Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

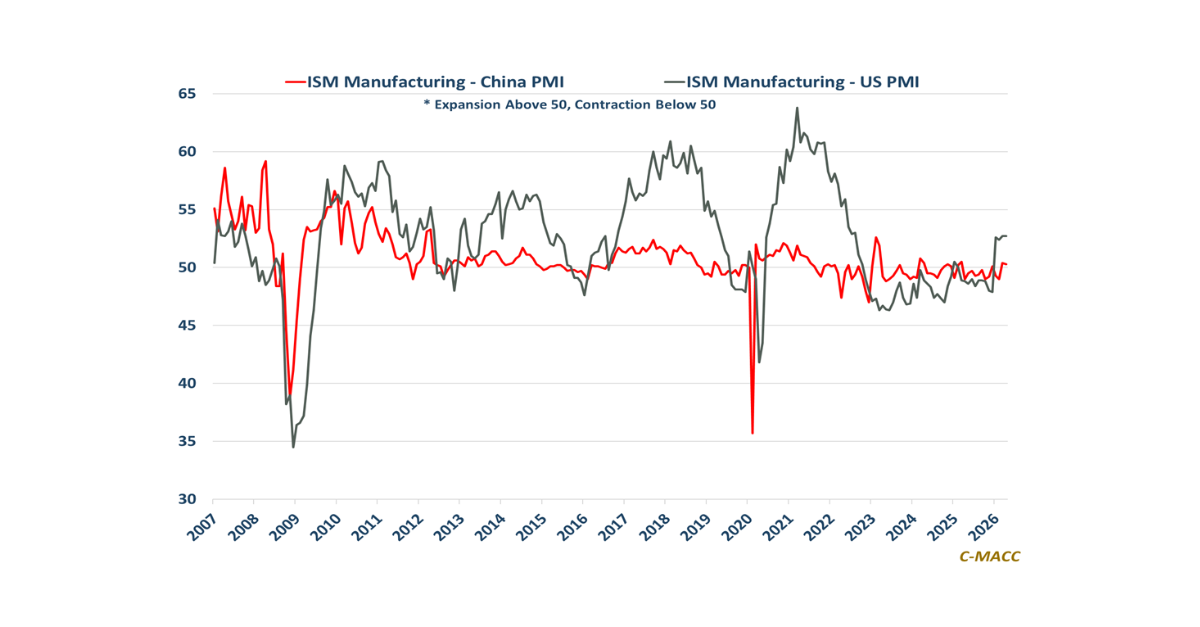

- General Thoughts: Escalating global protectionist policies and uneven restructuring are fracturing global polymer trade, amplifying oversupply, deepening regional imbalances, and ensuring heightened price volatility through year-end.

