Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: In an oversupplied and cyclical resin world, we think the next era of relative return leadership will belong to producers fusing scale, innovation, and deep customer intimacy into true competitive advantage.

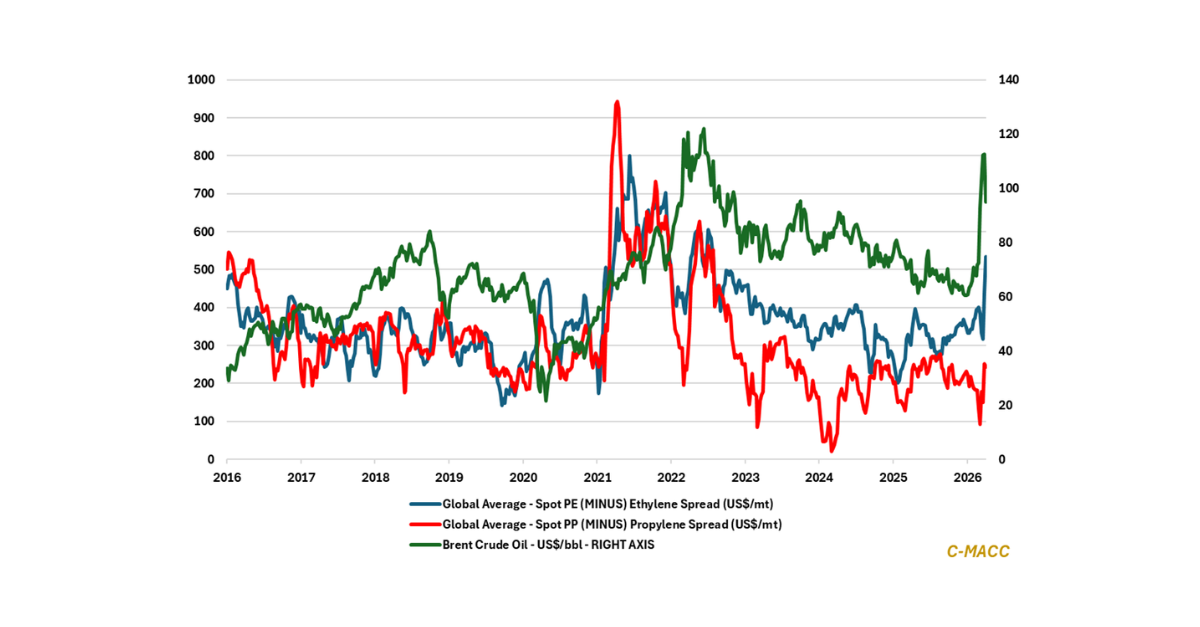

- Polyethylene (PE): As global PE oversupply builds, CPChem’s Singapore HDPE sale and Aster’s acquisition are an example of how integration, scale, and regional advantage are reshaping portfolios to protect long-term returns.

