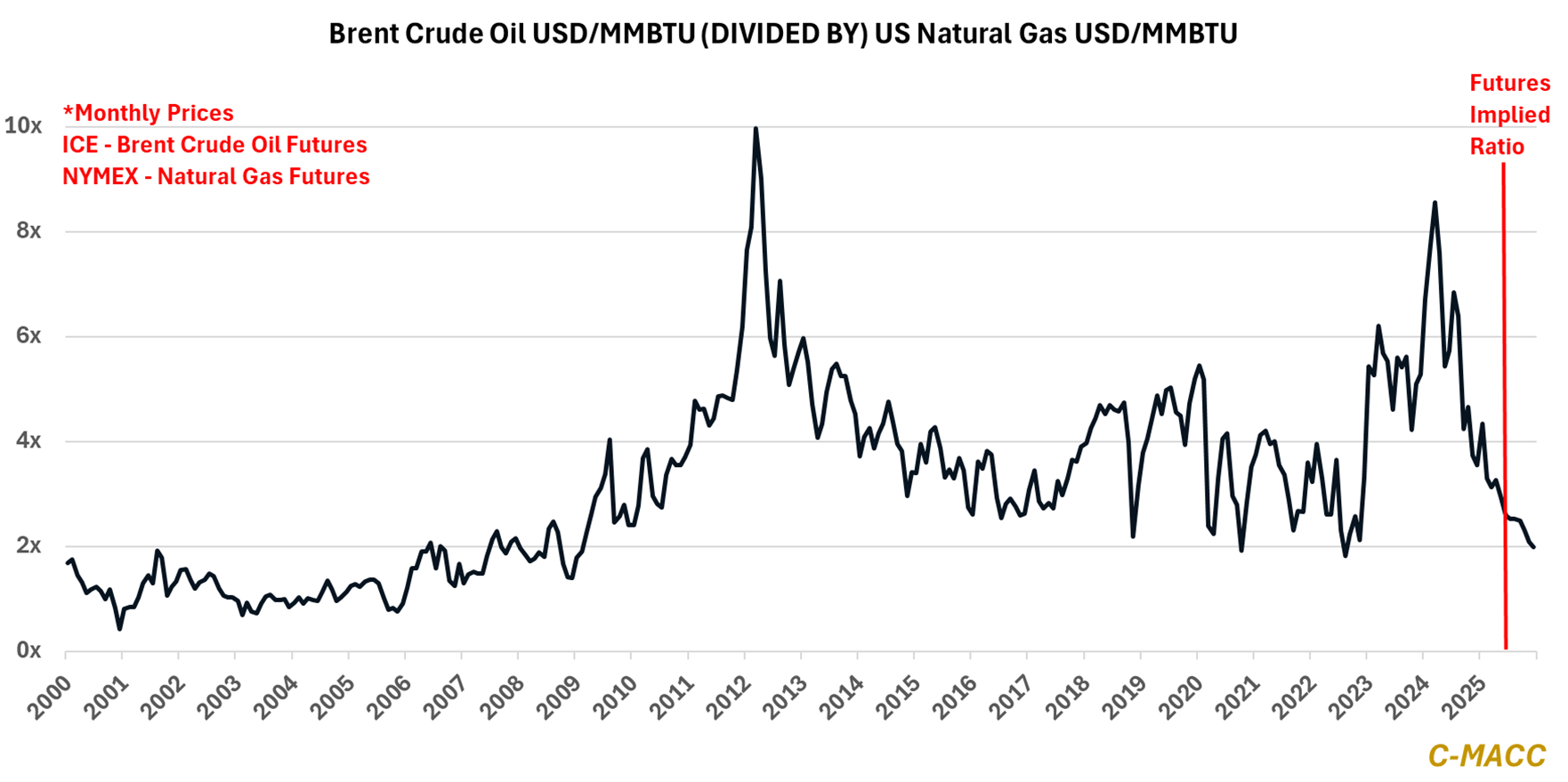

Exhibit 1 – Chart of the Day: The crude oil-to-natural gas ratio has fallen YTD – Futures markets foresee a lower 2H25.

Source: Bloomberg, C-MACC Analysis, May 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!