Base Chemical Global Analysis

Global Weekly Catalyst No. 291

- General Thoughts: US petrochemical feedstock cost positions improve relative to most of Asia and Europe, which favors improved per unit profits despite our expectation for flattish petrochemical product prices in 3Q25.

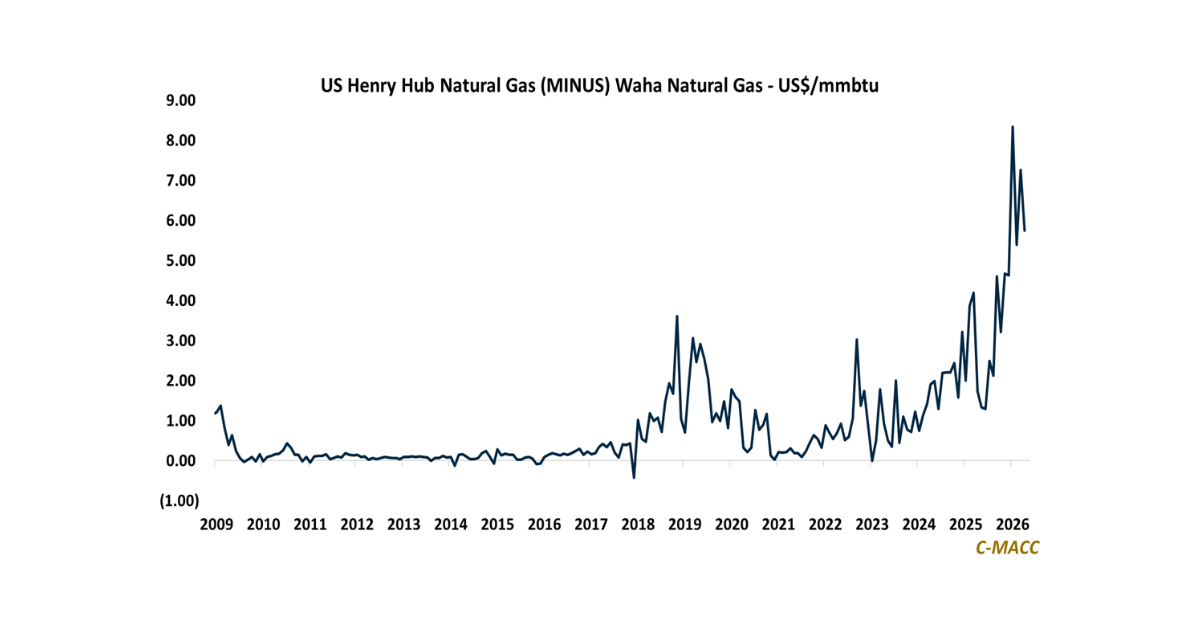

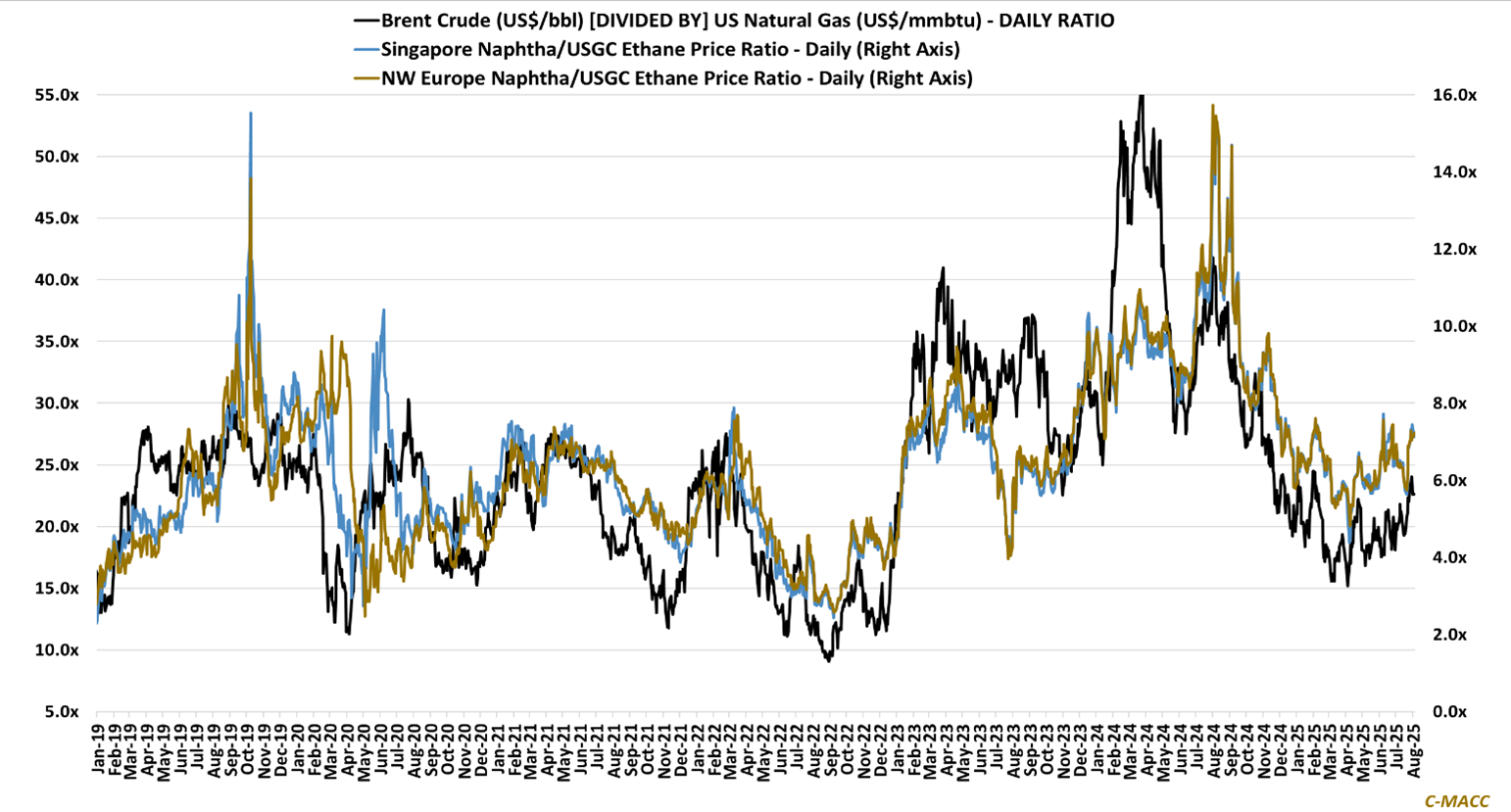

- Feedstocks & Energy: Brent crude oil and Ex-US naphtha prices reflect support compared to falling USGC natural gas and USGC ethane during the past thirty days, reflecting margin benefits for USGC ethylene producers.

- Olefins: US spot ethylene prices increased last week relative to Europe and Asia, which we view as a plus for US integrated producers and merchant ethylene sellers. US propylene markets reflect generally looser conditions.

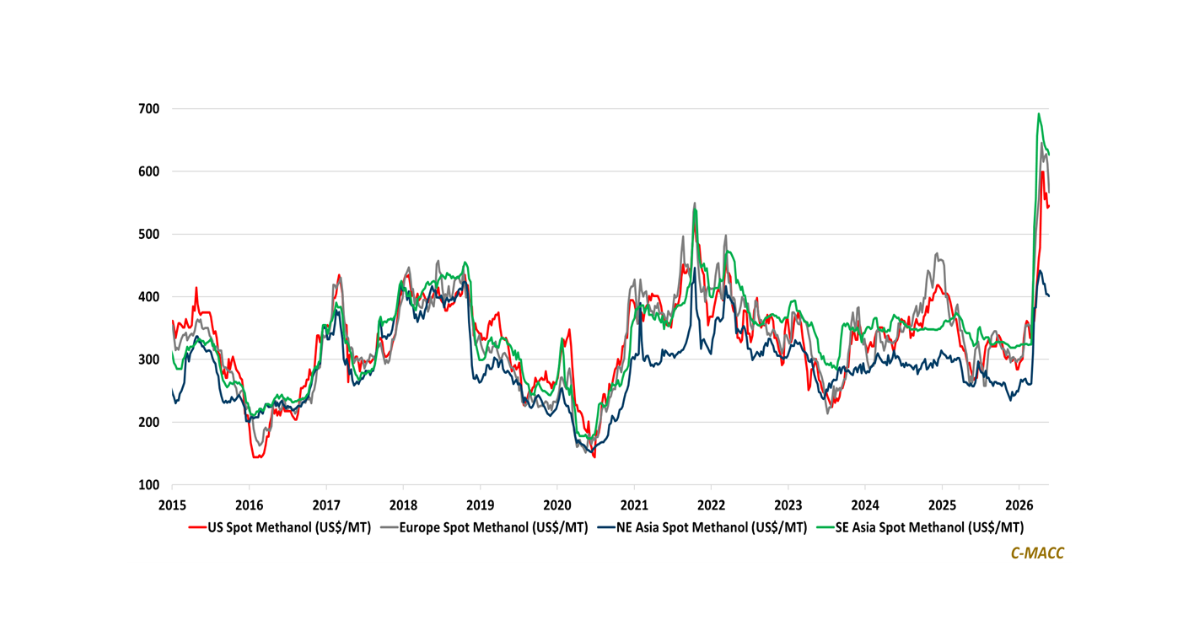

- Other Base Chemicals: US and Europe methanol prices rose last week relative to Asia, with margins seeing the most improvement in the US, favoring producers, such as Methanex, relative to net buyers, such as Celanese.

- Agriculture: Global ammonia prices showed very modest improvement last week, following substantial price hikes the previous week. With corn prices at a YTD low, we continue to take a cautious near-term demand view.

- Refining & Biofuels: US ethanol production margins increased last week to a new YTD high, benefiting from falling corn costs and relative support in ethanol and co-product prices. US refinery margins also improved last week.

Exhibit 1 – Chart of the Day: Crude oil and Ex-US naphtha approach YTD highs relative to US natural gas and ethane.

Source: Bloomberg, C-MACC Analysis, August 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!