C-MACC Sunday Executive Summary

Forging Low-Carbon Europe, Rethinking Global Strategy

- Europe’s manufacturers stand at a crossroads: high power costs, ETS allowances phasing out by 2034, and 2026 CBAM import levies, forcing firms to model carbon costs, reallocate capex, and spur low-carbon innovation.

- CBAM will impose a carbon price levy on select imports from 2026, limiting feedstock arbitrage and forcing importers to redesign value chains, boost green investments, and implement end-to-end digital carbon tracking.

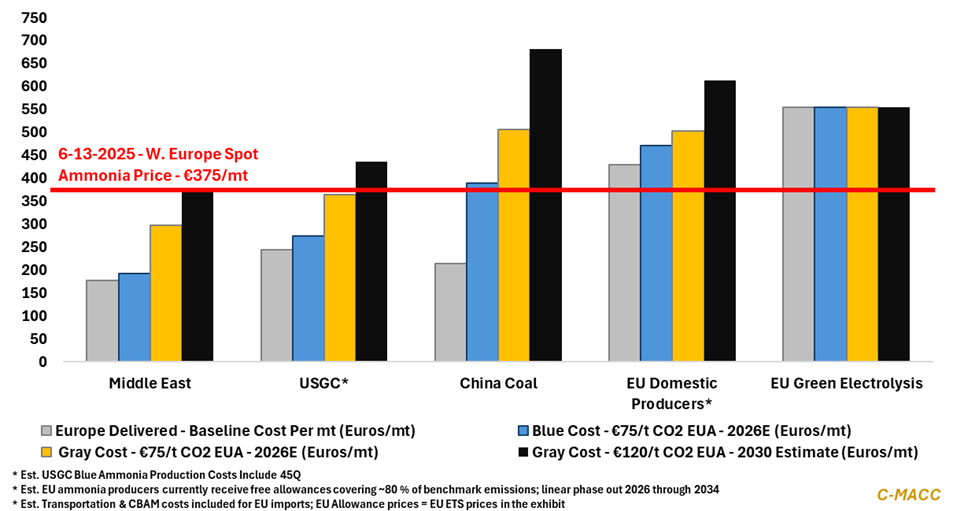

- EU ammonia producers face carbon-cost parity by 2034 as 80% free ETS allowances vanish, while low-cost US and Middle East blue-ammonia exporters—and Chinese coal-CCS ventures—target Europe’s premium prices.

- European petrochemicals are optimizing footprints, reallocating capex, and stress-testing portfolios before a likely 2027–28 CBAM scope expansion to methanol, ethylene, propylene, and polymers, which we view as likely.

- We also discuss petrochemical consolidation in Asia, US-Japan LNG diplomacy, and the redefinition of energy-trade geopolitics. Additionally, the slow US EV adoption relative to Europe is a slight positive for the US grid.

- Companies Mentioned: Yara, CF Industries, Fertiglobe, INEOS, LyondellBasell, SABIC, Borealis, HD Hyundai, Lotte Chemical, American Vanguard, APA Corp, Chord Energy, Borouge, ADNOC, Nutrien, JERA, Macquarie, Brookfield, KKR

- Products Mentioned: Ammonia, Methanol, Ethylene, Propylene, Hydrogen, Electricity, Natural Gas, Naphtha, Ethane, LPG, Polymers, Crude Oil, Corn, Fertilizer, Sugar, Cereal, Biofuel, Critical Minerals, Lithium Carbonate, Plastics, Composites

Exhibit 1: Carbon border shock ahead – CBAM to reflect initial benefits for the EU in 2026; long-term risks remain.

Source: EC Customs 2023/956, Bloomberg, C-MACC Analysis, June 2025

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!