Global Market Analysis

Weaker Dollar Enhances US Export Competitiveness, Mitigates Risk Across Trade-Linked Capital Projects

Key Findings

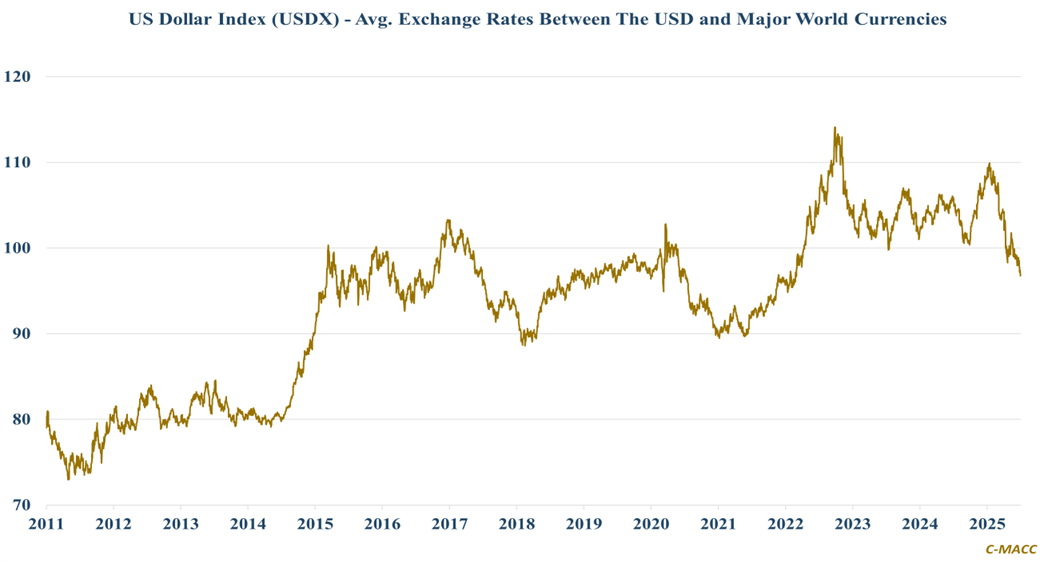

- General Thoughts: The US dollar posted its worst first-half performance since 1973 in 1H25, and this decline lacks proper attention, as it increasingly favors US competitiveness in polymers, chemicals, and agriculture exports.

