Base Chemical Global Analysis

Global Weekly Catalyst No. 293

- General Thoughts: Global feedstock cost deflation was broad-based last week, reinforcing downward pressure on chemical prices amid oversupply, with cost position being a key determinant of relative 2H25 performance.

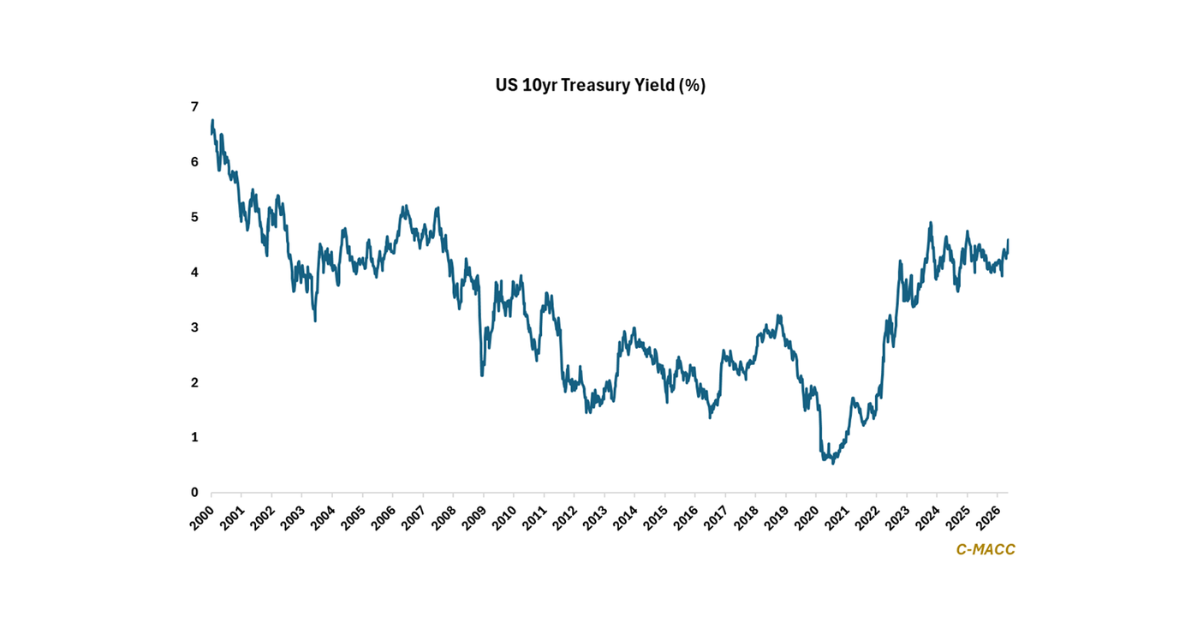

- Feedstocks & Energy: Global chemical feedstock values fell last week as natural gas and crude oil weakened, resetting cost curves lower, compressing petrochemical upside, and reinforcing relative US margin strength.

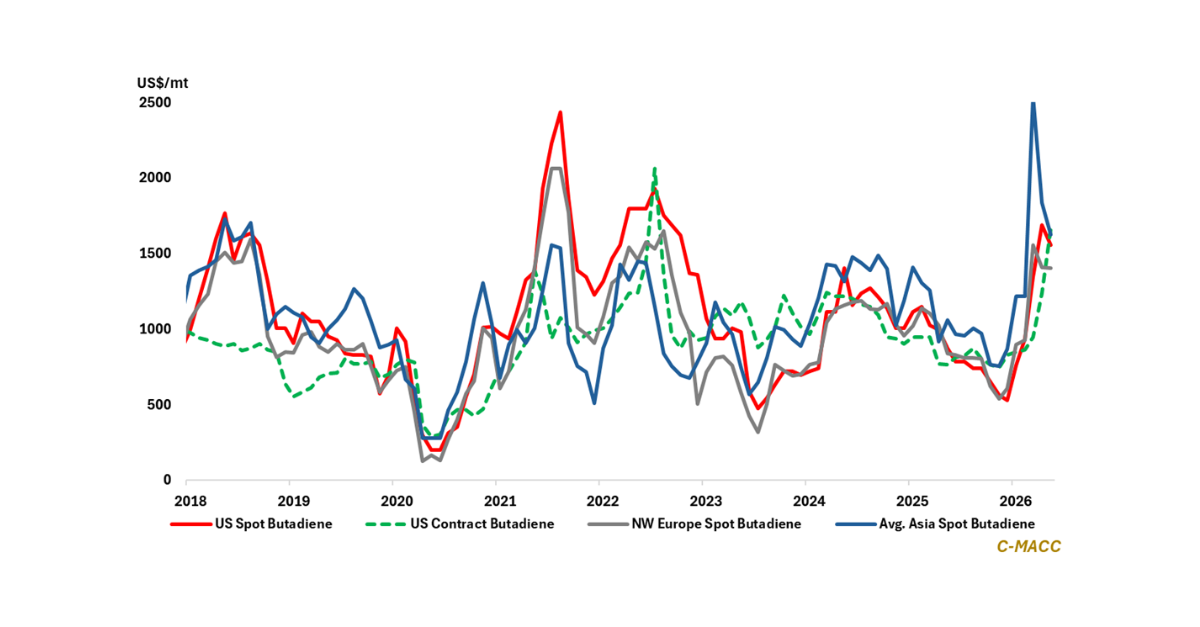

- Olefins: Global olefins weakened as ethylene and propylene diverged regionally, reinforcing US competitiveness, exposing European vulnerability, and leaving 2H25 upside capped absent unplanned outages and crude strength.