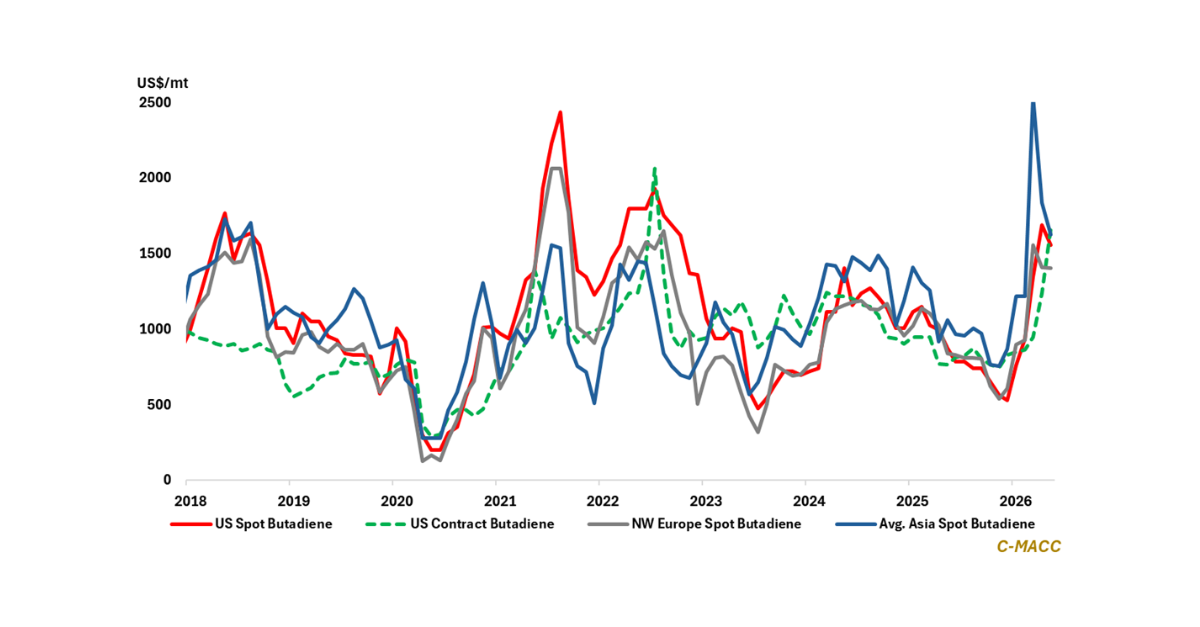

- Polyethylene (PE): Global PE markets remain trapped in an oversupply setting, with generally weak demand, rising protectionist actions, and new capacity limiting upside potential amid likely persistent price pressure into 4Q25.

- Polypropylene (PP): China’s surging PP exports, layered atop relentless new capacity, are redefining global trade flows, eroding margins and PP-to-PGP spreads abroad, and underscoring a 4Q25 structural test of supply discipline.

- Polyvinyl Chloride (PVC): Global PVC markets confront a 2H25 recalibration as China’s export surge collides with India’s ADDs, forcing rerouted flows, intensifying competition, and exposing structural fragilities that will shape 2H25 outcomes.