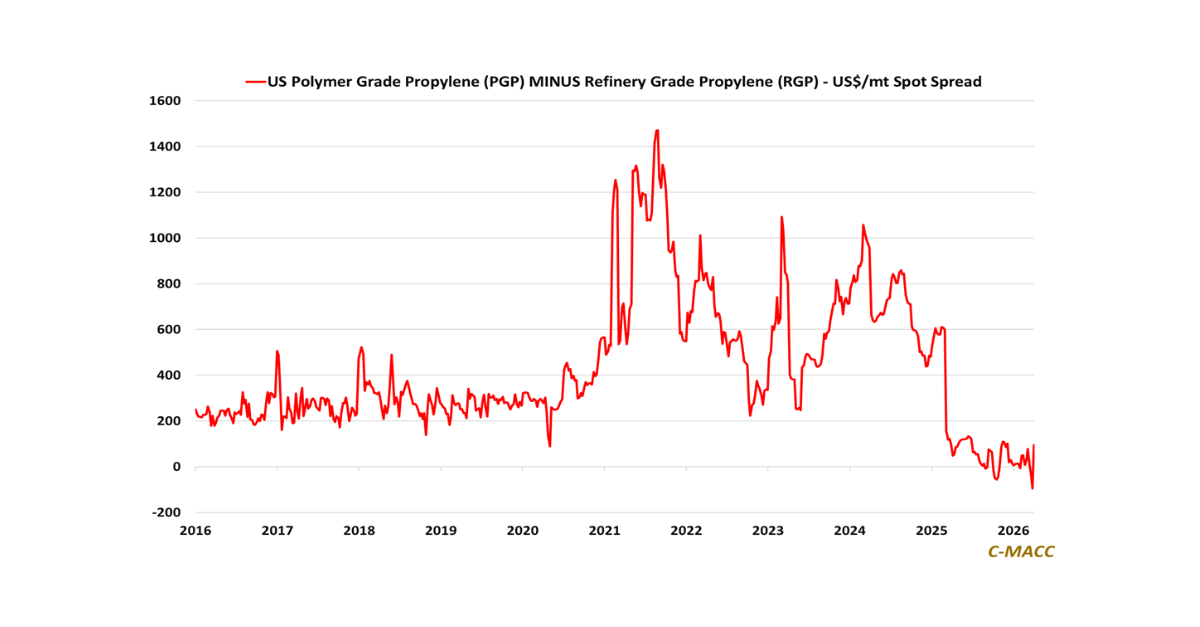

- Polypropylene (PP): Global PP spot prices slid lower last week, with the US seeing the most downward pressure and no-integrated producers most exposed as PGP prices find support and more PP production comes forth in 2Q25.

- Polyvinyl Chloride (PVC): In a squeezed global PVC market, integration and downstream control will increasingly distinguish resilient PVC players from merchant sellers exposed to price volatility heading into late 2025.

- Other Sector Developments: A flattening global polymer cost curve is driving prices lower and sustaining oversupply, forcing producers to rethink integration, scale, and supply strategies for 2H25.

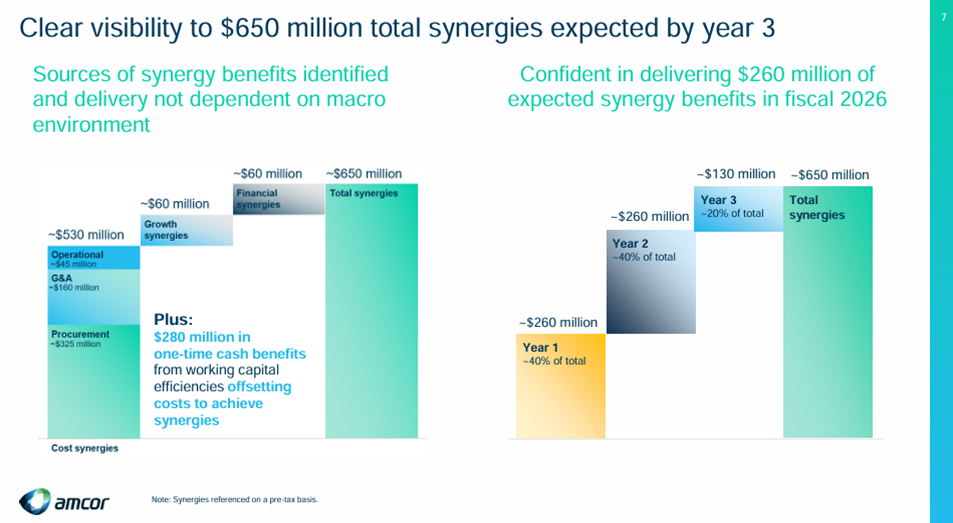

Exhibit 1 – Chart of the Day: Amcor estimates 50% of synergies with the Berry merger will be procurement driven.

Source: Amcor – 3QFY25 Management Earnings Call Presentation, May 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!