Base Chemical Global Analysis

Global Weekly Catalyst No. 286

- General Thoughts: Chemical cost curves are compressing as feedstock prices retreat, favoring low-cost regions, while mounting oversupply and weak demand signal an urgent need for structural capacity rationalization.

- Feedstocks & Energy: Global feedstock prices retreat toward 2Q lows amid eroding geopolitical risk premiums, with production trends suggesting that chemical production cost curves will likely remain contracted in 2H25.

- Olefins: Olefin prices, on average, were flat to up last week, with margins in the Middle East and North America moving modestly higher – feedstock and demand developments likely to reverse recent price strength in 3Q25.

- Other Base Chemicals: Weakening global methanol, chlor-alkali, and aromatic prices are primarily the result of feedstock values shifting lower, though non-integrated buyers in high-cost regions still face considerable risk.

- Agriculture: Ammonia prices bounced higher last week, though falling Ex-US natural gas prices and weak corn markets present headwinds. We are cautious on near-term margin developments, but constructive longer-term.

- Refining & Biofuels: US crude oil refining margins and US ethanol production margins improved last week, both benefiting from lower costs – we are more concerned with refiner output in 2H25 relative to ethanol production.

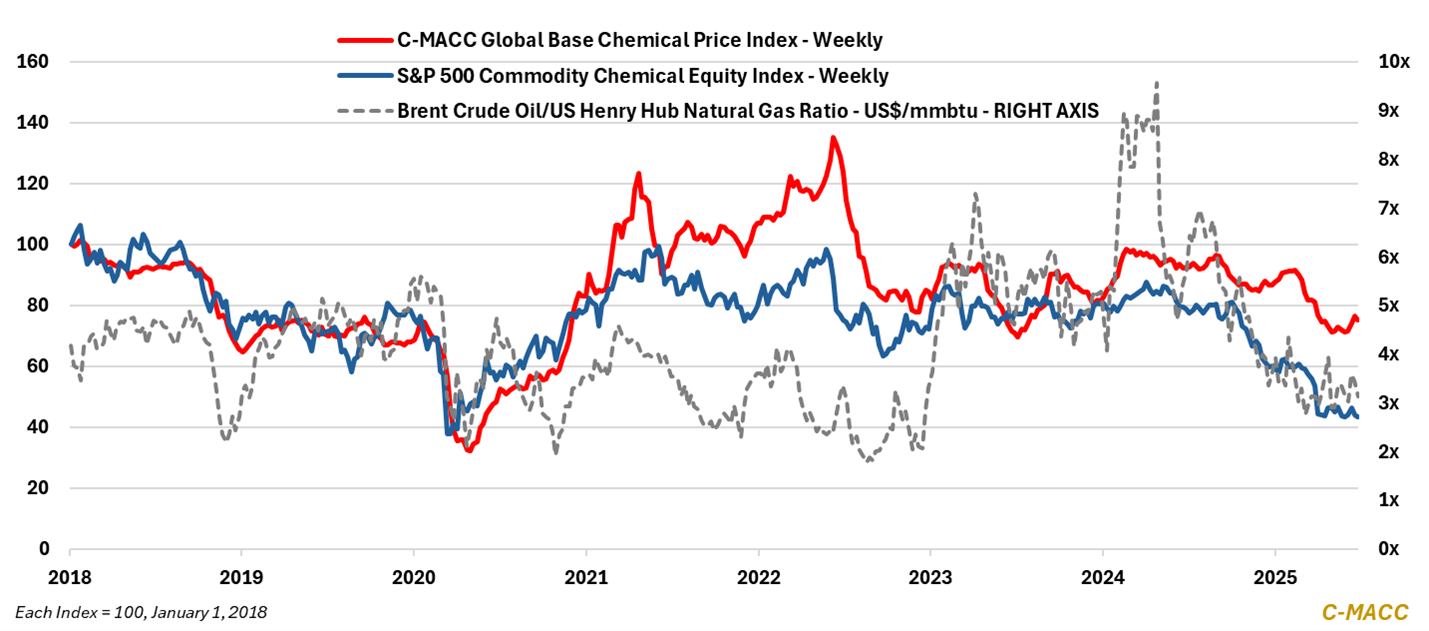

Exhibit 1 – Chart of the Day: US chemical equities mostly stick with cost curve shifts, not chemical prices, in June.

Source: Bloomberg, C-MACC Analysis, June 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!