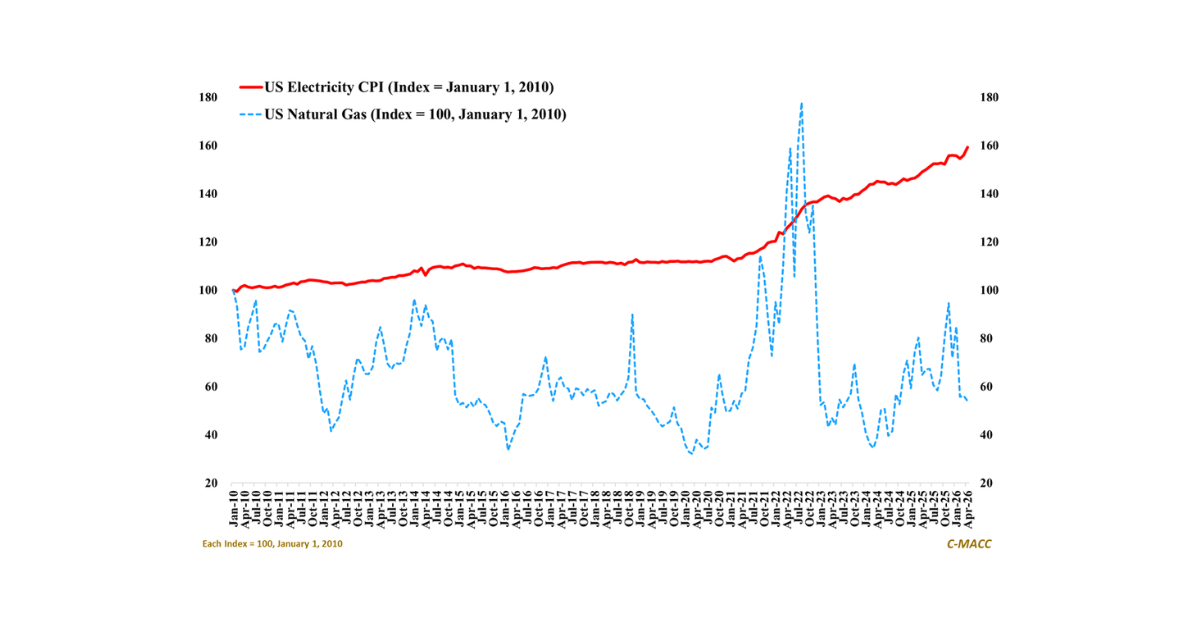

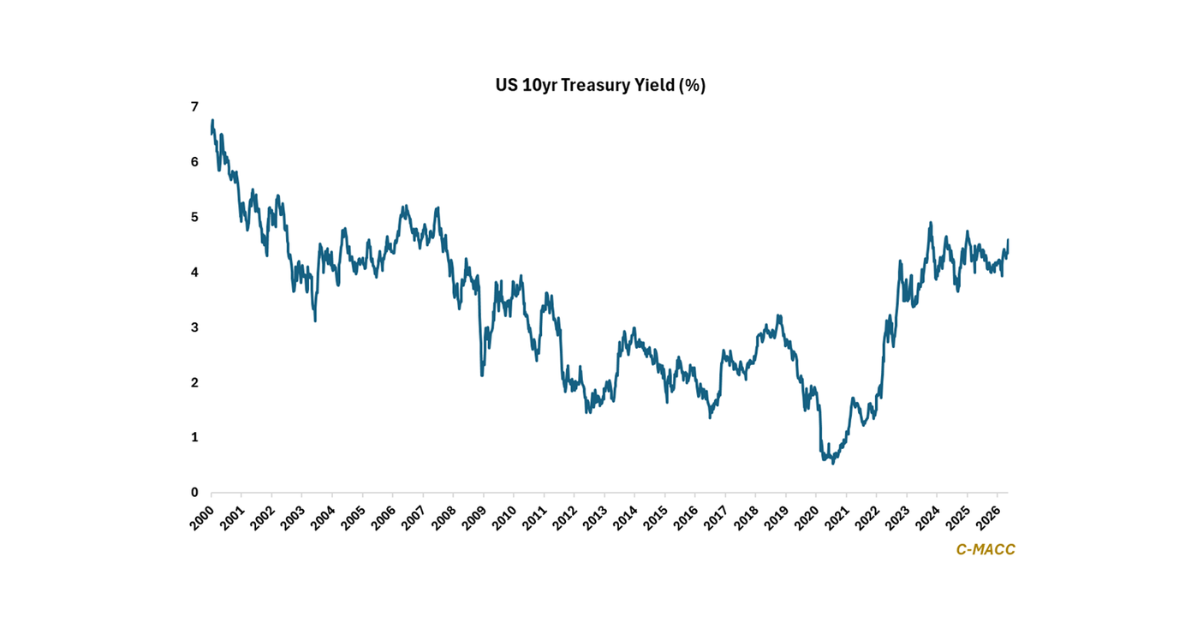

- Other Sector Developments: Recent US natural gas weakness relative to crude oil suggests more integrated polymer margin support for US producers than Europe and Asia, though oversupply and varied trade policies pose a risk for most.