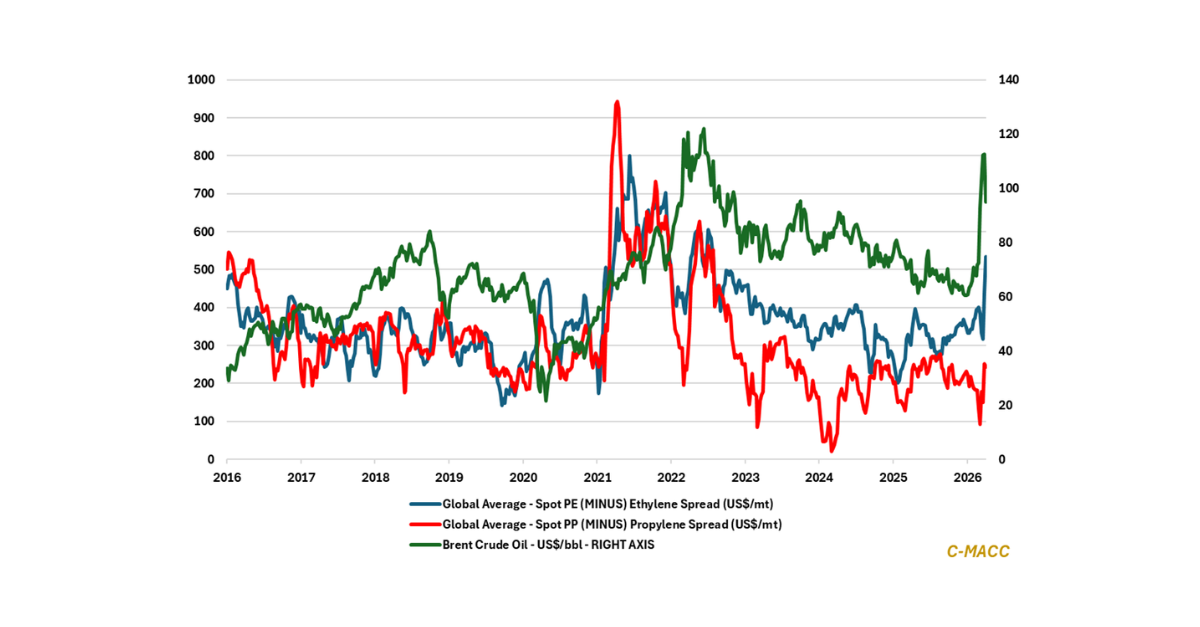

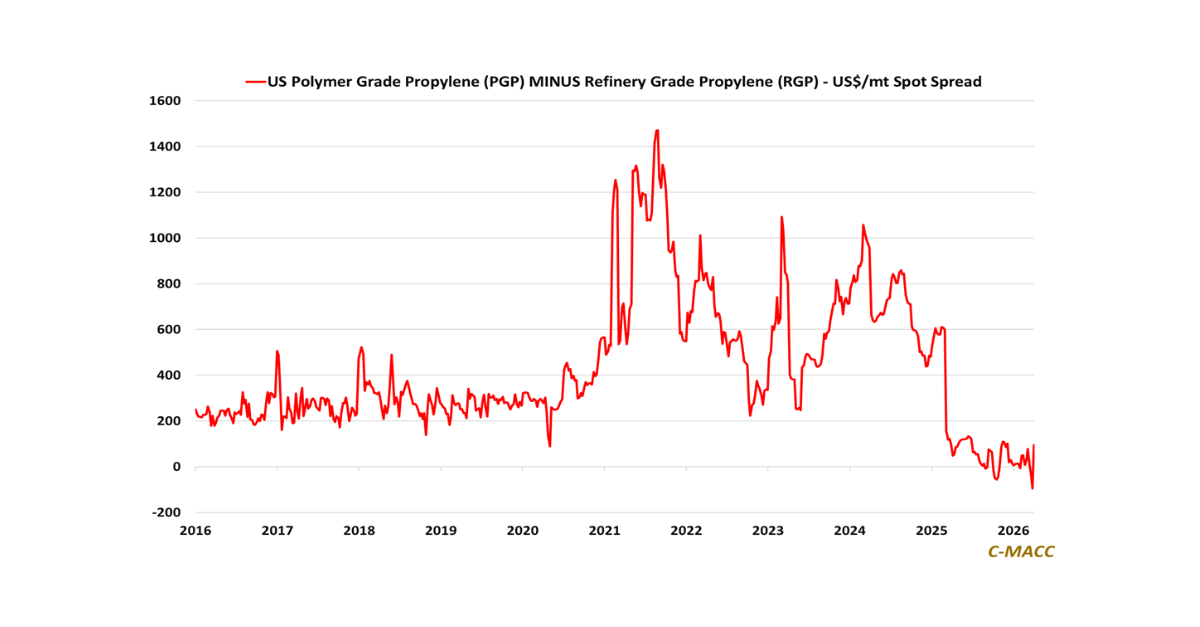

- Supply Chain/Commodities: Europe’s chemical rationalization persists despite a recent sentiment rebound, and US PGP tightness favors integrated, flexible producers positioned to outperform in an uneven 2H25 recovery.

- Energy/Upstream: Canada’s LNG debut signals global opportunity, but infrastructure gaps, regulatory delays, and pricing disconnects threaten domestic gas economics despite export prospects and long-term growth potential.

- Sustainability/Energy Transition: ExxonMobil advances circular plastics through integrated infrastructure. US ethanol markets face rising policy risk, distorting fundamentals, and weakening returns on biofuel production.

- Downstream/Other Chemicals: US housing faces a rare oversupply-demand disconnect. Grain markets remain sentiment-driven, benefiting from dollar weakness but clouded by political risk and fragile 2H25 fundamentals.

Exhibit 1: The US dollar reflects a YTD low relative to other major global currencies, a positive trend for US exporters.

Source: Bloomberg, C-MACC Analysis, July 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!