Base Chemical Global Analysis

Global Weekly Catalyst No. 289

- General Thoughts: Shrinking feedstock spreads are no longer cyclical noise and more of a structural warning that volatility fatigue is masking an urgent need for global chemical capacity cuts in 2H25 if a better 2026 is to develop.

- Feedstocks & Energy: Shrinking oil-to-gas ratios expose a margin trap masquerading as stability, where underpriced stagnation, not volatility, will ultimately starve high-cost producers into inevitable rationalizations.

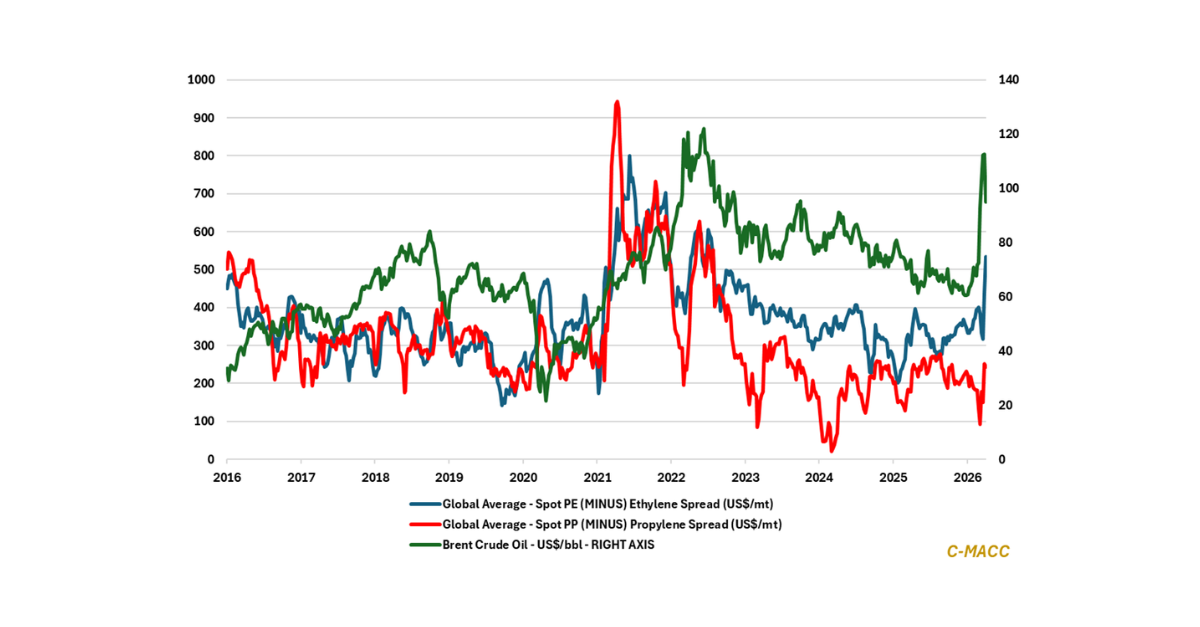

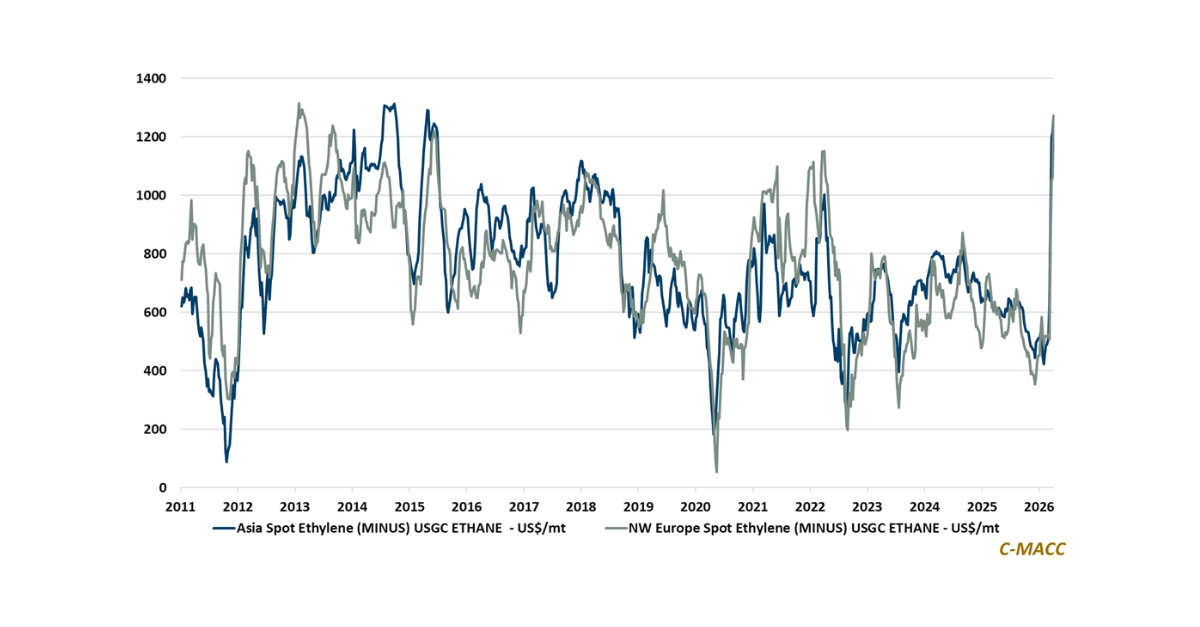

- Olefins: Localized outages mask a more significant truth: global olefin premiums are fragile, with Asian derivative oversupply and soft freight rates poised to arbitrage away Western margin illusions in 2H25 per our model.

- Other Base Chemicals: Falling global methanol prices and resilient China acetyls signal margin erosion ahead, with even low-cost US and Middle East producers vulnerable as gas-to-methanol spreads quietly collapse.

- Agriculture: Flat ammonia prices mask a brewing margin reset, as low-cost and low-carbon supply developments and CBAM-linked carbon pressures quietly threaten high-cost producers clinging to outdated cost structures.

- Refining & Biofuels: US ethanol’s recent profit margin strength has quietly developed amid its price outpacing corn, with upside tied more to oil-linked fuel dynamics and export resilience than grain market fundamentals.

Exhibit 1 – Chart of the Day: Global chemical feedstock ratios have mostly returned to April levels; negative for 2H25.

Source: Bloomberg, C-MACC Analysis, July 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!