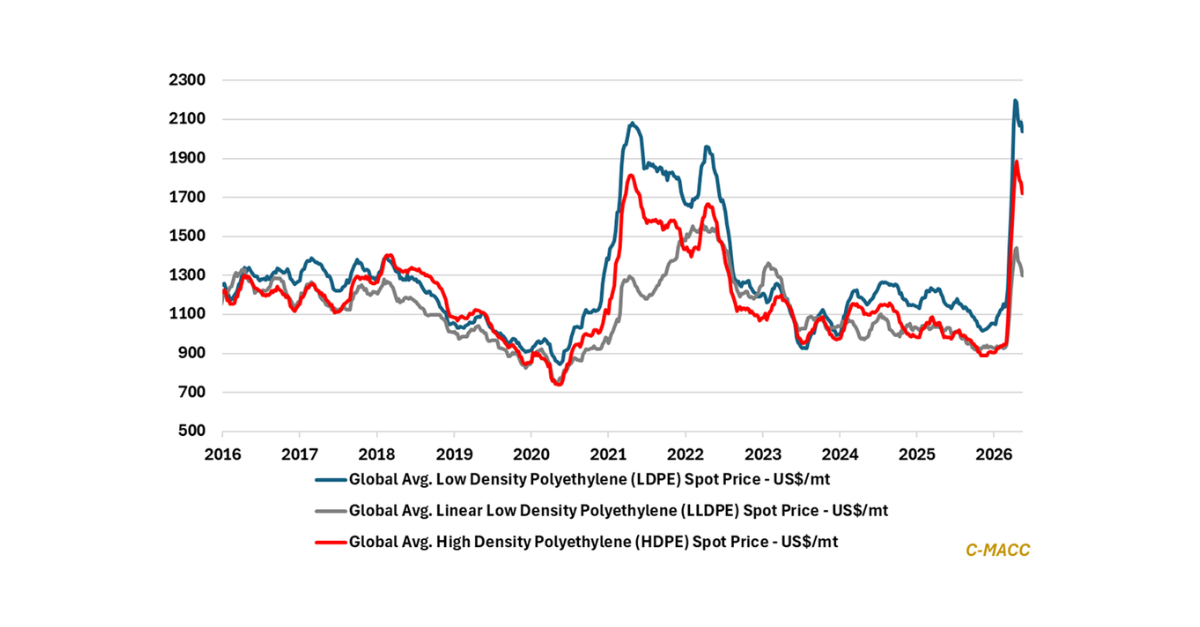

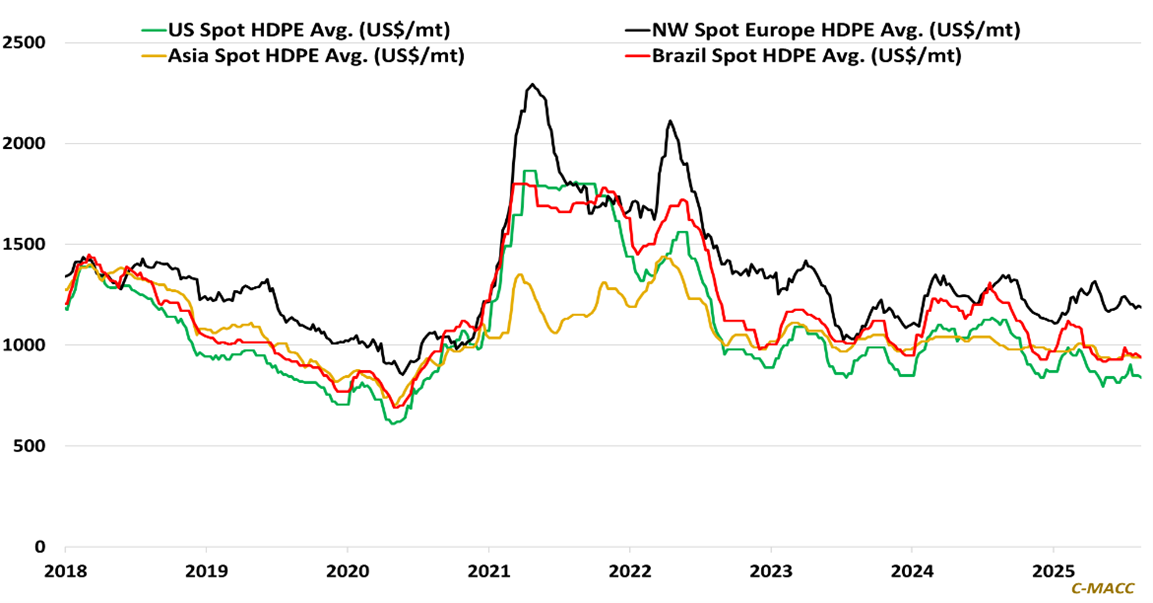

Exhibit 1 – Chart of the Day: Global spot HDPE prices likely stay depressed into year-end, absent unplanned events.

Source: Bloomberg, Company Reports, C-MACC Analysis, August 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!