- Other Base Chemicals: Benzene tracked crude lower, chlor-alkali found selective Chinese support, and methanol diverged regionally, with China cushioning acetic acid erosion as tightening spreads foreshadow 2H25 volatility.

- Agriculture: Global ammonia spot prices held steady WoW despite gas weakness, but cheapening feedstock, low crop prices, and acreage shifts likely signal renewed downside before sentiment resets into mid-2026 recovery.

- Refining & Biofuels: US ethanol production margins rose again last week, reaching a YTD high amid falling corn costs and firm ethanol and co-product prices. US refinery margins were unchanged, despite lower crude prices.

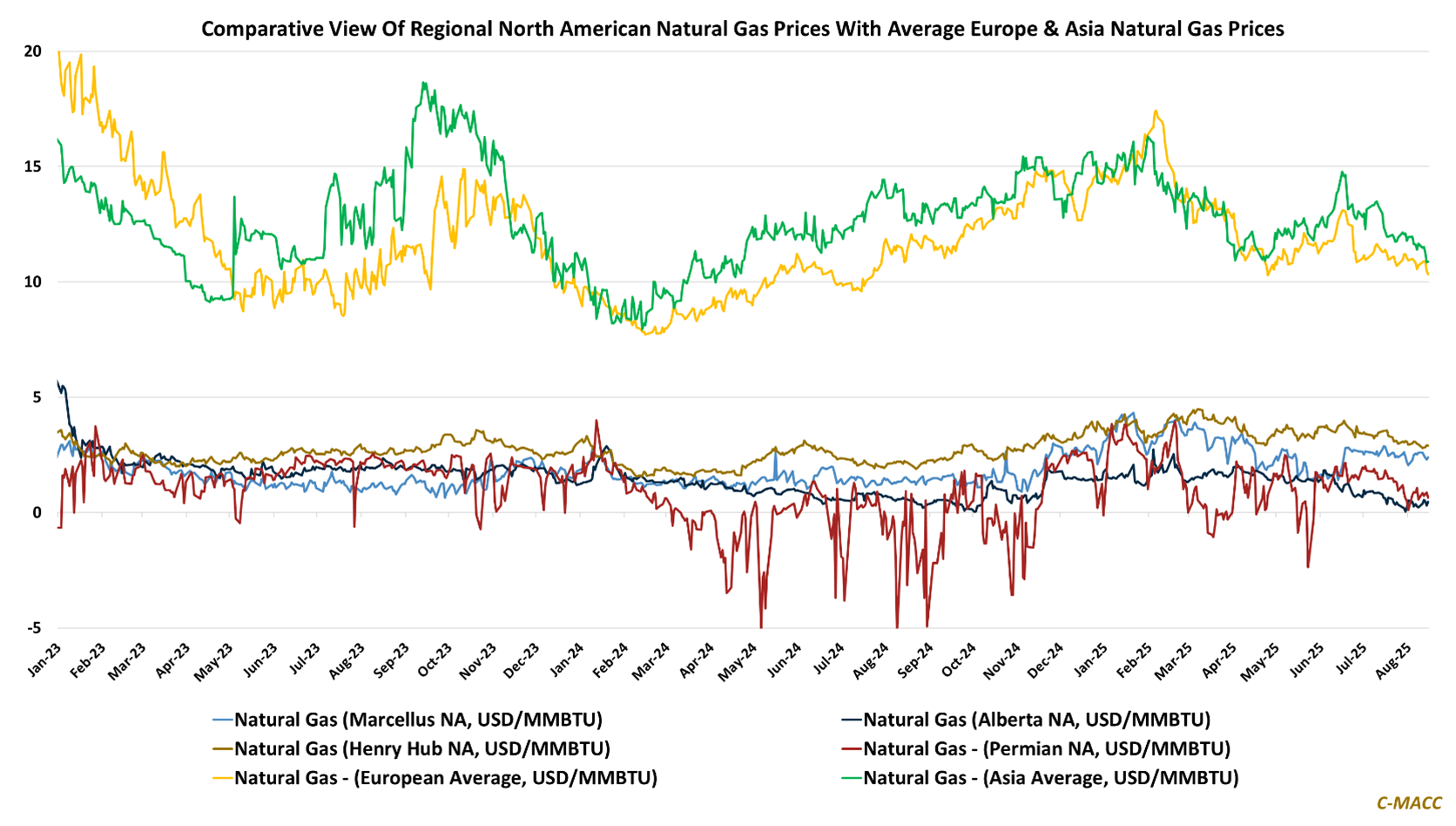

Exhibit 1 – Chart of the Day: On average, global natural gas prices trend lower in 3Q25; many markets near YTD lows.

Source: Bloomberg, C-MACC Analysis, August 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!