Global Market Analysis

Margins Be Damned: Rise of the Counter-Cyclical Titans

Key Findings

- General Thoughts: State-backed expansion, protectionist trade shifts, and counter-cyclical consolidation are redefining chemicals, rewarding scale, optionality, and resilience over near-term profits or pure cost leadership.

- Supply Chain/Commodities: BHP’s copper pivot and SQM’s lithium resilience illustrate how scale, optionality, and policy insulation increasingly dictate global competitive advantage over cyclical pricing or cost leadership.

- Energy/Upstream: LNG contracts will increasingly ship cheap US natural gas into geopolitical leverage abroad, while elevating domestic price risk, transforming the US advantage into rising costs and industrial vulnerability.

- Sustainability/Energy Transition: Solar’s fragility and battery storage’s continued rise reveal that competitiveness hinges less on wafer costs or subsidies, and more on regulatory resilience, power security, and arbitrage flexibility.

- Downstream/Other Chemicals: Lowe’s FBM acquisition targets home builders amid historic sentiment lows, proving distribution scale and counter-cyclical conviction now outweigh cyclical confidence in housing markets.

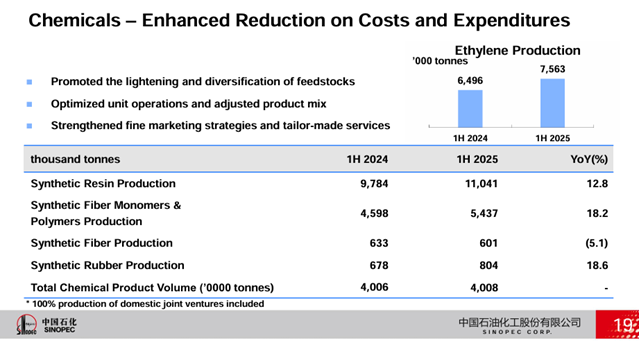

Exhibit 1: Despite segment losses, Sinopec grew its ethylene production in 1H25; it plans to boost it further in 2H25.

Source: Sinopec – 1H25 Results Presentation, August 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!